This article is excerpted from Tom Yeung’s Profit & Protection newsletter dated July 29, 2022. To make sure you don’t miss any of Tom’s picks, subscribe to his mailing list here.

Investing in electric vehicle stocks is deceptively tricky. For every Tesla (TSLA) that makes it, dozens more, from Electric Last Mile Solutions (ELMSQ) to Workhorse (WKHS), fizzle out.

After all, electric vehicles are first and foremost, vehicle producers.

These capital-intensive automakers tend to make poor investments. Car manufacturers often spend millions to update production lines, only to find that customers have moved on to a different trend by the time the first vehicle gets produced.

Dealership networks also create a headache for manufacturers; most states have regulations that limit the number of new dealers, forcing new entrants to sell direct-to-consumer.

It’s no surprise that companies like Lordstown Motors (RIDE) have struggled against entrenched competitors like Ford (F) and General Motors (GM). $100,000 invested in the 74 EV stocks tracked by Thomson Reuters would have shrunk to $54,000 over the past year.

The Good News About Electric Vehicles

At the same time, electric vehicles are an undeniable part of our transportation future. The U.S. Energy Information Administration (EIA) forecasts that electric vehicle sales will quadruple over the next thirty years.

Much like computers in the 1980s…

The internet in the 1990s…

or ecommerce in the 2000s…

We know that electric vehicles are coming. Cheap oil fields are being depleted as new battery technologies hit consumer markets. And nationwide charging networks will make these cars a practical alternative to internal combustion engines.

That’s especially clear when taking a look at Luke Lango’s recent presentation. In it, he details how a tiny $3 tech company could soar more than 40x over the next decade as the Apple Car changes the world in the 2020s like the iPhone changed the world in the 2010s.

… Interested? You can check out Luke’s full presentation here.

Meanwhile, one company also makes the Profit & Protection cut.

Lithium Americas (LAC)

Lithium Americas is a development-stage lithium mining firm with three projects in its pipeline. Its two brine resources in Argentina will come online in late 2022, while its Nevada mine at Thacker Pass should start producing by mid-decade.

There are four key reasons to consider the firm.

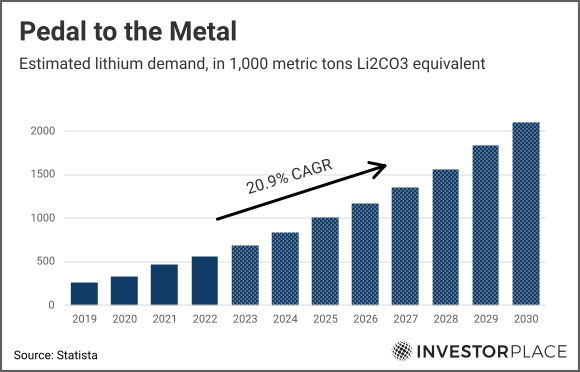

1. Rising Lithium Demand

Electric vehicle batteries will need a lot

of lithium metal — far more than the 90,000 tons currently produced annually.

That’s because a single electric vehicle requires anywhere from 10kg to 15kg of pure lithium metal — thousands of times more than what any cell phone or laptop battery uses. Automakers will need new-entrant miners like Lithium Americas to fill that gap.

Lithium is also a finite resource, setting a floor beneath prices. The U.S. Geological Survey estimates around 21 million metric tons of proven lithium reserves; if every automaker suddenly switched to making EVs, the world would run out of lithium in just two decades. Many analysts believe lithium prices should remain firmly in the $70,000 range per metric ton for the next decade.

2. Low-Cost Production

Lithium Americas will also enter as one of the world’s lowest-cost producers, an essential competitive advantage in the world of indistinguishable commodities.

The company’s brine flats in Argentina operate much like Sociedad Quimica y Minera de Chile’s (SQM). Miners pump brine through the lithium-rich ground and collect them in large ponds. The high deserts of Chile and Argentina — one of the world’s driest climates — eventually evaporate the water and leave lithium-rich salts behind for purification.

It’s a natural process that saves two-thirds or more in costs compared to open-pit mining. And though LAC’s operations will be slightly higher-cost than SQM’s, Argentina’s low taxes and royalties will keep prices competitive.

3. Undervalued American Assets

LAC also owns the rights to Thacker Pass, the largest known lithium resource in the U.S. It’s a geopolitically important asset that will help American battery producers reduce reliance on imported production from Australia, Chile and China.

Thacker Pass is admittedly a troubled asset. Lawsuits from environmentalist groups, ranchers and Native American tribes have long dogged the project, despite bipartisan political support for its go-ahead. LAC won the mining rights to the site during the Trump administration and received the final mining permits under the Biden one.

Nevertheless, these fears are now pricing LAC’s shares as if Thacker Pass will never produce an ounce of metal. Lithium America’s shares trade at under $25, valuing the company at 4.3 billion CAD.

That’s far too low, even if Thacker Pass fails to start.

Analysts at Morningstar now estimate that LAC’s Argentinian Cauchari-Olaroz project will produce more than 150,000 metric tons per year by 2030 and for Pastos Grandes to add another 24,000 metric tons. At an average price of $70,000 per ton, LAC and its partners will gross upwards of $12 billion in revenues annually, potentially netting LAC $1 billion annually.

Investors buying LAC shares will receive two Argentinian projects at a discount and an American one for free.

4. A “Picks-and-Shovels” Play

Finally, there’s LAC’s business:

A “picks-and-shovels” play on electric vehicles.

Today’s EV industry is a highly fragmented market. Motortrend counts no fewer than 36 different major and minor brands. Add in dozens of micro-mobility firms, 300 EV charging companies and plenty more auto part makers, and you have an industry with no clear winners besides those whose share prices have already “gone to the moon.”

Much like the U.K. “bicycle bubble” of the late-1890s where hundreds of bike manufacturers went bust, the next decade will see a massive shakeout among EV startups.

Meanwhile, low-cost lithium producers are far fewer in number. SQM is the leading low-cost producer, and LAC will soon join them as Argentinian sites come online. It’s a far more guaranteed business that deserves a place in the Profit & Protection list.

That’s because no matter which electric vehicle company becomes the next Tesla, the winners will still have to stand in line for their lithium supply.

The Electric Vehicle Firms Hiding in Plain Sight

If signed into law, Thursday’s reconciliation bill would require electric vehicles to have batteries made with at least 40% minerals extracted or processed in the U.S., or in a country with an American free trade agreement.

Lithium America’s Thacker Pass mine is an obvious beneficiary — provided production moves ahead.

But the firm isn’t the only winner of the bill. The legislation will also potentially do away with the 200,000 vehicle cap for the $7,500 electric vehicle tax credit. And next week, we will take a closer look at why that’s terrible news for Tesla…

… And who gains from it.