Instacart (NASDAQ:CART) has been one of the more intriguing IPOs of the past year. In September, CART stock went public at $30 per share, surging to nearly $43 as investors piled in. However, the stock has since fallen back below its IPO price to around $25, as the market reassesses the upstart grocery delivery platform’s valuation and growth prospects.

So, the key question many investors have is where CART stock will go over the next five years? Let’s dig deeper into its financials and future projections to gauge its potential.

Where Is CART Stock Heading in the Long Run?

Instacart’s early post-IPO price swings don’t reveal much about the stock’s long-term trajectory. As a newly-public company, Instacart lacks robust analyst coverage and the price history of more established names. Its limited trading period means we can’t rely much on technicals or past price action to determine the future direction of CART stock.

In my view, the $30 IPO pricing was too rich, given the uncertain economic environment and Instacart’s largely unproven business model. Thus, the stock’s current $25 level seems more sensible. However, considerable risks remain that could result in additional downside. As a newly-public firm, Instacart has a minimal track record to look at, making long-term growth estimates less certain. Plus, competition is heating up in the grocery delivery space from the likes of DoorDash (NASDAQ:DASH), Uber (NYSE:UBER), and smaller players.

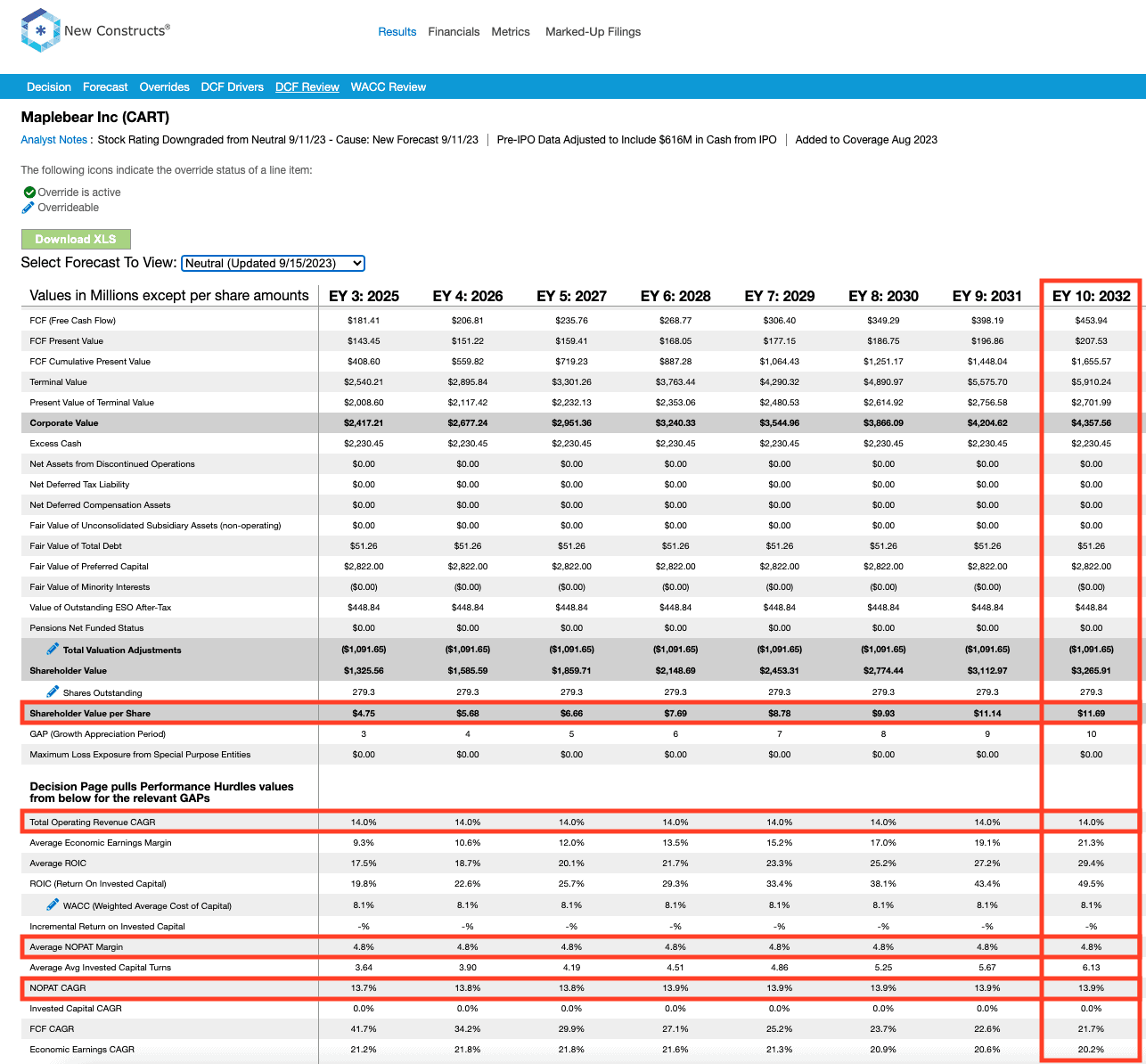

My position is that 4X gains to more than $100 per share seem unlikely in the next five years without Instacart significantly exceeding estimates. A reverse DCF analysis suggests the stock looks overvalued currently. Even assuming 14% annual revenue growth, the stock’s current fair value could be as low as

$11.69 per share. With more modest top-line expansion expected, CART stock may struggle to reach even $30 per share by 2028, based on these consensus forecasts.

{kind=link}

Can CART Stock Still Be a Multibagger?

If Instacart can achieve its targets, substantial share price gains are achievable. The company grew revenue at a 15% year-over-year clip last quarter, and is expected to reach 48 cents in earnings per share next year after producing losses in 2023. Longer-term estimates call for double-digit top-line growth for years to come, potentially reaching 10-15% annually in the 2030s. Profitability should improve markedly as well if scale is achieved.

Of course, Instacart could certainly beat expectations and post faster growth than projected. However, competition will likely intensify significantly in the coming years as grocers and delivery services target the same markets. From my perspective, Chinese e-commerce stocks seem to offer more attractive value in emerging tech currently based on their growth runways.

Therefore, I believe a reasonable 5-year price target range for CART is $25 to $35 per share, barring a major broad economic acceleration. While strong earnings growth is forecasted, revenue growth estimates appear insufficient to justify 4X stock price appreciation in my view. Ultimately, executing on projections within an increasingly competitive niche will prove challenging without dumping large sums into marketing.

The Bottom Line

In conclusion, while Instacart certainly has disruptive potential in the grocery delivery space, its long-term upside seems constrained relative to other tech names, in my opinion. Significant risks and uncertainties remain for this newly public company with a limited track record to assess.

While CART stock could certainly trade higher in 5 years, it is unlikely it will quadruple without major industry consolidation. Of course, investors must weigh Instacart’s prospects themselves and decide if the growth narrative seems sustainable. But my take is that expectations should be tempered for this emerging grocery delivery platform. Significant gains seem achievable, just not at the scale some bulls envision.

On the date of publication, Omor Ibne Ehsan did not have (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.