Growth stocks are needle-movers of the broader stock market these days, so it is essential for your portfolio to have exposure to them. Anyone not keeping a pulse on growth stocks is likely underperforming the market by a good margin or losing out entirely.

That said, most growth stocks right now are trading at nosebleed valuations. These stocks have significant downside potential if the market decides to correct, and their upside potential is driven a lot by the broader market’s momentum. However, there are many outliers, and I think many of them can deliver multibagger returns from their current valuations in the coming years. Here are seven to look into:

Sprout Social (SPT)

Sprout Social (NASDAQ:SPT) provides a platform for businesses to manage their social media presence. While the stock has been battered lately after a recent revenue miss, I believe the selloff is overdone, and Sprout Social remains poised for explosive growth ahead. It is now down around 75% from its peak.

In Q1 2024, Sprout delivered 28.7% year-over-year revenue growth to $96.8 million. The company also swung to profitability, posting adjusted EPS of 10 cents, which crushed estimates by 9 cents. However, its full-year 2024 outlook was mixed, with adjusted EPS of 45-46 cents, beating expectations but revenue guidance of $405-$406 million, slightly missing the $425.6 million consensus.

Despite the near-term hiccup, I’m convinced Sprout’s best days lie ahead. People spend more time on social media than ever, and Sprout is perfectly positioned to help companies maximize their presence. The company’s robust platform and AI capabilities give it a major competitive edge.

Although growth may moderate temporarily, analysts still expect Sprout’s earnings to quadruple between 2024 and 2028. With that level of profit expansion on tap, I believe Sprout could be a multibagger by 2026, even with a muted valuation multiple.

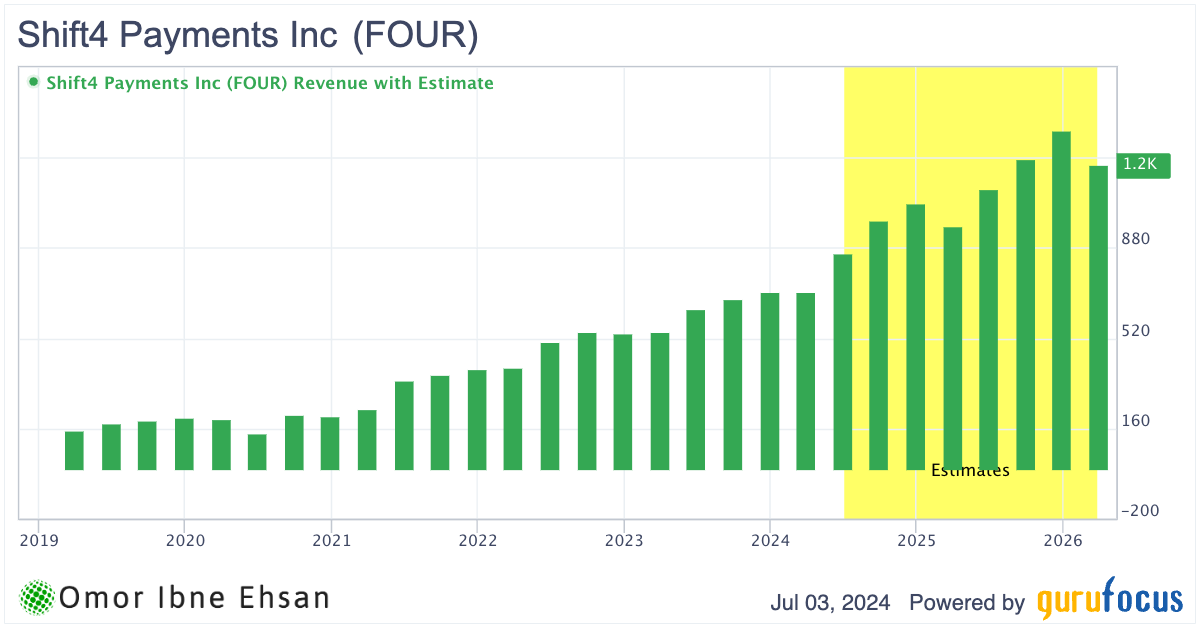

Shift4 Payments (FOUR)

Shift4 Payments (NYSE:FOUR) is a leading provider of integrated payment processing and technology solutions. While the company missed on both revenue and earnings in Q1, I believe the long-term growth story remains intact.

Revenue grew an impressive 29.32% YOY to $707.4 million, even though it fell short of estimates by $43.6 million. Shift4 is one of the fastest-growing fintech companies out there, with a three-year revenue CAGR of over 50%. Analysts are projecting a robust 41% sales growth for the full year 2024.

Click to Enlarge

The earnings miss of 8 cents, with EPS coming in at 54 cents, is certainly disappointing. However, most fintech stocks are trading at depressed valuations in the current market environment, and I believe Shift4 is no exception. The company has been aggressively pursuing M&A, spending over $1 billion on acquisitions since 2021. This has resulted in goodwill ballooning.

While this M&A strategy does introduce some risk, it’s also been a major growth driver. Shift4’s three-year total asset CAGR stands at an impressive 23.51%. In my view, the market is not giving the company enough credit for its strong growth trajectory.

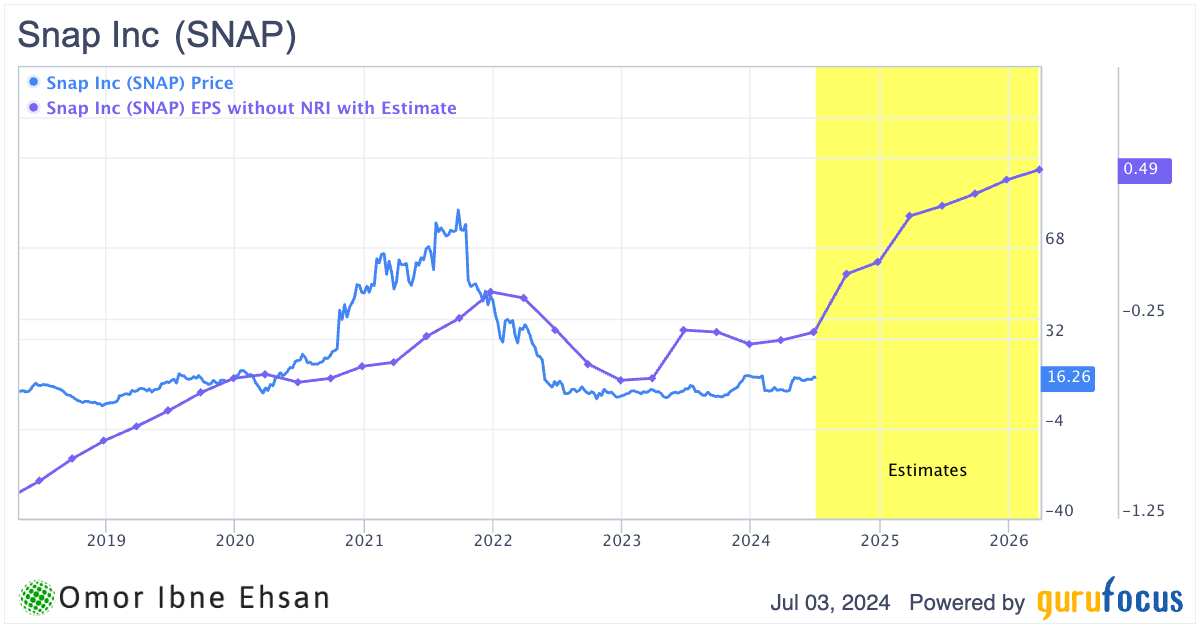

Snap Inc (SNAP)

Snap Inc. (NYSE:SNAP) operates as a camera and social media company. In my view, SNAP stock is one of the most underestimated names in the market right now, and it has explosive potential ahead.

I believe Snap is poised for a major recovery, similar to the impressive turnaround META pulled off from 2022 to today. That’s because Snap has been rapidly improving its fundamentals and has substantial room to boost profits going forward.

Revenue growth accelerated to an impressive 21% YOY in Q1, up sharply from just 5% the prior quarter. Meanwhile, Snap’s average revenue per user (ARPU) has remained relatively stagnant for years – but that’s precisely why I see immense untapped potential here.

Click to Enlarge

We could witness an explosive comeback if Snapchat can successfully grow this key ARPU metric and drive earnings higher in the coming years. Snap’s brand-safe environment and continued ad platform innovation position it well to capture rising demand.

Besides, you should consider the looming possibility of a TikTok ban. Given the significant audience overlap between the two platforms, this could drive floods of Gen Z and Millennial users onto Snapchat.

Super Micro Computer (SMCI)

Super Micro Computer (NASDAQ:SMCI) makes servers and storage solutions for data centers. The company is at the forefront of the AI revolution, and its stock could potentially soar much higher if the AI mania continues. In Q3 2024, Supermicro achieved record-breaking revenue of $3.85 billion, a staggering 200% increase YOY. Non-GAAP earnings per share also skyrocketed 308% to $6.65.

These impressive results reflect the strong demand for Supermicro’s plug-and-play AI solutions. CEO Charles Liang highlighted that the company continues to face some supply chain challenges due to new products requiring key components. However, the AI tailwinds appear to be overpowering these headwinds for now.

Supermicro’s stock has been consolidating for about four months after an explosive rally. I believe if the AI hype train keeps chugging along, we could see the stock break out to new highs. The valuation of 35 times forward earnings and three times sales is not excessive for a company growing at a triple-digit pace.

That said, investors should be aware that much of Supermicro’s upside potential is tethered to the sustainability of the AI boom. The stock could face a steep selloff if the AI narrative shifts or interest fades. But for now, I believe the risk/reward looks attractive for this AI hardware pure play.

GigaCloud Technology (GCT)

GigaCloud Technology (NASDAQ:GCT) operates a B2B e-commerce platform connecting suppliers and retailers of large parcel products. Despite its misleading name, this company’s business is growing at a breakneck pace, putting even many cloud companies to shame. In Q1 2024, GigaCloud nearly doubled its revenue YOY to $251 million, marking its fifth consecutive quarter of growth.

What’s powering this explosive trajectory? GigaCloud’s highly robust technology suite transforms how B2B buyers and sellers of oversized items connect and transact globally. Its supplier-filled retail model streamlines the entire supply chain journey. Strategic acquisitions of Noble House and Wondersign are further diversifying GigaCloud’s already impressive product and service offerings.

GCT stock has delivered a blistering 339% return over the past year, although shares have traded sideways since February. I believe GigaCloud could be poised for another major breakout if it continues to prove to investors that it can maintain this growth pace.

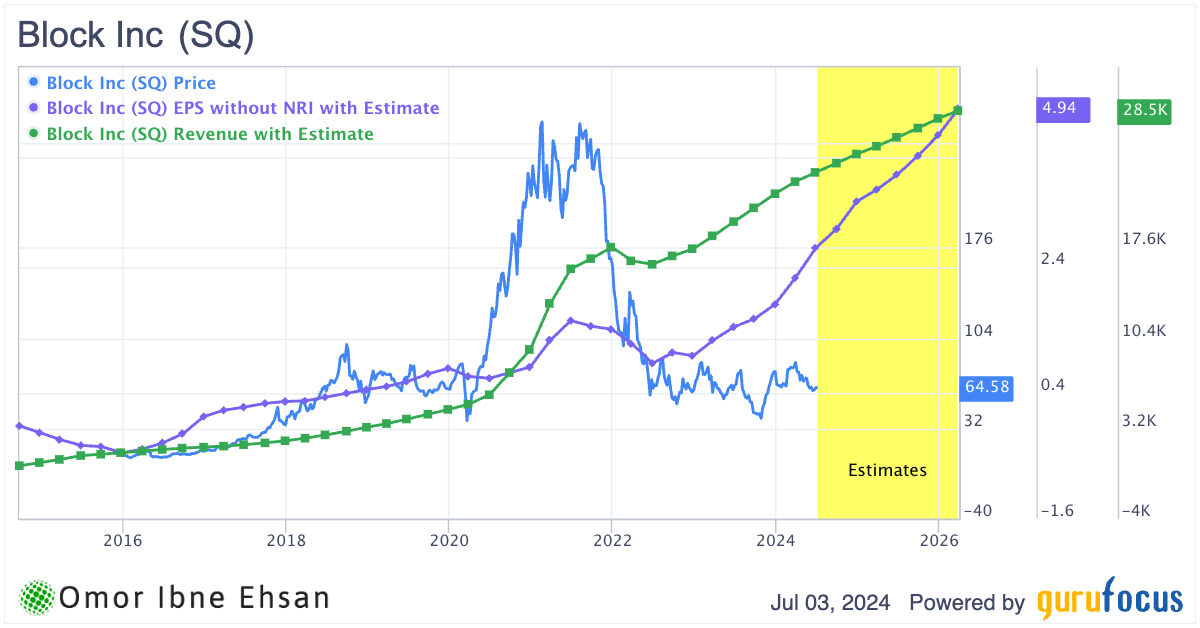

Block (SQ)

Block (NYSE:SQ) provides financial services and mobile payments solutions for businesses and individuals. The company just reported impressive Q1 2024 results, with EPS of 85 cents, beating estimates by 12 cents, and revenue of $5.96 billion, surging 19.4% YOY.

Block is one of the fastest-growing fintech companies in the market, and its depressed valuation looks too compelling to pass up at current levels. Despite drastically improving its fundamentals, SQ stock has traded sideways over the past two years.

Click to Enlarge

EPS is projected to double within the next four years. You’re essentially paying a mere 12 times 2026 estimated earnings at the current stock price.

Moreover, Cash App achieved 49% year-over-year gross profit growth, driven by strong momentum in Cash Card. With Cash App’s MAUs reaching 57 million, I believe there’s still a massive runway ahead for further monetization.

The stock won’t stay undervalued for long, as the market eventually realizes this fintech juggernaut’s immense profit potential.

Li Auto (LI)

Li Auto (NASDAQ:LI) designs and manufactures premium smart electric vehicles in China. This company was on fire just a year ago, smashing earnings estimates and rewarding workers for outperforming delivery targets. However, the tables have turned swiftly for Li Auto in 2024. The stock has plummeted 44% year-to-date after the company lowered delivery guidance and missed Q1 estimates, with EPS of 17 cents falling short of expectations by 3 cents. Revenue also disappointed, coming in at $3.54 billion and missing projections by over $250 million despite still growing an impressive 30.75% YOY.

While the near-term picture looks grim, I believe the intense selling pressure on LI stock has been overdone. This company remains one of the most popular EV brands in China and recently posted strong delivery numbers that hint at a potential turnaround. Li Auto delivered 47,774 vehicles in June, up 46.7% compared to last year. This brought Q2 deliveries to 108,581, a 25.5% YOY increase. As of June 30, Li’s cumulative deliveries reached 822,345 vehicles, ranking it first among emerging Chinese EV makers.

I’m optimistic that Li Auto could engineer a significant rebound. The company is insulated from Chinese EV tariffs and has ambitious international expansion plans. If Li can continue executing and regain its prior momentum, the stock looks poised for a sharp recovery.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or

indirectly) any positions in the securities mentioned in this article.