A new twist in the K-shaped economy… why Luke Lango says the Iran war will widen the K’s spokes… a new divide emerging inside AI itself… beware the growing danger in private credit… and what it’s all telling us about the future of AI

The top arm of the ‘K’… represents the top 20% of high-income households—but nearly half of them could be walking on eggshells…

That line comes from a Fortune article earlier this week. And it hints at something quietly shifting beneath the surface of what we thought we understood about who’s doing well financially today.

Here’s the short version: today’s K-shaped economy, where asset owners thrive while wage-dependent households struggle, has developed a new fracture – a divide forming within the “haves” themselves.

Back to Fortune:

The wealthy who are at financial risk are “high earners whose lack of budgeting and profligate spending has them overleveraged and exposed…

While they appear to be doing well from the outside, they are only a step away from real financial trouble.”

According to Fortune, those wealthy enough to be insulated from this “real financial trouble” have a new name – the “secure elites.”

Now, there’s a fascinating parallel playing out in today’s stock market. But before we explore that, let’s start with the market’s equivalent of the K-shaped divide…

AI versus everything else.

Get ready for the K-shaped stock market to widen

Longtime Digest readers know this story well.

On one side of the market, we have “yesterday’s economy” stocks (minus oil recently) – companies that haven’t kept pace with rapid technological advances.

On the other side, we have AI and the companies powering it, marching higher on the back of massive capital investment and explosive earnings growth.

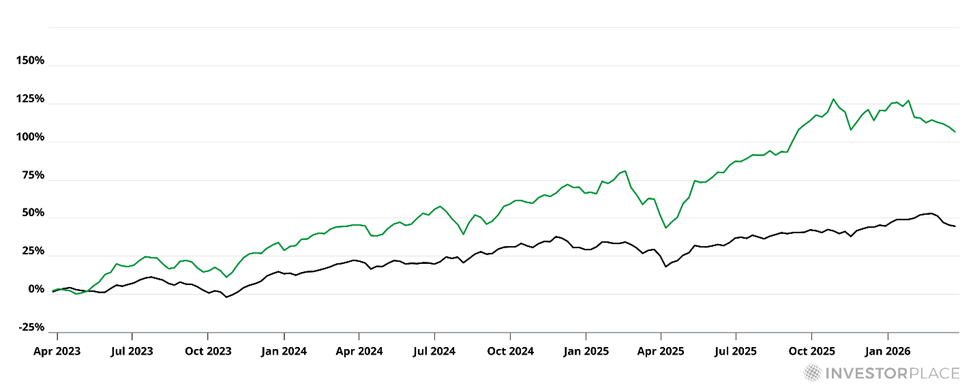

To illustrate the performance gap, the chart below shows the Equal Weight S&P 500 up roughly 40% over the past two years while the Global X Artificial Intelligence & Technology ETF (AIQ) has surged more than 100% over the same period.

To be clear, “non-AI” stocks haven’t done poorly – they’ve just lagged. And that divide has defined this market.

According to hypergrowth expert Luke Lango, editor of Innovation Investor, this lag isn’t going away. If anything, he believes the current macro uncertainty will make it more pronounced:

Yes, the war will end. But, no, everything won’t go back to ‘normal’.

The consumer, already struggling… faces a sustained energy cost premium and a credit environment that stays restrictive longer than pre-war expectations suggested.

These are real headwinds for real businesses. The broad market…faces genuine pressure from the lingering war aftermath that doesn’t disappear on ceasefire day.

But Luke says it’s different for the AI sector.

Hyperscaler capex decisions are made on 5 to 10-year return horizons – irrespective of glum consumer sentiment surveys…

Microsoft and Google aren’t cutting AI data center budgets because American workers haven’t gotten a raise recently…

And Brent crude settling at $75 instead of $65 won’t influence Nvidia’s $1 trillion in confirmed orders.

Luke concludes:

Sophisticated capital with perfect industry information is making decade-scale [AI] commitments in the middle of a war.

That is the revealed preference of people who know more than the macro noise suggests…

Buy AI infrastructure into the chop. Stay cautious on the consumer-exposed broad market.

Stepping back, the takeaway is familiar – but important…

We still have a K-shaped market. And based on Luke’s analysis, today’s macro uncertainty will likely only reinforce that outperformance of technology versus “the rest.”

But here’s the new wrinkle…

Even within AI, a new divide is forming.

Let’s return to that Fortune framing for a moment…

Within the upper K of the economy, we have the “secure elites” – households with strong balance sheets, low debt and genuine financial resilience. Yet there are also the high earners who look financially healthy but are “only a step away from real financial trouble.”

There’s a similar dynamic playing out within AI.

On the “secure elite” side are the companies at the center of the AI buildout – the chipmakers, the data center suppliers, the infrastructure players. These companies are seeing enormous, visible demand. Orders are locked in. Capital is committed. Revenues are surging.

Whether consumer-facing AI products ever make one dime in profit won’t matter for the revenues of the “secure elite” over the next three-to-five years, as the hyperscalers pour billions into the rollout of AI infrastructure.

But move one step away from that core and the picture starts to change…

How much are people willing to pay for AI?

That’s the question the market is only now beginning to ask seriously.

Let’s start with the obvious…

The purpose of all that AI infrastructure isn’t just “to exist” – it’s to power applications that people and businesses are willing to pay for. But this is where the story starts to break down.

The part of AI that consumers actually use – the part they’re expected to pay for – is software. Models. Interfaces. Tools that help users write, design, analyze and automate.

But while the physical infrastructure of AI is generating real profits today, the software running on top of it is running into economic headwinds. And the evidence is starting to accumulate…

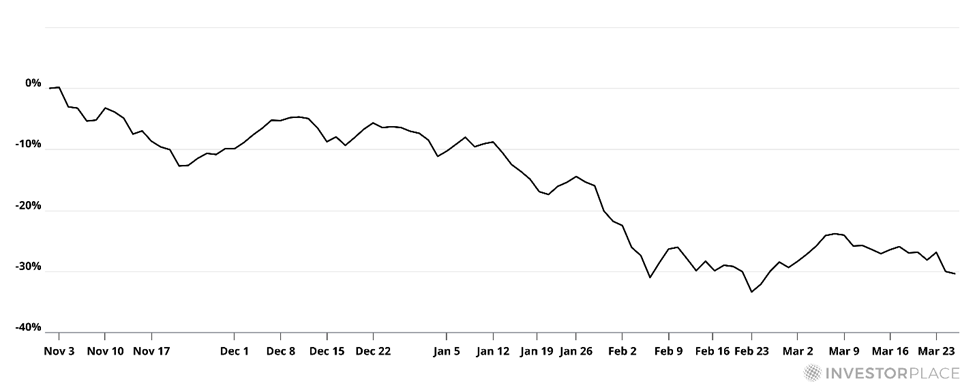

Since late October, the iShares Expanded Tech-Software Sector ETF (IGV) has fallen 30%.

Meanwhile, companies like Salesforce (CRM), Workday (WDAY) and UiPath (PATH) have each suffered double-digit drops as investors reassess their place in the AI story.

What makes this shift notable is that, until very recently, many of these same companies were viewed as core AI beneficiaries – not fringe players, but the “AI upper K,” central to the trade.

Investors grouped them alongside the infrastructure names, assuming they’d ride the same wave of demand and monetization.

That assumption is cracking.

Axios recently highlighted a study from MIT researchers examining hundreds of AI initiatives. Their conclusion: despite tens of billions of dollars in spending, the vast majority of organizations have yet to see a meaningful return.

That doesn’t mean AI won’t deliver. But it does mean the timeline – and the economics beyond today’s physical AI rollout – remain genuinely uncertain.

The clue that tells us this is real – private credit

Now, a software true believer might say, “Jeff, a 30% drawdown in IGV is just froth coming out of the market. It doesn’t mean software isn’t a secure elite.”

Fair.

So, let’s shift our focus away from stock prices to operational cash flows.

We’ll do this by looking at the private credit market. This is a corner of the financial system we’ve been tracking in the Digest alongside legendary investor Louis Navellier – and it’s worth understanding, because it connects directly to what’s happening in AI software.

Private credit is, in simple terms, lending that happens outside traditional banks. Instead of a company borrowing from JPMorgan, it borrows from a private fund – often at higher interest rates, with fewer public disclosures and less liquidity for investors who put money in.

For years, major private credit funds – including Blue Owl Capital (OWL), Blackstone (BX) and Ares Management (ARES) – poured billions into software companies, betting that steady subscription revenues would make them safe, reliable borrowers.

But in recent months, what some are calling a “SaaS-pocalypse” has cast doubts about AI’s real winners and losers.

Many of these software companies are finding that actual cash flows from their AI products aren’t strong enough to cover their debt obligations. Customers are building their own tools, questioning expensive software upgrades or simply not renewing. The numbers are sobering.

Here’s Business Insider:

The specter of AI disruption of the software sector could send defaults in private credit soaring to their highest level since the pandemic, Morgan Stanley said…

Defaults in the direct lending space could soar to 8%, the strategists estimated, nearing the peak default rate seen during the pandemic.

The trend will largely be driven by the disruptive effects of AI on software companies, they added.

That cash flow strain is rippling through the funds that financed these companies – and investors are feeling the heat.

As we highlighted in yesterday’s Digest, some credit funds have begun “gating” withdrawals. In other words, investors who assumed their money was accessible are now being told they may have to wait months or longer to get it back.

Louis believes the worst is yet to come:

For the past year and a half, I’ve been warning folks about one of the biggest risks in the financial system – one that has been hiding in plain sight.

Private credit.

Wall Street has been able to paper over some of the stress – extending loans, restructuring terms and pushing problems a little further into the future. But that kind of “extend and pretend” strategy only works for so long.

Sooner or later, the market is forced to confront which assets are sound, which loans are impaired and which borrowers were never built to make it through a tighter credit cycle.

I believe the private credit market is approaching a real moment of truth.

Now, it’s not all bad. Louis argues that in every crisis, money doesn’t disappear – it just moves from weak balance sheets into high-quality, cash-rich, low-debt “fortress” stocks.

He’s just released a deep dive into the growing cracks in private credit that details not only how to protect your portfolio, but how to benefit as this crisis redirects enormous currents of capital through the financial system.

Bottom line: If you’re in a credit fund that has software exposure, I hope you’ll make time to watch it.

Coming full circle

At the top of this Digest, Fortune described the financially vulnerable wealthy as “high earners whose lack of budgeting and profligate spending has them overleveraged and exposed…only a step away from real financial trouble.”

The private credit funds that financed the AI software boom were, in their own way, lending to that exact profile: companies that looked like stable, subscription-driven businesses on the outside…but were quietly burning through cash and over-leveraging under the surface.

Today, both groups are in trouble – the software borrowers who aren’t generating returns sufficient to repay their loans, and the funds that bet they would.

So, just as we now have a new “secure elite” within the upper tier of households, we’re seeing a similar divide within AI itself. We see it in the strength of infrastructure names…the weakness across software…and the increasing stress in the private credit markets that financed that growth.

It’s all the same story – just showing up in different places.

This leaves us with a simple but important shift in how to think about this market…

We can no longer just “own AI” – and certainly not blindly lend to it.

After all, in a K-shaped market, the difference between being in the “secure elite” versus everything else can have profound consequences for your portfolio.

One last thought before we go…

If the world is paying trillions to build AI…but AI is struggling to pay back its loans, at what point do we ask whether the hyperscalers will ever see a real return on that investment?

And perhaps more unsettling: what if the honest answer to “how much will the world actually pay for AI” turns out to be far less than investors currently assume?

Have a good evening,

Jeff Remsburg