Listen to the audio version of this article (generated by AI).

Alphabet says AI demand is outrunning supply … AWS logs its fastest growth in four years … Meta beats but pulls back 10% … and the capex canary sings louder than ever … Eric Fry’s latest on where to invest in AI today

We are compute constrained in the near term.

Our cloud revenue would have been higher if we were able to meet the demand.

That was Alphabet’s CEO Sundar Pichai on last night’s earnings call – and it speaks directly to the question we posed in Monday’s Digest.

The numbers that followed were genuinely impressive – across the board. But as with most things in this AI story, there’s more to it than the headlines suggest.

On Monday, we presented last night’s cluster of Big Tech earnings not as a test of individual companies, but as a diagnostic on the AI trade itself. We said there were two issues to watch: revenues, as a signal of whether AI-driven demand is actually materializing, and capex, as a signal of whether conviction in that demand is holding.

Now that the numbers are in, here’s what we learned…

Massive revenue growth across the board

Let’s start with Alphabet (GOOGL).

Google Cloud revenue surged 63% year-over-year to $20.02 billion – well ahead of the $18.05 billion Wall Street expected. Total revenue came in at $109.9 billion versus the $107.2 billion consensus, with net income up 81% from a year ago.

It was a blockbuster performance, putting the Pichai quote above in an important context. He wasn’t just spouting the usual CEO earnings-call optimism – he was highlighting a real supply constraint.

Google Cloud, acting as the company’s primary AI revenue engine, didn’t merely beat expectations – it was demand-limited.

From Pichai:

Our enterprise AI solutions have become our primary growth driver for cloud for the first time in Q1.

That’s a stronger enterprise AI demand signal than generic cloud growth – but I’ll note that it still sits closer to the infrastructure layer than a pure end-user monetization signal. I’ll get more into this distinction shortly.

Shifting to Microsoft (MSFT), its revenue came in at $82.89 billion, versus the $81.39 billion expected, with adjusted EPS of $4.27, versus the $4.06 estimate. Azure and other cloud services grew 40% – ahead of the 38.8% to 39.3% analyst range.

Another strong performance.

Meanwhile, the enterprise adoption numbers are striking. GitHub Copilot now has over 26 million users, and over 90% of the Fortune 500 is using Microsoft 365 Copilot. Commercial bookings jumped 112% year-over-year, driven by Azure commitments from OpenAI.

Turning to Amazon (AMZN), it delivered the most dramatic acceleration of the group.

Amazon Web Services (AWS) grew 28% to $37.59 billion – the fastest pace in 15 quarters, up from 24% last quarter. Total revenue of $181.52 billion crushed the $177.3 billion consensus, and EPS of $2.78 obliterated the $1.64 expectation.

One number to highlight is Amazon’s chip business. Graviton, Trainium, and Nitro combined have now exceeded a $20 billion annual revenue run rate, growing triple digits year-over-year.

Finally, Meta (META) beat on revenue – $56.31 billion versus $55.45 billion expected, up 33% from a year earlier and the fastest quarterly growth since 2021. Plus, adjusted EPS of $7.31 topped the $6.79 estimate.

Still, shares are down about 10% as I write on Thursday because daily active people came in at 3.56 billion, below the 3.62 billion Wall Street projected and more than 5% below Q4.

The company partly attributed the decline to internet disruptions in Iran, which is a genuine factor. Whether that fully explains the miss or masks something more structural is a question worth watching over the next quarter or two.

Enterprise growth is real, but here’s what it does and doesn’t tell us

Across all four companies, demand is strong and accelerating – but it’s worth being precise about the nature of these revenues.

Much of it is enterprise AI deployment: companies paying to build, train, and run AI systems. That is genuinely encouraging and more advanced than it was even two quarters ago.

But enterprise demand is also a messy signal…

Some of what’s driving these numbers is durable deployment. Some is still experimentation, pilot programs, and capacity being built ahead of demand that hasn’t fully arrived yet. At this stage, the earnings don’t cleanly separate those outcomes.

And either way, the “end user” here is overwhelmingly corporate. That’s an entirely different story from ordinary people opening their wallets for AI products in their daily lives.

That market – the Regular Joe who decides every month whether an AI subscription is worth keeping – is still largely unproven at scale.

So, what’s our best window into that demand?

OpenAI remains the clearest window into the consumer side

It doesn’t report earnings, but as we covered on Tuesday, OpenAI has reportedly missed internal usage and revenue targets due to massive compute costs and rising competition.

It has a real and growing enterprise business – ChatGPT Enterprise, API revenue, and deep integration with Microsoft’s product suite. But consider the scale of its infrastructure commitments: OpenAI has obligated itself to $250 billion in Azure spending alone – and that figure doesn’t even include the broader compute costs its own operations require.

At that scale, even strong enterprise growth may not be enough to close the loop. Consumer monetization isn’t a nice-to-have – it’s a necessity.

The evidence that it’s arriving at scale remains thin. That’s the gap last night’s strong enterprise numbers didn’t resolve.

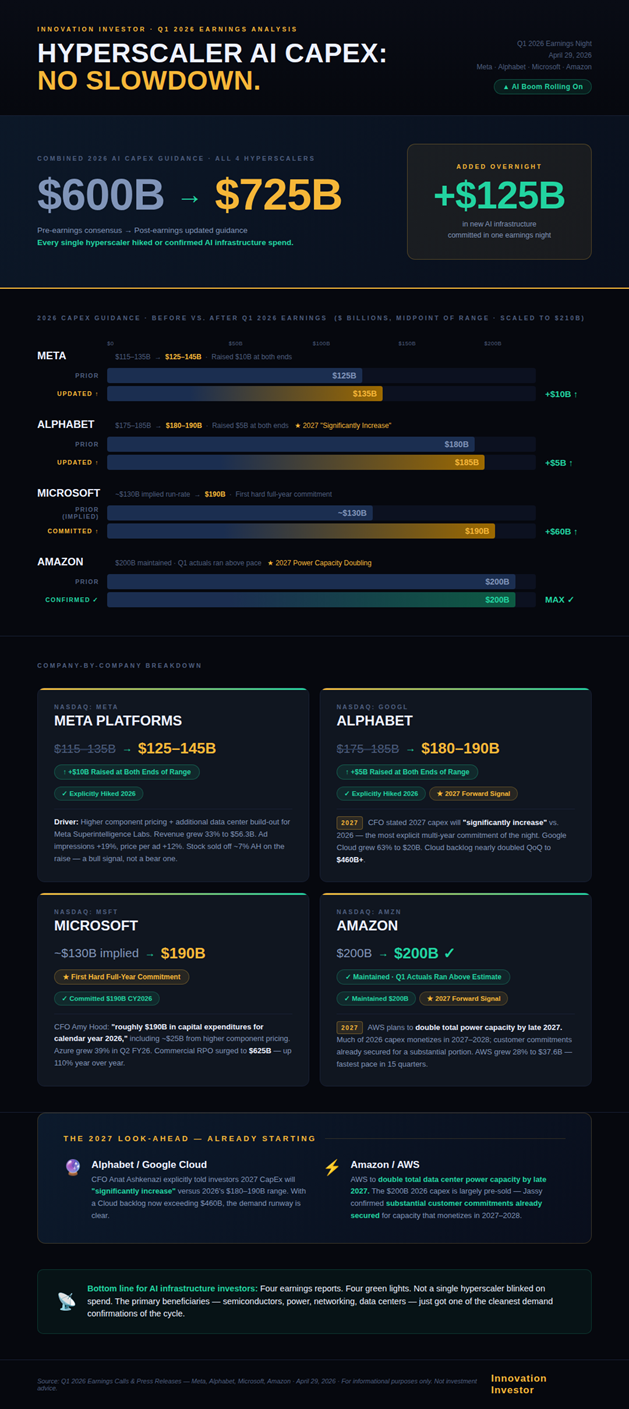

Shifting to our capex question: the canary didn’t just survive – it sang louder

On Monday, we said the “canary” worth watching was whether any hyperscaler quietly signaled doubt by dialing back investment. This wasn’t our prediction for last night – we flagged the capex canary as a longer-term watch item, not an imminent threat.

But was there not even the faintest glimmer of that signal: three of the four raised their spending commitments, and the fourth held firm on a $200 billion full-year plan.

Microsoft’s quarterly capex actually came in below estimates – $31.9 billion versus the $35.3 billion consensus – but paired that undershoot with a full-year guide of $190 billion, well above the $154.6 billion analysts had expected. The message: more conviction overall, just on a more deliberate quarterly cadence.

Alphabet raised its full-year range to $180 to $190 billion, up from $175 to $185 billion previously, and CFO Anat Ashkenazi told analysts to expect 2027 capex to “significantly increase” from there.

Meta raised its 2026 range to $125 to $145 billion, up from $115 to $135 billion, citing higher component pricing.

Finally, Amazon is holding firm on its $200 billion commitment.

Add it up, and you’re looking at somewhere north of $700 billion in combined 2026 capex across these four companies.

That’s not just a vote of confidence in AI’s potential, it’s a multi-hundred-billion-dollar bet that demand is real and growing.

Here’s a chart our hypergrowth expert Luke Lango sent me that summarizes the numbers:

Bottom line: the capex picture is increasingly clear. The returns picture is where it gets more nuanced.

So where does all this leave us?

In a better place than the skeptics expected, but a more nuanced place than the bulls may admit.

The infrastructure layer delivered genuinely good news last night. Cloud demand is real, accelerating, and in some cases supply-constrained – even if it doesn’t yet tell us cleanly how much of that demand will translate into durable end-user monetization.

But what we didn’t learn last night is whether the current wave of enterprise AI adoption is primarily a cost-cutting story from Corporate America or the beginning of a genuine new revenue-generation story.

Right now, the evidence leans toward efficiency: companies using AI to do more with fewer people. That’s valuable. But cost-cutting has a ceiling.

What we’d rather see is AI generating entirely new revenue streams rather than trimming existing costs – something that hasn’t yet shown up clearly in the numbers.

Bottom line: Last night’s numbers were strong. They confirmed the infrastructure bet is real. What they didn’t do is prove that the returns will match the investment.

Which brings us to a question that the $700 billion capex number raises…

If the builders are spending at this scale, who actually captures the return?

Our global macro expert Eric Fry of The Speculator has spent months studying how major technology booms play out – and his conclusion adds a layer of complexity to last night’s numbers.

His research shows that in every major tech cycle, from railroads to the internet, it’s rarely the infrastructure builders who capture the lasting gains.

As Eric puts it:

The builders struggled. The appliers got rich.

He points to Cisco – the poster child of internet infrastructure — which lost roughly 85% of its value after the dot-com bubble burst and took decades to recover.

The company that best used Cisco’s wreckage?

Amazon – up more than 100,000% from its early days.

Eric believes that same rotation – from AI Builders to AI Appliers – is beginning now. In his new free presentation, he names the stocks he’d sell and the overlooked companies he believes capture the next phase.

You can check it out right here.

Coming full circle, we’ll end on this…

The AI trade is real. Whether it’s as profitable as it is powerful is the question that will define the next few years.

Have a good evening,

Jeff Remsburg