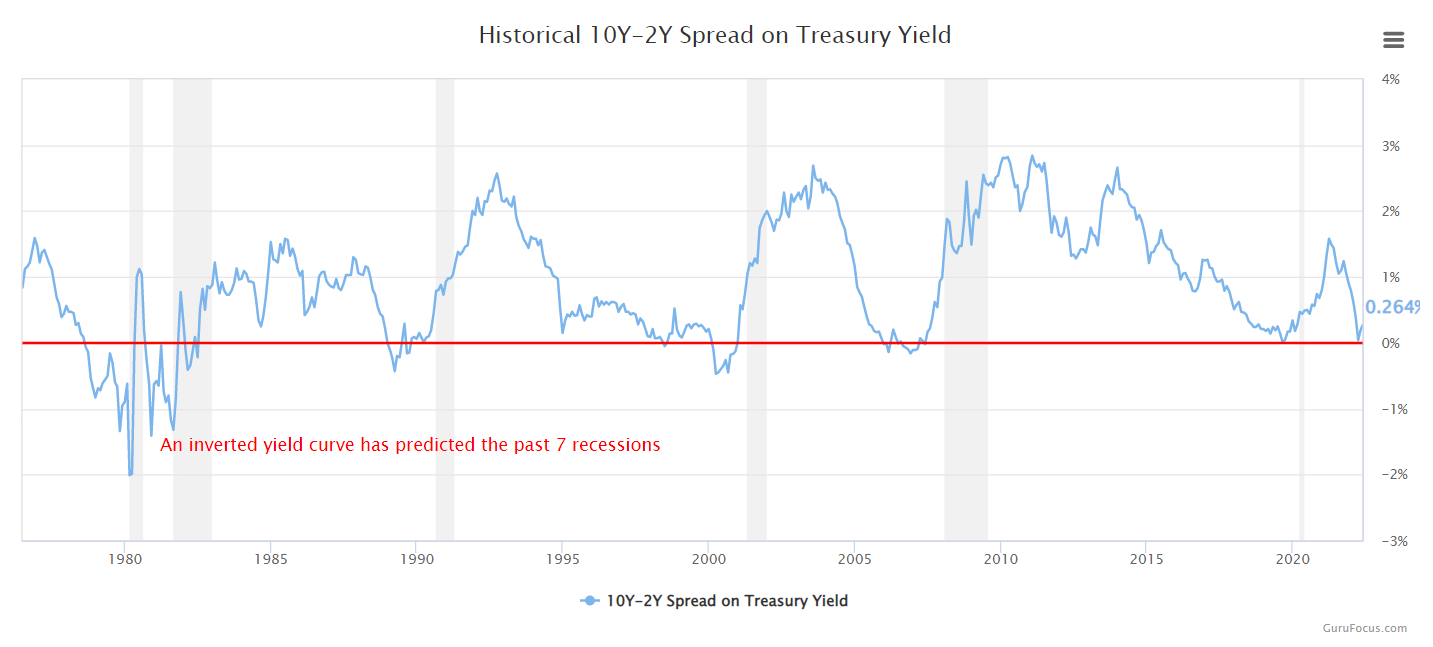

- The 10 to 2 year spread on the treasury yield suggests that durable good sales could contract soon.

- Ford (F) is overvalued relative to its fair book value.

- Quantitative metrics suggest that F stock doesn’t exhibit an attractive risk-return tradeoff.

Upgrades and downgrades are thrown around cheaply these days. Of course, a company such as Ford (NYSE:F) holds a solid market position and possesses a high-quality business model. However, matters shouldn’t be looked at in isolation, but rather in context. For instance, a company’s long-term use case isn’t always a valid variable to use for near term stock price discovery.

When I look at F stock, I see two fault lines. First off, I see a stock that has faced a selloff within its quantitative bounds, suggesting that it is not a “buy-the-dip” opportunity. Secondly, Ford forms part of the durable goods market, characterized by exponential peaks, bottoms, and troughs that are inextricably linked to economic cycles.

I firmly believe F stock will be one of the underperformers in the following months. Here’s why.

| Ticker | Company | Price |

| F | Ford Motor Company | $13.15 |

Morgan Stanley Upgrade

Adam Jonas of Morgan Stanley (NYSE:MS) recently upgraded F stock from “underweight” to “equal-weight” as he believes its risk-to-reward profile has finally hit a balance. I disagree entirely with Jonas’ call as I think it is unaligned with economic, financial, and quantitative reality.

First of all, it needs to be mentioned that we are, in fact, in a contractionary economic cycle. The 10 to 2 year treasury yield spread has dropped significantly, meaning that the market foresees that interest rates will rise rampantly in the short run. Yet, the spread also suggests that interest rates might fall in the long-term because of a possible medium-term recession.

Click to Enlarge

If the yield curve spread is anything to go by, then I’m afraid that durable goods will struggle. There is an overwhelming amount of evidence that financed durable goods are often on the receiving end of consumer utility cycles. Thus, Ford’s impressive sales figures during the past two years will probably be met with shockingly low figures over the next few quarters.

Furthermore, Ford is battling with its Rivian (NASDAQ:RIVN) allocation. Recently, the company lost approximately $5.4 billion on its Rivian investment, eroding its investors’ residual value in the process. Although Ford has dumped a significant amount of its stake in Rivian, the company still owns 87 million shares, which adds additional risk to F stock, in my opinion.

Valuation Metrics

Ford is considered a cyclical value stock, meaning that its stock price will likely oscillate around its price-to-book multiples. Ford stock is trading at 1.1x its book value, suggesting that it is an overvalued asset. Additionally, the company’s levered free cash flow has dropped by 51.45% year-over-year, implying that the stock is also losing intrinsic value on a cash basis and not only on an accrual basis.

Lastly, Ford has a high beta of 1.15. High beta stocks exhibit excess sensitivity to the general market. Thus, a prolonged market selloff could lead to substantial losses for Ford investors, meaning that it provides a poor risk-to-return profile.

A Final Word on F Stock

Ford stock exhibits a Sharpe ratio of negative 0.16. Thus, Morgan Stanley’s claim that the stock’s risk-to-reward prospects are well-aligned is a folk tale. Additionally, we’re in an economic environment that could see durable goods suffer significantly. Thus, I’m bearish on Ford stock and think it’s a sell for now.

On the date of publication, Steve Booyens did not hold any position (either directly or indirectly) in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.