It seems like the markets can’t get enough of FireEye Inc (FEYE). After trudging through a volatile start to the year, FEYE stock finds itself down about 20% since the beginning of January.

Due to both internal and external challenges, FireEye sought the assistance of Morgan Stanley (MS) to explore a possible sale of the company.

At least two companies put forward a bid, including internet security giant Symantec Corporation (SYMC). However, no bid reached the $30 premium for FEYE stock, and FireEye promptly retracted the sales offer. Was this a smart move, or is management expecting way too much?

Although FEYE stock rebounded immediately after the rejection made the newsreel, there’s tons of questions hanging over the struggling cybersecurity firm.

First and foremost is sales, or lack thereof. For the first quarter of fiscal year 2016, FireEye could only muster a mixed performance. The actual loss on FEYE earnings was less than forecasted. However, first-quarter revenue was down more than 2% against expectations. Even more problematic, FireEye cut its guidance for the year.

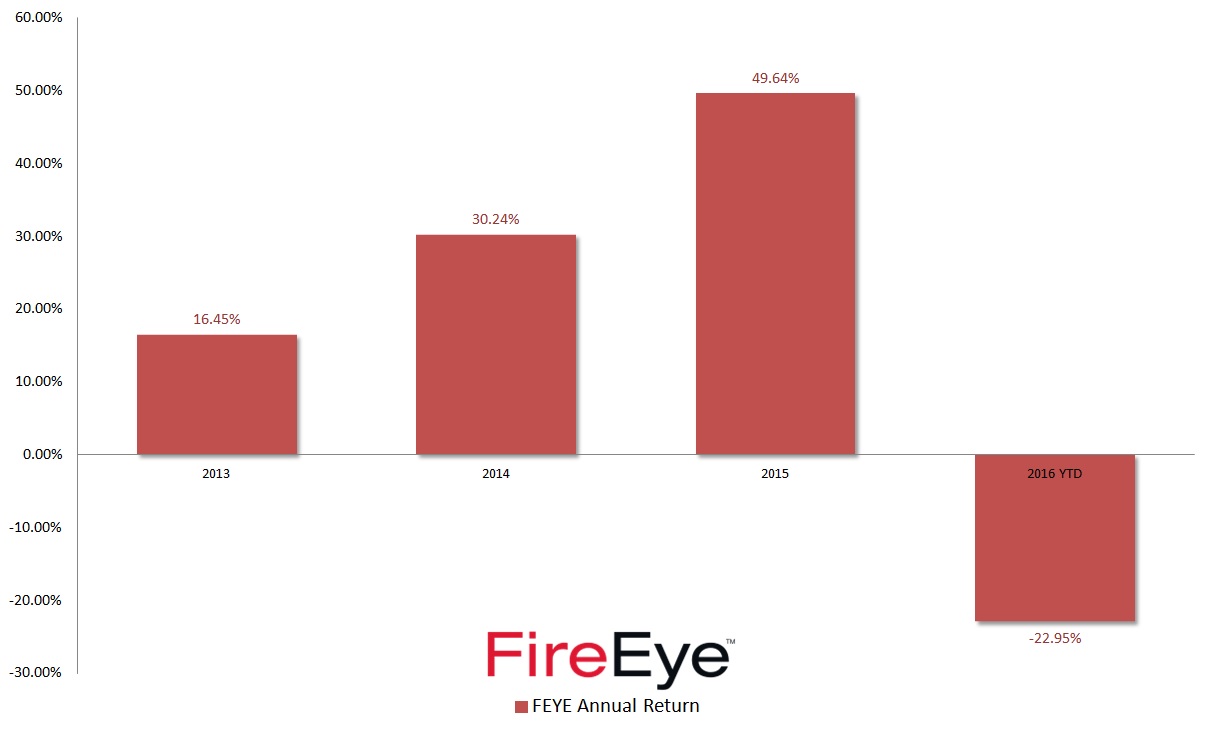

FireEye: Weak Financials, Strong Sector

Admittedly, the company’s financials hardly inspire confidence.

Click to Enlarge

Of course, financial performance isn’t the final arbiter of investment profitability. We’ve seen plenty of companies that look terrible on paper, yet flourish in the markets. But what makes FEYE distinct is that speculators have undoubtedly bought shares hoping for a buyout. With that option taken off the table for now, will these weak-hand traders continue to stay on board?

While those hoping for a quick pop will probably walk toward the exit, there’s plenty of reasons why investors will want to maintain their position.

As I argued previously, you have to consider the underlying industry of FireEye — cybersecurity is a massively important sector. The digitalization of crime has become much more sophisticated. Companies and government bodies are collectively willing to spend billions of dollars to avoid the crippling damage that network hacking or other related intrusions can render.

More critically, cybersecurity isn’t just about financial losses. With stunning competency, terrorist organizations are using the internet — particularly social media platforms — to disseminate propaganda and for recruitment campaigns. As we steadily head toward a new decade, cybersecurity will be at the forefront of the global “War on Terror.” Those that have expertise in this area will not only have the opportunity to service private sector demand, but public demand as well.

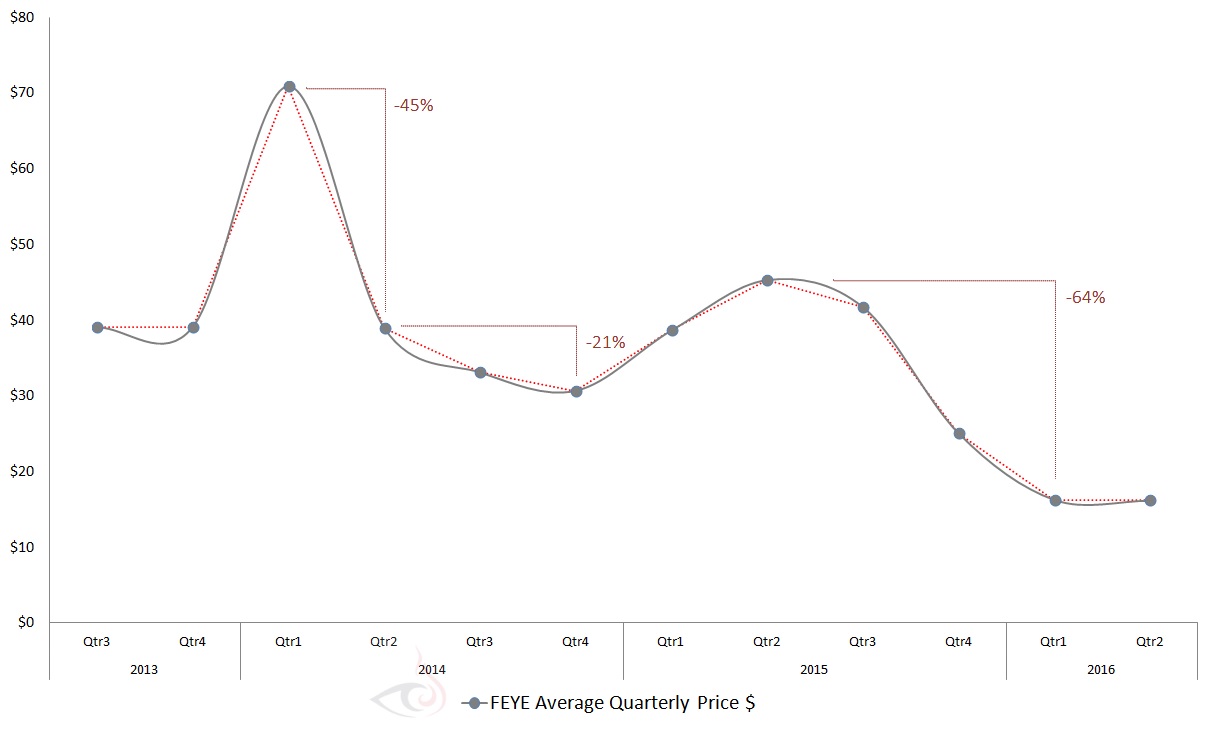

FEYE Stock Charts

Technically, there’s also a case to be made for FEYE stock despite its tumultuous history. When we break down FireEye shares’ price action on a quarterly average basis, we see evidence of a bottom support level forming.

Click to Enlarge

During the second half of 2015, another bout of extreme volatility plunged shares down to where they are now. But starting this year, the average price of FEYE has not changed appreciably quarter-to-quarter.

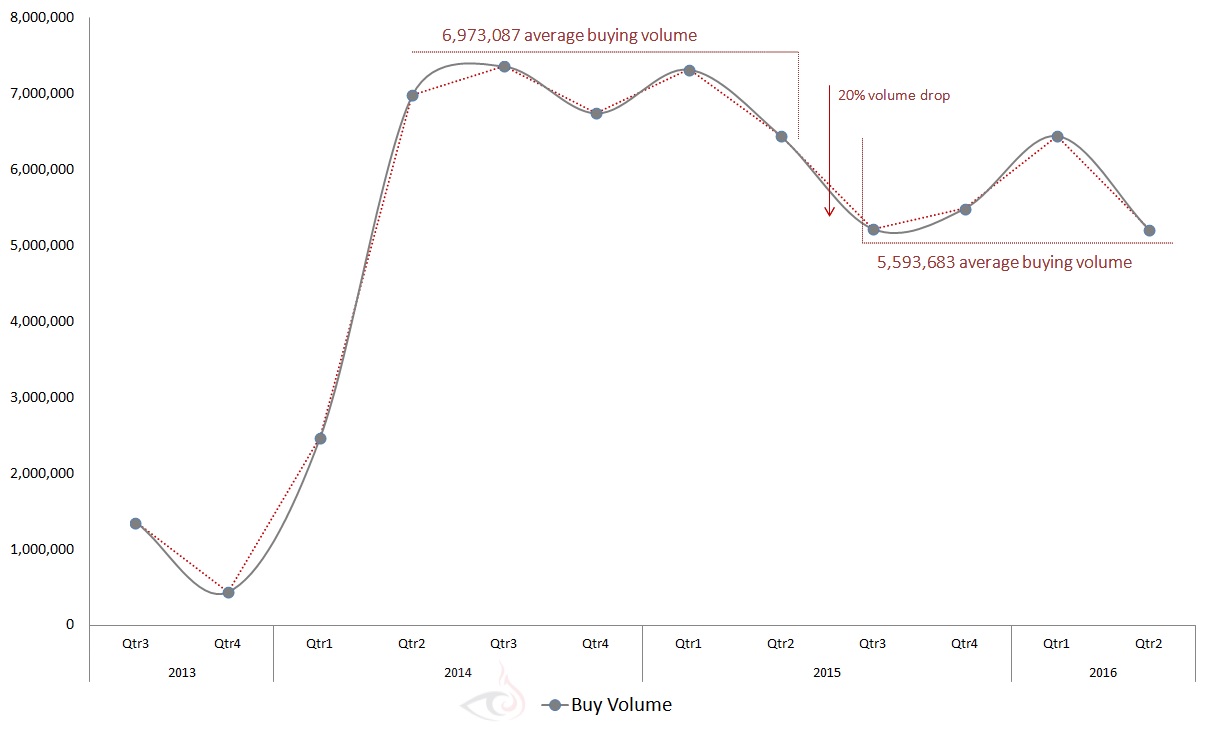

We also have to consider the case of buying volume, or trading volume, when FEYE stock gains against the prior session.

Click to Enlarge

Starting from the second-half of 2015 until today, that number has declined to 5.6 million, or a 20% drop in volume.

Yes, it’s a significant reduction, but the average share price has lost 34% over the same time frame. It also proves that there’s still substantial buyers’ interest toward FEYE stock.

FireEye has had one of the rougher journeys among newly public companies. Because of this, many will question their decision to shun acquisition offers. As difficult as it must have been, management has made the right decision.

FEYE stock is more than just a buyout target. There’s plenty of industry tailwinds that can push FireEye through a challenging period. In addition, FireEye has a large core of supporters that believe in its long-term potential.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.