Listen to the audio version of this article (generated by AI).

April inflation comes in hot… why Louis Navellier doesn’t expect relief at the pump anytime soon… but he’s bullish on this corner of the market… Luke Lango says the market’s divergence is getting worse… the “Summer of Stagflation”

This morning’s April Consumer Price Index (CPI) report revealed the hottest annual inflation rate since May 2023.

The figure came in at 3.8% – up from 3.3% in March, and above the 3.7% estimate.

The obvious culprit is energy. Costs have jumped almost 18% year over year, the steepest annual increase since September 2022. Gasoline is up 28.4%, and fuel oil has surged 54.3%.

But the higher prices aren’t limited to energy…

Shelter costs also ticked higher, rising 3.3% versus 3% in March. Food was up 2.3%. And airline fares jumped 2.8% for the month alone, putting the 12-month gain at 20.7% – a number that hits anyone planning a summer trip right in the wallet.

Overall, core inflation (which strips out food and energy) edged up to 2.8% year over year. That’s higher than the March reading of 2.6% as well as the 2.7% forecast. But it’s the monthly reading that really matters – core prices rose 0.4%, nearly double the 0.2% pace reported in both February and March.

That number is worth noting because when core starts accelerating, it means the energy shock isn’t staying in its lane – it’s bleeding into the broader economy.

For consumers, the math is troubling…

Wages aren’t keeping pace, credit card balances are near record highs, and now the monthly cost of just living – gas, groceries, rent – is climbing again. This morning’s data explains why last Friday’s University of Michigan Consumer Sentiment Survey reported the lowest reading since it began tracking the data in 1952.

Bottom line: It looks like we’ve reached the inflection point where the Iran conflict broadens from being just a geopolitical story to a kitchen-table story.

Unfortunately, we shouldn’t expect any relief on oil prices soon

That’s the bottom line from legendary investor Louis Navellier – a reality that’s weighing on cost-conscious drivers, inflation-worried investors, and businesses already grappling with elevated transportation and input costs.

Let’s jump to Louis’ latest issue of Breakthrough Stocks from last week:

I don’t anticipate any price relief in crude oil prices or at the pump until October, when worldwide demand naturally declines.

A peace deal and the full reopening of the Strait of Hormuz would also lead to a decline in energy prices, but even when that happens, it will take some time before prices drop back to pre-conflict levels.

How long could that take?

Here’s MarketPlace:

The general rule is it’s going to take as much time as the outage duration, Rystad Energy chief economist Claudio Galimberti said.

So, if it’s out two-and-a-half months, it will take another two-and-a-half months to get back to normal.

We’re still dealing with the supply disruption, so estimates are of little value. But we can say the market probably won’t see oil back in the $60s anytime soon.

That’s important because sustained high energy prices create problems for consumers and Wall Street alike. Which naturally raises the question Louis posed to readers:

So, what should investors do in this environment?

Follow the money

In Louis’ issue, he highlighted the acceleration in CapEx spending from Alphabet (GOOGL), Amazon (AMZN), Meta Platforms (META) and Microsoft (MSFT) on their earnings calls two weeks ago:

Analysts expected these four hyperscalers to spend about $670 billion on AI in 2026.

After the reports, that estimate jumped to $725 billion. And spending is expected to accelerate further in the years ahead.

For Louis, the investment roadmap is straightforward:

Follow the money.

That leads to the companies positioned to benefit most from the wave of AI-driven spending and earnings growth.

That’s why AI infrastructure is on his radar. And one aspect of that buildout, in particular, looks especially compelling.

Here’s Louis:

As the AI Revolution heats up, there will be a massive surge in demand for storage solutions – specifically NAND flash storage.

NAND is the technology behind the solid-state drives and memory chips that store data in everything from smartphones to data centers. It’s fast, compact and energy efficient – which makes it the storage solution of choice for AI workloads.

Louis explains that training models, running inference, and powering machine learning applications all require enormous amounts of data to be stored quickly, reliably, and securely. That’s translating directly into soaring demand for NAND memory.

Importantly, supply isn’t keeping pace.

According to Commercial Times, demand for NAND is expected to grow more than 20% this year, yet supply is on pace to climb only 15%-17%. That imbalance is creating a powerful tailwind for leading memory players.

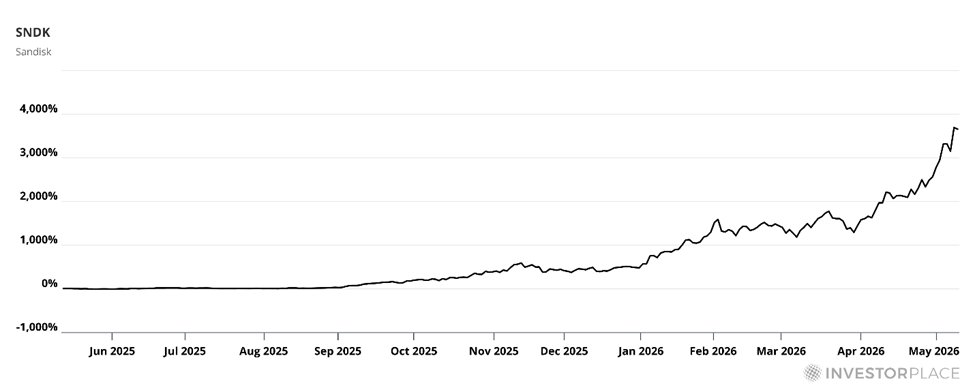

For example, SanDisk (SNDK) – the pure-play NAND provider that spun off from Western Digital in early 2025 – has risen more than 3,500% over the last 52 weeks.

Additional leading NAND stocks have also made big moves, leading to the question…

Is it too late?

Louis says no. With major new production capacity unlikely to arrive before 2027, supply elasticity remains constrained. That means NAND pricing could stay elevated for far longer than many investors expect.

So, while the momentum has certainly been explosive, Louis believes it’s being driven by a structural supply-demand imbalance with plenty of runway still ahead. This is why he just steered his Breakthrough Stocks subscribers into a new NAND position:

As the AI Revolution heats up, there will be a massive surge in demand for storage solutions – specifically NAND flash storage.

That’s why I’m adding a new stock to the Buy List this month.

I won’t reveal it today out of respect for Louis’ Breakthrough Stocks subscribers, but the investment legend will be giving away one of his favorite stocks for today’s market at his live event tomorrow at 1:00 p.m. Eastern.

As we’ve been highlighting here in the Digest, Louis remains especially bullish on small caps for several reasons – including what he believes will eventually become a much easier monetary policy environment under potential Fed Chair Kevin Warsh.

To be clear, Louis isn’t calling for immediate rate cuts – especially not after this morning’s hot CPI print. But he does believe the market is underestimating just how accommodative policy could become under Warsh, and how that could pour gasoline on leading small-cap and AI infrastructure names.

You can get the full story directly from Louis tomorrow at 1:00 p.m. Eastern. Just click here to reserve your seat today.

Before we move on, one note…

Given everything we’ve covered so far today – hot inflation, record-low consumer sentiment, a Fed that’s boxed in – you might expect some defensive posture from Louis.

Not so much.

Consider what he wrote to subscribers in last week’s Breakthrough Stocks issue:

The last time I saw anything like this was 1999.

Back then, the internet boom drove stocks to extraordinary heights. Today, it’s the AI data center boom.

The similarities are striking. And if history is any guide, we are still in the early innings.

But this excitement doesn’t apply to all stocks…

In fact, we have a “tale of two markets” that’s only growing more pronounced.

We’ve been tracking this bifurcation for years now. But this earnings season is bringing it into even finer resolution.

There are effectively two stock markets operating simultaneously today. The AI market. And the “everything else” market.

To be clear, “everything else” hasn’t been bad. It’s just been getting lapped by AI.

Over the last month, the S&P 500 has climbed nearly 7%. But strip out AI stocks (by looking at the US 500 Excluding Artificial Intelligence Enablers Price Return Index, SPXXAI), and the index hasn’t even gained a full 1%.

Meanwhile, data from Jefferies shows AI companies have generated over 80% of the S&P 500’s year-to-date returns. Strip away the AI component, and the benchmark has advanced a mere 2%.

But here’s where things are changing during this earnings season…

Whereas “lagging but okay” was yesterday’s story for many non-AI stocks, we’re beginning to see some genuinely ugly numbers.

Our technology expert Luke Lango, editor of Innovation Investor, has been tracking this deterioration. And last Tuesday, he pointed to Whirlpool as a red flag worth noting:

Whirlpool effectively confirmed the underlying economic reality.

“War in Iran resulted in recession-level industry decline in the U.S. as consumer confidence collapsed in late February and March,” the company stated directly in its earnings filing.

U.S. appliance demand fell 7.4% in Q1, including a 10% decline in March alone. CEO Marc Bitzer compared the slowdown to conditions seen during the global financial crisis.

Now, as we’ve covered here in the Digest, Luke believes we’re entering the “Summer of AI.” But in keeping with the “tale of two markets” dynamic that we’re tracking, Luke also says that some companies are entering the “Summer of Stagflation”:

AI companies are reporting stellar earnings, and their stocks are mostly soaring.

Other companies are reporting worrisome earnings, and their stocks are mostly struggling.

Welcome to the Summer of AI… as well as the Summer of Stagflation.

This dynamic will persist. Which means it is our job to make sure you benefit from the Summer of AI – and avoid the Summer of Stagflation.

Coming full circle, guess one of the corners of the market that Luke highlights as likely to outperform during the Summer of AI?

You guessed it – the “AI memory dogs” as he put it, specifically citing SNDK as well as other NAND-focused plays tied directly to the exploding demand for AI infrastructure.

That’s why both Louis and Luke continue circling back to the same core message…

Follow the AI spending wave.

Bottom line: while much of the market may continue struggling through slower growth and rising inflation, the companies powering the AI buildout could still be in the early stages of a massive multiyear run.

We’ll keep you updated on all these stories here in the Digest.

Have a good evening,

Jeff Remsburg

(Disclaimer: I own GOOGL, AMZN, and MSFT)