Growth stocks may not be the first thing on your mind right now, and I get it. Most growth plays are tied to tech or software, sectors that have faced immense pressure amid recession fears and a brutal tech selloff sparked by Big Tech’s disappointing results. To make matters worse, the Federal Reserve has held off on interest rate cuts far longer than anticipated. The market expects a cut in September, and I believe that’s when the Fed will finally budge. But if they move too slowly, more pain could be in store.

It’s also worth noting that most historical recessions have begun just as rates start to fall. Unemployment trends aren’t encouraging either, with the Real-Time Sahm Rule Recession Indicator crossing 0.53. This rule states that when the three-month moving average of the national unemployment rate exceeds the prior 12-month low by 0.5 percentage points or more, we’re in the early stages of a recession. The last occurrences? COVID and 2008.

Despite the bearishness, I believe some growth stocks can buck the trend. And even if they don’t, I’m optimistic about their long-term prospects. Let’s dive in!

Oscar Health (OSCR)

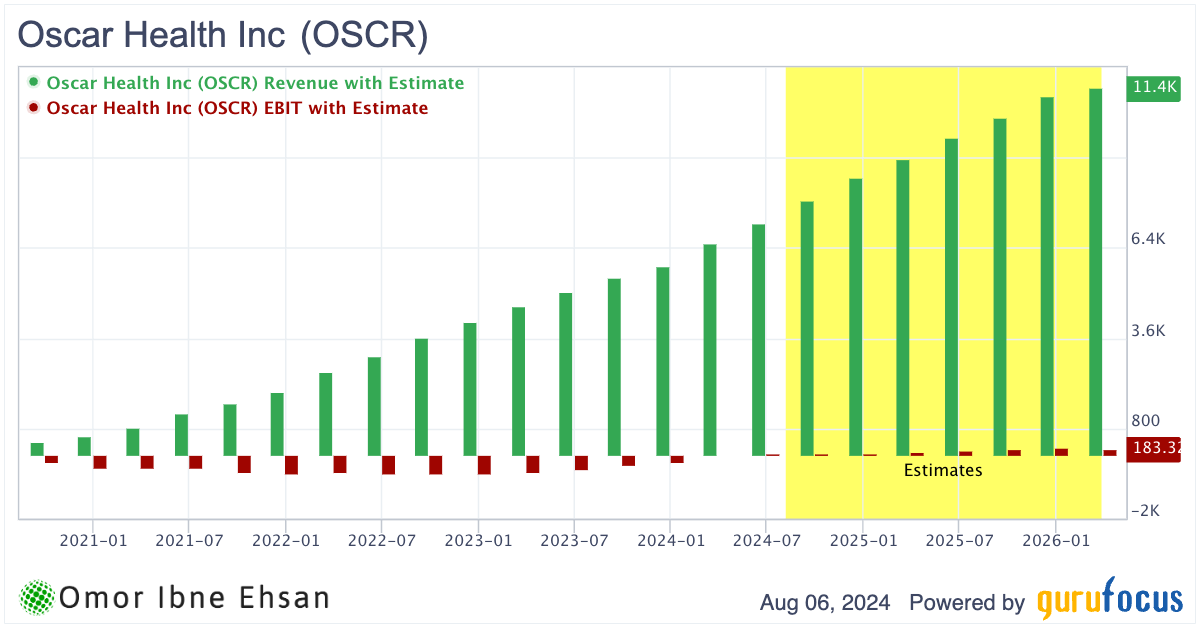

Oscar Health (NYSE:OSCR) provides health insurance plans and healthcare technology solutions. The company has been making waves lately with strong financial results and membership growth.

In Q1 2024, Oscar reported total revenue surged 46% year-over-year to $2.1 billion, driven by membership gains, higher premiums, and lower risk adjustment. Net income turned positive for the first time ever at $178 million. For the full year 2024, analysts forecast revenue will jump 48% to around $8.7 billion. This newcomer is expanding fast in the massive health insurance market. Trailing 12-month revenue could reach $11.4 billion.

Click to Enlarge

The stock has skyrocketed 123% over the past year as the financials impress. While still early in its growth trajectory, Oscar is expected to nearly double revenue again over the next three years to 2027. Earnings per share of 4 cents are estimated for 2024, projected to soar to $2.40 by 2027.

I believe Oscar Health is a promising growth stock to consider. Plus, the health insurance industry tends to be more insulated from economic and market volatility than many tech sectors. It’s a pretty solid growth stock.

AppLovin (APP)

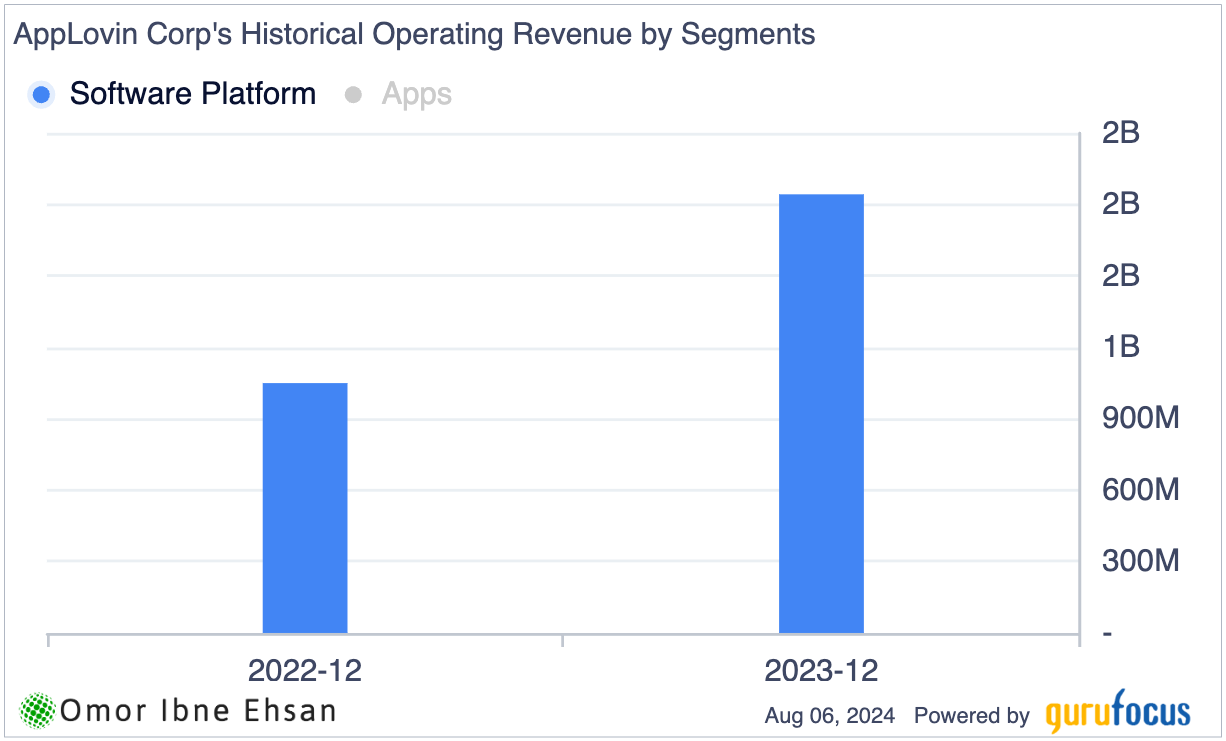

AppLovin (NASDAQ:APP) is a software platform that helps mobile app developers grow their businesses through marketing, monetization and analytics solutions. The company has been delivering impressive financial results lately, with Q1 2024 revenue surging 48% year-over-year to $1.06 billion, driven by a 91% jump in its software platform revenue to $678 million. That’s what is driving most of the growth.

Click to Enlarge

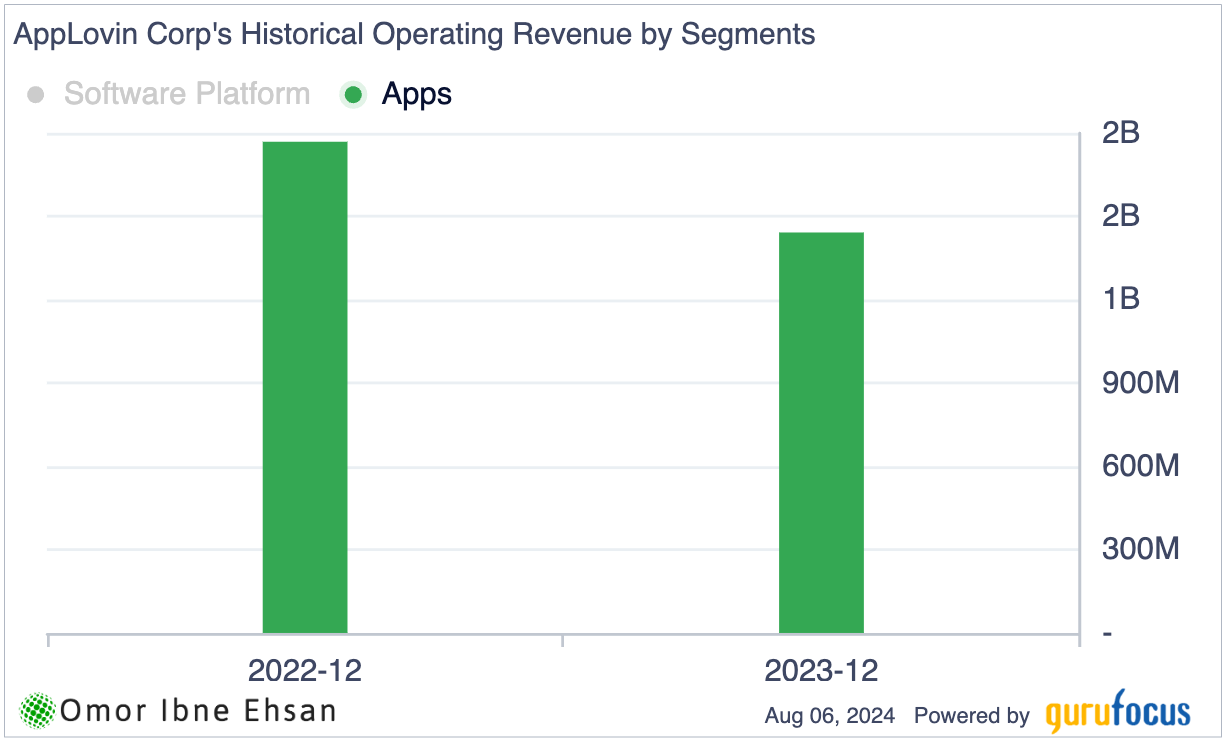

However, it’s not all rosy. Apps revenue has declined.

Click to Enlarge

Some analysts, like Mark Zgutowicz from Benchmark Co., maintain a “Sell” rating on the stock. There are also concerns about competition ramping up to challenge AppLovin’s success. Indeed, analysts do think that this growth will slow down significantly to around 11% top-line growth annually in the coming years.

That said, most analysts are bullish, with a consensus “Strong Buy” rating and an average price target of $101.89, implying 52% upside potential. BTIG recently raised its target to $114, seeing AppLovin as a top pick for H2 2024. Even if growth slows down, the margin growth should keep the stock trading at a premium.

While the complex business and YTD performance have made some investors cautious, I believe AppLovin’s growth prospects, reasonable valuation (23x forward P/E), and potential for margin expansion make it a compelling growth stock to consider for the long run. The recent pullback could present an attractive entry point for investors willing to dig deeper.

IAMGOLD (IAG)

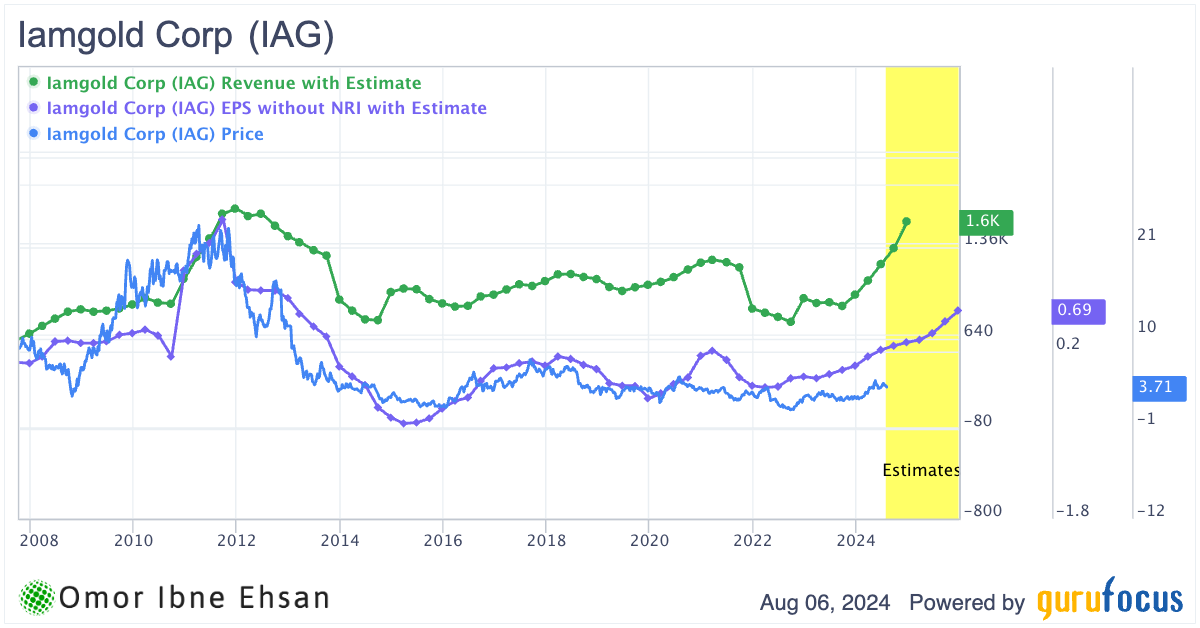

IAMGOLD (NYSE:IAG) is an intermediate gold producer operating mines in North America and West Africa. The company started 2024 with very strong performance, reporting attributable production of 151,000 ounces in Q1, driven by stable operations and positive grade reconciliation at its Essakane mine, as well as record production at its Westwood mine since restarting in 2021. IAMGOLD stock is up 53% in the past year, largely due to gold prices performing significantly better than expected in recent quarters, even as other equities have declined.

I believe rising gold prices could drive IAMGOLD shares even higher in the long term as the company benefits from increased profitability. If it meets analyst estimates, it could double or more.

Click to Enlarge

However, keep in mind that gold is ultimately a commodity, and prices are unpredictable. For long-term investors though, betting on gold via IAMGOLD could prove quite profitable, as the precious metal is unlikely to disappoint over an extended horizon.

While most analysts currently have a “Hold” rating on the stock with an average price target of $4.8, implying a 30% upside, IAMGOLD’s future looks bright with the Côté Gold mine in Canada ramping up production. If you’re bullish on gold, IAMGOLD provides solid exposure and growth.

Pan American Silver (PAAS)

If you’re betting on gold, why not consider silver too? Silver prices surged nearly 40% from February to July but have pulled back 12.5% recently. I see this as a buying opportunity, as gold’s strength could drive a second silver spike with investors seeking safe havens. Pan American Silver (NYSE:PAAS) stock has tracked silver prices, spiking and then retreating lately, but I believe a long-term position could pay off handsomely.

Pan American Silver is a leading silver mining company with operations across the Americas. The company reported strong Q1 2024 results, with silver and gold production within guidance ranges and lower costs, generating $133.2 million in operating cash flow.

Analysts are bullish, expecting PAAS’s EPS to soar from 66 cents in 2024 to $1.62 in 2026 on expanding margins. The average price target of $25.59 implies 19% upside. While one analyst recently lowered their target, most maintain buy ratings.

However, there are risks to consider. The ILO consultation process at the Escobal mine in Guatemala has faced delays under the new government. PAAS is also exposed to volatility in silver prices and operating challenges like grade variability at certain mines. But all-around, I’m optimistic about PAAS as a leveraged silver play with strong fundamentals and growth potential. The recent pullback looks like an attractive entry point for patient investors.

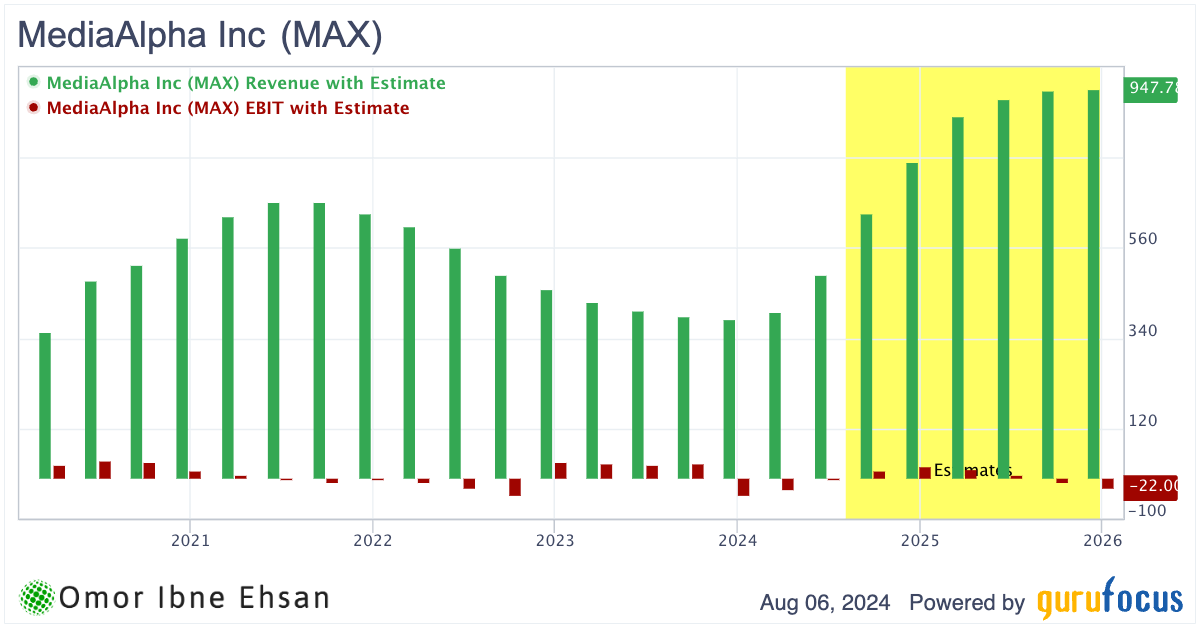

MediaAlpha (MAX)

MediaAlpha (NYSE:MAX) operates an insurance-customer acquisition platform in the United States. The company has been delivering hypergrowth levels of top-line growth as companies have greatly expanded their advertising and marketing budgets in the past two years. MediaAlpha beat Q2 sales estimates by over 18% and while MAX stock has been quite volatile this year, it is still up 78% in the past 12 months.

Of course, a recession could force companies to start scaling back their advertising expenditure, but I think it’s worth paying more attention to MediaAlpha since it is a key partner of insurance companies. Insurers generally have very sticky financials, so I expect that stickiness to extend to MediaAlpha somewhat, even if the economic downturn does get worse.

William Blair analyst A. Klauber recently boosted his Q3 2024 EPS estimate for MediaAlpha to 10 cents, up from 4 cents previously. The company is guiding for impressive Q3 revenue growth of 290% year-over-year at the midpoint. While there are some risks around the ongoing FTC inquiry into its marketing practices, I believe the long-term growth story remains intact for this adtech leader in the insurance space.

I would also like to point out that most of the upside will likely come from a sales rebound. Profits are unlikely to go up much.

Click to Enlarge

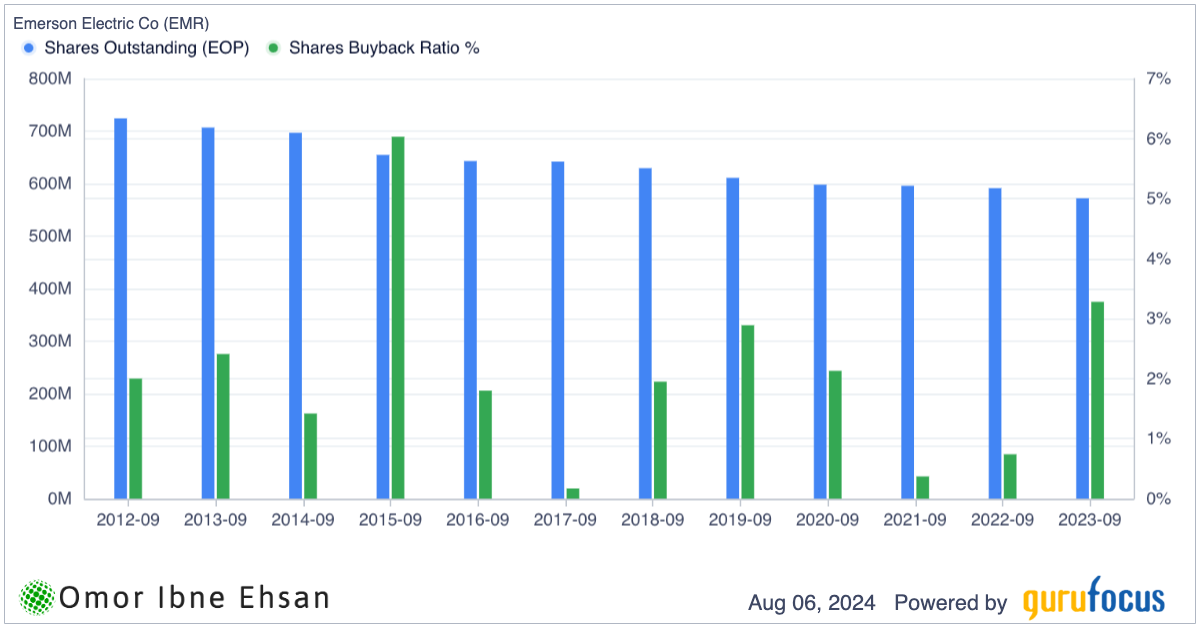

Emerson Electric (EMR)

Emerson Electric (NYSE:EMR) is a global technology and engineering powerhouse that manufactures products and provides services for industrial, commercial and consumer markets. The company has been executing exceptionally well, with strong sales growth, operating leverage and earnings in its latest quarterly results.

I believe Emerson Electric has tremendous staying power as a large, well-established company with a long history in the stock market. The stock has performed impressively, rising 79% over the past five years, and I think it will continue to excel in the coming years if industrialization trends persist. Emerson is benefiting from the surge in infrastructure spending and industrialization, along with an influx of workers from abroad.

While the current economic downturn could present some headwinds, I don’t expect the tech selloffs to significantly impact industrial companies like Emerson. Analysts seem to agree, with the consensus rating being a “Strong Buy” and an average 12-month price target of $130, suggesting potential upside of over 19%.

Newmont (NEM)

Newmont (NYSE:NEM) is a mining company that has been riding the wave of rising gold prices lately, and I think it’s worth taking a closer look at for your portfolio. While gold is their main focus, they also mine other valuable metals and rare earth materials that I’m quite bullish on for the long haul.

Despite the recent market turbulence dragging down stocks, NEM has surged over 50% from its February lows. Why? Well, they just delivered one of the most impressive earnings reports I’ve seen in a while. Newmont crushed EPS estimates by almost 40% and beat revenue expectations by 26.2%. Speaking of revenue, it skyrocketed 64% year-over-year. It’s also a buyback machine.

Click to Enlarge

Analysts expect breakneck growth to moderate, but they still see robust gains ahead, with around 20% annual EPS growth and 10% yearly revenue increases. At current prices, NEM looks like a bargain if it can deliver anything close to those projections. However, I’d take those estimates with a grain of salt, as commodity prices can be fickle.

All that said, I’m optimistic about where gold is headed, so I believe Newmont deserves a spot on your watchlist. You can sit on its 2% dividend yield as it rises.

On the date of publication, Omor Ibne Ehsan did not hold (either directly or indirectly) any positions in the securities mentioned in this article. The opinions expressed in this article are those of the writer, subject to the InvestorPlace.com Publishing Guidelines.

On the date of publication, the responsible editor did not have (either directly or indirectly) any positions in the securities mentioned in this article.