What a difference a month makes… Back in early April, stocks were crashing into a bear market on fears that President Trump’s “Liberation Day” tariffs would freeze global trade, reignite inflation, and send the economy spiraling into a recession. After April 2’s tariff blitz, stocks fell 10% in two days; something that’s happened only a handful of times in the past 100 years.

Since then – thanks to tariff rollbacks, resuming trade flows, and a restabilized global economy – the market has staged one of its sharpest short-term rallies ever as the S&P 500 climbed nearly 20% in just over 20 days.

This rally is showing no signs of fatigue just yet… and we don’t think it will anytime soon.

Just look to yesterday’s Consumer Price Index (CPI) report. In our view, it wasn’t just a “good” inflation report – it was the sort of data that should help set the stage for a massive summer stock rally.

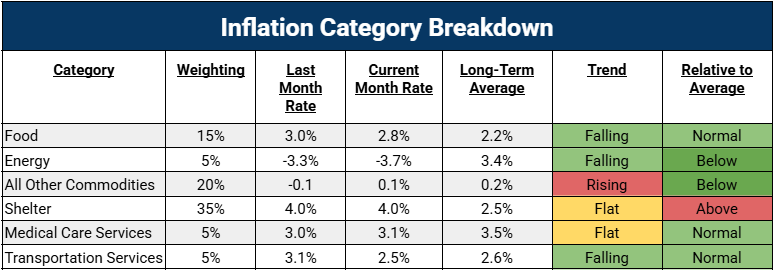

Headline CPI came in at just 0.2% month-over-month, below the 0.3% consensus. It was the same story for core CPI – a measly 0.2% increase, also undercutting estimates. Nearly every major component of the index either cooled or dropped outright:

- Food price inflation – down from 3.0% to 2.8% year-over-year

- Energy inflation – still negative and getting even more so, falling from -3.3% to -3.7%

- Transportation services inflation – down from 3.1% to 2.5%.

Shelter stayed elevated; but even there, cracks are starting to show.

In short, inflation didn’t flare up as so many feared. It fizzled. And in this environment, that’s about as bullish a signal as it gets.

But here’s the real kicker: April’s soft inflation print wasn’t just a sign of easing price pressures. To us, it was a death knell for what had been the market’s biggest fear this spring: tariff-driven reinflation.

Overblown Inflation Fears Are in the Rearview

After Trump launched the biggest tariff barrage since the Smoot-Hawley days on April 4, pundits rang the alarm bells, warning of imminent price spikes.

But it seems the data is giving those doomsayers the cold shoulder.

In March, before the tariffs began, CPI inflation was 2.4%. In April – post-“Liberation Day” – it ran at 2.3%. And right now, according to the Cleveland Fed’s Nowcasting, real-time data for May is tracking at 2.4%. It seems there’s no tariff reinflation to be seen.

How about core CPI inflation? 2.8% in March, 2.8% in April, tracking for 2.8% again in May – that’s a textbook definition of stable.

So, what gives? Didn’t Trump just slap a 125% tariff on Chinese imports, among other things?

Yes; but he also hit the brakes.

Since “Liberation Day,” we’ve had a 90-day tariff pause, exemptions for auto parts and electronics, a U.S.-UK trade deal, and a U.S.-China trade truce. Collectively, those actions slashed the average effective U.S. tariff rate from a sky-high 30% to a far-more-manageable 13%.

So, if 30% tariffs didn’t spark reinflation, 13% tariffs definitely shouldn’t.

That’s why we’re burying the reinflation narrative. The data is making it clear that tariffs are not causing reinflation.

And so long as things keep trending in the direction they are going right now, tariffs won’t cause any reinflation anytime soon.

Inflation Eases, Tariffs Fall, and the Bull Market Case Gets Stronger

With that crippling fear in the rearview, there’s little left to stop this rally…

Because let’s look at the macro mosaic now:

- Inflation is stable and trending lower: headline inflation slowed to 2.3% year-over-year in April, down from 2.4% in March.

- Tariffs are falling: U.S. tariffs on Chinese goods dropped from 145% to 30%, and Chinese tariffs on U.S. goods fell from 125% to 10%.

- Trade deals are happening: The U.S. and U.K. finalized a trade agreement focusing on security cooperation, and the U.S. and China signed an initial trade deal reducing tariffs and aiming to end retaliation.

- The Federal Reserve is poised to cut rates: Policymakers anticipate two rate cuts in 2025, with the federal funds rate currently at 4.25%–4.50%

- Consumer spending is holding up: Bank of America data indicates consumer spending grew at a 1.6% annualized rate in April 2025, showing moderate momentum.

- Corporate earnings are solid: Analysts project S&P 500 earnings growth rates of 6.4% to 8.8% for Q2 through Q4 2025, with a full-year growth estimate of 9.7%.

- AI stocks are ripping higher. Today, Wednesday, May 14:

- Nvidia‘s (NVDA) shares rose 3% in premarket trading after a significant AI chip deal, pushing its market cap above $3 trillion.

- AMD‘s (AMD) stock surged 5.5% following a $6 billion buyback announcement and a $10 billion joint venture with Saudi-backed firm Humain.

- Palantir (PLTR) shares hit all-time highs, climbing 2% premarket after an 8% gain, driven by optimism around AI and tariff relief.

Put it all together, and we have what we call a ‘no-brainer bull market’ setup.

The Final Word: Soft CPI Clears the Way for a Summer Surge

The market’s technicals are just as bullish as the macro backdrop is.

The S&P 500 is up 17% in just 23 trading sessions. That’s happened only seven times since WWII. Every single time, it marked the beginning of a major bull market.

This is what late 1998, spring 2009, and summer 2020 felt like. If you knew what was coming then, you were backing up the truck.

And we think that’s exactly what investors should be doing right now…

Especially in AI stocks.

Those are the companies that will benefit most from this macro tailwind cocktail of easing inflation, falling tariffs, and incoming rate cuts.

So, yes, April’s CPI report was a big deal. It removed the final major roadblock to a full-fledged summer meltup.

The rally is real. The path is clear, and the fuel is loaded.

It’s time to lean in and grab ahold of the gains ahead.

And we expect that in this summertime surge, a new form of AI – something we call AI 2.0 – will steal the spotlight and rake in the biggest profits on Wall Street by far.

AI 2.0 isn’t about faster chatbots or better spreadsheets.

It’s about bringing intelligence into our homes, our factories, our streets. It’s about machines that see, think, and move – and the companies that turn that ability into serious revenue.

While the world’s distracted with what AI has done… The smart investors are already looking at what it’s about to do next.

Learn more about some of our favorite AI 2.0 picks right now.

Questions or comments about this issue? Drop us a line at langofeedback@investorplace.com.