Two years ago, Chinese electrical vehicle (EV) maker Nio (NYSE:NIO) announced it didn’t have the funds to last another 12 months. Now, NIO stock is a strong-buy rated EV trade with massive upside potential going into December. Plus, the latest news and upcoming events point to an eventful 2022 for the company.

NIO’s business has grown impressively over the past year, and news from the premium EV maker’s management team has never been more bullish. However, shares are down by more than 18% year-to-date (YTD) and have continued to slide as we exit November.

An Exciting Shell Deal to Move NIO Stock

In a news release published by Shell (NYSE:RDS.A, NYSE:RDS.B) on Thursday, Nov. 25, the company announced it has partnered with Nio to improve the charging experience for EV customers around the world.

According to the release, the two firms will “develop a network of co-branded battery swap stations. Cooperation in China will start with two pilot sites and aim to reach 100 sites by 2025, as well as additional co-branded battery swap stations at Shell EV charging hubs and Shell Recharge fast chargers at Nio locations.” Cooperation will extend to Europe in 2022.

Nio’s revolutionary and patented concept of battery swaps is gaining traction with EV drivers. Instead of waiting hours for a battery to be fully charged (and wasting precious time on a trip), NIO’s customers can simply swap their depleted battery unit for a fully charged one in minutes.

The battery swap concept is making the switch from internal combustion engines to EVs much easier for those who have been sitting on the fence. It also made it possible for the company to offer a “battery-as-a-service” (BaaS) program. This is an entirely new value proposition for customers to own just the vehicle and lease the battery to avoid worrying about expensive replacements after degradation.

Shell could take the concepts globally, opening new growth frontiers for the Nio brand.

Growth Into New Markets on the Horizon

Most noteworthy, the latest Shell/Nio partnership could help accelerate the latter’s entry into new European markets. It could also make compelling convenience propositions to North American drivers.

Shell is the world’s largest operator of refueling stations globally with about 46,000 locations in several countries. It intends to operate north of 500,000 EV charge points worldwide by 2025. Nio’s battery swapping is an innovative proposition the global mobility retailer wishes to introduce to select markets.

The EV manufacturer could have many more recurring revenue points as the Shell partnership grows. Thanks to the deal, Nio can gain more brand visibility and potentially appeal to a larger customer base.

The future is definitely looking better and brighter for NIO stock.

Investors Should Love Nio’s Evolving Business

Nio started making

vehicle deliveries in 2018. Since then, the business has been ramping up smoothly and swiftly. Recently, the company upgraded the capacity of its flagship production location and made further investments in its co-production facility. With that and new products from Nio’s second facility, the company could increase annual capacity to over 600,000 vehicles by the second half of next year.

The current long waiting times for new customers could soon be a thing of the past. Even better, Nio’s gross margins have been improving with productivity growth. Vehicle gross margins could expand from 18% during the third quarter of 2021 to 25% in the long run.

Increasing competition remains a factor to watch as new entrants into the Chinese EV market carve out their own niches. But analysts are bullish on NIO’s financial performance, growth outlook and cash flow generation capacity right now.

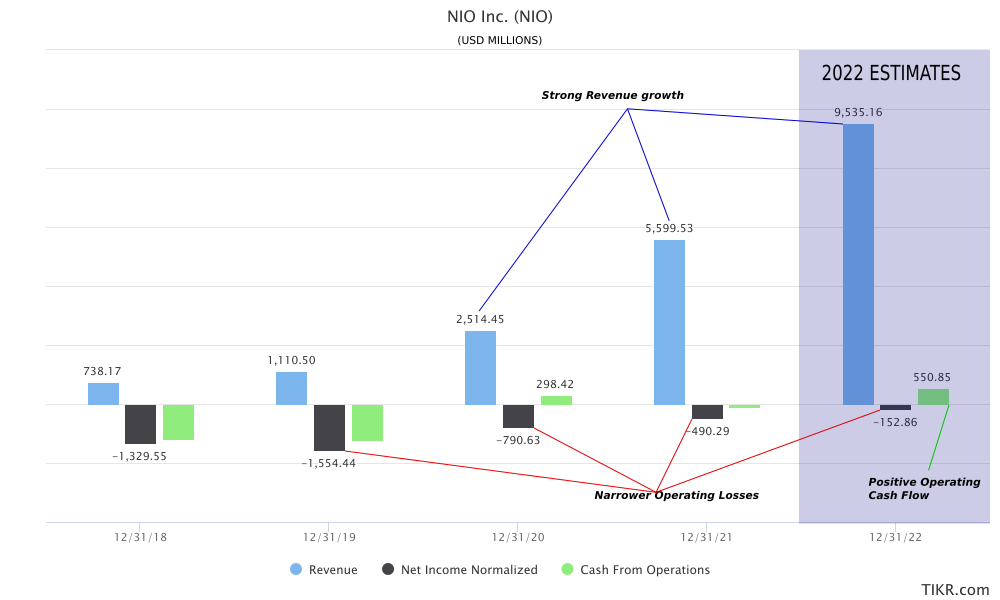

<em>Wall Street Analysts’ projections for Nio’s revenue, earnings, and cash flow in 2022. Source: <a href="https://tikr.com/">TIKR.com</a></em>

If Wall Street’s predictions for Nio’s operations play out over the next year, the company could significantly grow its revenue, narrow its operating losses and generate about half a billion dollars in operating cash flow in 2022.

The Bottom Line on NIO Stock

Nio is getting closer to generating sustainably positive operating cash flows as its capacity and revenues grow. Positive cash flow will allow the business to rely less on new capital injections for growth initiatives. The company could soon be able to fund some projects from internally generated cash flows.

In other words, Nio has the potential to become self-sustainable. Stockholder dilution could be minimal in the near future.

Nio’s shares may remain volatile in the near term, as the stock still faces the risk of delisting from U.S. exchanges. Auditing issues remain a problem, but a solution is still being sought among the respective countries’ authorities. Any success on this front could significantly reduce the risk for Chinese companies, including NIO stock.

Investors may not necessarily expect 1,200% gains in 2022 as seen in 2020, but impressive execution on Nio’s part could justify higher stock prices next year. Watch out for potential fireworks and new products during Nio Day on Dec. 18.

On the date of publication, Brian Paradza did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

Brian Paradza is an investing enthusiast who was awarded the CFA Charter in 2019. A strong believer in fundamentals-based long-term investing, Brian learns from gurus like Warren Buffett but acknowledges human behavioral tendencies that drive short-term “madness”. You may find him inquisitive as he examines tech investing opportunities, cannabis, blockchains, and the new cryptocurrencies asset class.