Listen to the audio version of this article (generated by AI).

Albany pulls the plug… Ford’s “AI Boomerang” in jobs… a margin-debt flashing light… why we’re not worried about the AI trade yet… and how to trade either way

Yesterday, New York Governor Kathy Hochul signed an executive order barring construction of new large-scale data centers – those drawing 50 megawatts or more of power – for up to one year.

New York is now the first state in the nation to impose such a ban, though at least 15 others are considering or actively advancing legislation to restrict, study, or temporarily ban new data center construction.

Hochul framed it as a matter of survival for ratepayers:

We’re in the midst of one of the most significant economic upheavals in generations … perhaps ever.

These hyperscale AI data centers consume enormous amounts of power…

They drive up costs for local ratepayers, and I refuse to let those costs get passed down to New Yorkers.

This isn’t just a New York issue – it’s representative of a national anti-AI mood that’s increasingly framed in political and moral terms.

Back in April, Sen. Bernie Sanders (D-Vt.) said:

AI oligarchs do not want to just replace specific jobs.

They want to replace workers.

That’s a wildly provocative and easily debated assertion. But even if that’s true, these “AI oligarchs” still must contend with something more powerful than they are – the customer.

Cut too many of the right employees, and quality drops – and the customer retaliates long before any politician does.

About a year ago, Ford (F) CEO Jim Farley made a headline-grabbing prediction

He said:

Artificial intelligence is going to replace literally half of all white-collar workers.

While Ford then cut portions of its workforce and turned to AI during its broader restructuring, it turns out AI couldn’t quite finish the job on its own.

Over a rolling three-year initiative to fix costly vehicle defects, Ford has quietly rehired 350 veteran engineers – internally nicknamed “gray beards” – to fix quality problems its AI-driven design systems couldn’t catch on their own.

The fix worked: Ford just topped JD Power’s Initial Quality Survey for the first time in 16 years.

Ford isn’t alone in its return to human workers.

IBM (IBM), Starbucks (SBUX), McDonald’s (MCD), Air Canada, and Commonwealth Bank of Australia, among others, have all made similar reversals recently after quality dropped.

But the most dramatic example may be Klarna (KLAR), the Swedish buy-now-pay-later giant. It slashed 22% of its workforce and boasted that its AI chatbots could do the work of 700 human agents – before quietly launching a recruitment drive to bring humans back into customer support after service quality collapsed.

Workforce firm Careerminds found that two-thirds of companies that made AI-driven cuts in the past year are already rehiring, more than half within six months.

This pattern already has a nickname: the “AI Boomerang” – cut for AI, watch the judgment-heavy edge cases pile up, then rehire humans at a higher cost.

Nearly a third of rehiring companies ended up spending more than they’d originally saved, because AI-era replacement roles now command a 20%-25% pay premium over the roles they replaced.

Still, the wider jobs data tells a complicated story

Challenger, Gray & Christmas’s June report showed overall U.S. layoffs cooling sharply – down 53% from May.

But AI was still the leading reason cited for job cuts that month, the fourth straight month it’s topped the list. And AI-linked cuts now account for roughly 23% of everything announced this year.

Meanwhile, an MIT study using a tool it calls the Iceberg Index estimated AI can already perform work equivalent to 11.7% of the U.S. labor force – about $1.2 trillion in wages.

As of now, actual layoffs represent only a small fraction of that exposure – but clearly the potential for far more is available.

Put those two threads together, and you get the real shape of this story…

AI fear is currently running well ahead of AI layoffs.

Our technology expert, Luke Lango, has been tracking this broad anti-AI sentiment

Luke, editor of Innovation Investor, has argued for months that the thing most likely to end this AI bull market isn’t a technological stumble – it’s policy:

The force that will derail the AI Boom is not a technological failure, demand collapse, or even a recession.

It is politics – specifically, a populist backlash against AI that is already building momentum, fueled by the growing economic pain hitting American households right now.

And it’s on a trajectory to reach full force right around the 2028 presidential election cycle.

Yesterday’s data center moratorium in New York is exactly the kind of early tremor Luke predicted. Rising energy bills, viral anger, and politicians willing to act on it are shaping up to be a fierce headwind against AI.

But Luke isn’t sitting on the sidelines waiting for that day. He’s still bullish on AI today because he believes we’re in the strongest phase of the boom.

At the same time, he’s constantly monitoring the political landscape, corporate spending, and market leadership for the signals that the investment landscape is beginning to change. That allows him to stay positioned in the companies still benefiting from AI’s rapid expansion today – while preparing subscribers for the eventual shift before it becomes obvious to Wall Street.

If you’d like to follow Luke’s research and see the AI companies he believes are best positioned in this stage of the cycle, you can learn more about Innovation Investor here.

So, where does all this leave investors?

We’re still long the AI trade – but watching the calendar just as closely as the earnings.

But being long the AI trade doesn’t feel very good these days, and there’s a new reason for caution

Yesterday, we learned that margin debt just hit a level that’s only been seen at past market tops.

Let’s go to CNBC:

According to data from Leuthold Group, margin debt has grown by more than 40% over the past 12 months, a threshold seen at prior market peaks in 2000, 2007 and 2021.

To make sure we’re all on the same page, margin debt is money you borrow from your broker, using your existing stocks as collateral, to buy even more stock. It juices your gains on the way up – but amplifies your losses on the way down.

What’s unusual this time is the pace relative to the market itself…

The S&P 500 is up about 22% over the past year, dividends included – roughly half the rate at which margin debt has grown. Put simply, investors are borrowing money faster than stocks are actually rising.

Leuthold’s chief investment officer, Scott Opsal, was direct with CNBC about the implications:

When people start doubling down with borrowed money, that’s a contrarian sign that’s really hard to beat…

This is very bearish looking.

Opsal has a theory for where the borrowed money is going: the AI trade.

He points to the recent boom in leveraged ETFs – assets in those funds nearly doubled in just two months this spring.

That matters because concentrated bets amplify themselves on the way down, too. If a single AI infrastructure or data-center stock cracks, the margin calls that follow could ripple through every other investor leaning on the same trade – forcing sales that have nothing to do with the underlying business and everything to do with a broker demanding more collateral.

To be clear, this doesn’t mean the AI trade is finished. But alongside the political backlash we’ve been tracking above, it’s one more sign that this bull market may be entering its more fragile, top-heavy stretch.

As always, be sure you know what you own, why you own it, and what your exit strategy will be if you’re not in it for the long haul.

If this has you feeling panicked, take a breath…

Everything above is a reason for caution, not runaway fear.

The recent sharp pullback isn’t unusual – it’s often just the toll booth on the way through a bull market, especially in the group leading this one.

That kind of drop can feel like the beginning of the end. But let’s be clear about where the damage is concentrated, and then contextualize it…

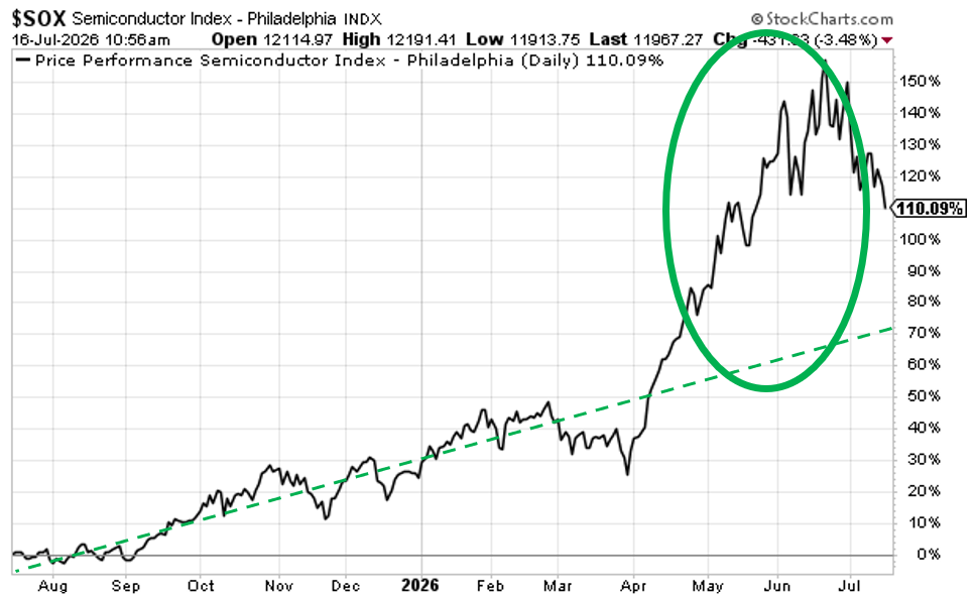

The PHLX Semiconductor Sector Index (SOX) – a proxy for the AI trade since semis are the brains of AI – is down about 18% from its recent peak in June.

It’s off again today despite Taiwan Semiconductor (TSM) reporting a record 77% surge in quarterly net profit that beat Wall Street expectations. Investors are concerned about a 15% hike in its 2026 capital spending plan, reinforcing the sector-wide fear that excessive spending will hurt long-term profit margin.

Now, this pullback is painful for sure, but it’s also well short of the 30%+ drawdowns that have marked prior sector-wide tops in 2000, 2008 and 2018.

Plus, we should remember the near-vertical ascent that preceded it (trendlines added for perspective).

From this perspective, we’re just working off some of that excess.

Now, a skeptic could say:

Okay, Jeff, but what stops the current 18% SOX pullback from becoming a 30% crash next month, then 90% debacle by Christmas?

Well, I can’t guarantee you that won’t be the outcome – but history argues against it.

Studies of S&P 500 volatility since 1929 show that only about 39% of corrections have ever deepened into a full 20%+ bear market – and in the decades since World War II, that rate has dropped closer to 25%.

Most corrections stall out in the mid-teens and recover within a few months, which is almost exactly where the SOX sits today.

Bottom line: If you’re white-knuckling your way through this correction, there’s reason for optimism.

Still, if you want to be more selective in how much exposure you have to today’s volatile market, we have an idea for you…

Let historical data guide your trades.

This morning, legendary investor Louis Navellier and TradeSmith CEO Keith Kaplan went live in their Breakthrough 2026 event.

In short, instead of predicting where the market or a stock will go next, Keith’s team studied decades of price history across roughly 5,000 stocks, looking for historically favorable windows when those stocks have risen or fallen with real consistency – in bull markets and bear markets alike.

Running an 18-year backtest, trading only within those windows produced 857% total growth, more than double the S&P 500 over the same stretch, and the strategy still came out ahead in 2007, the worst year in the test.

With this approach, you can pick and choose your shots, keeping as much money as you want on the sidelines. You take advantage of trading opportunities only when – and for how long – you decide, all according to historical data.

If you missed the broadcast, we have a free replay available to you right here.

We’ll keep you updated on all these stories here in the Digest.

Have a good evening,

Jeff Remsburg