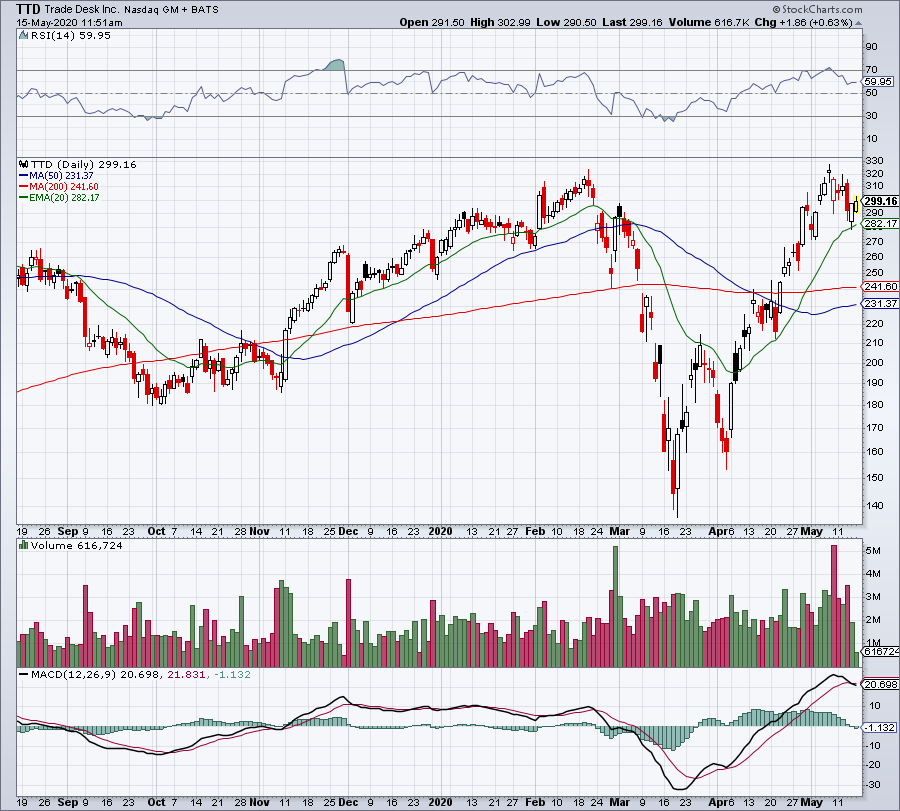

The Trade Desk (NASDAQ:TTD) is one of the best growth stocks out there — and I’m not trying to be hyperbolic. Yet TTD stock plunged from $320 in February to sub-$150 in March, down 58%.

I don’t think that The Trade Desk deserved such a plunge and I’ll highlight why in a minute. But equally, I don’t know that it deserves to rally 140% from its March low to a new all-time high in May.

Again, this is a fabulous company with incredible growth. But that kind of move amid this kind of uncertainty has me thinking twice. But first, the good.

Why We Like TTD Stock

What does The Trade Desk do?

The company “operates a self-service cloud-based platform that allows buyers to create, manage, and optimize data-driven digital advertising campaigns.” This spans mobile, social, desktop, connected TV and more, and essentially acts as an A.I.-based advertising platform.

When we think of advertising, Alphabet (NASDAQ:GOOGL, NASDAQ:GOOG) and Facebook (NASDAQ:FB) may first come to mind. The Trade Desk works in a different way. It acts as a tool to advertisers, rather than the distribution platform (i.e. a search engine or social media site).

It’s worth pointing out that TTD helps place ads in all sorts of mediums, including in search engines and social media sites. But it must be understood that this is a tool for advertisers and it’s one that’s generating a ton of growth.

Even with the impact of the novel coronavirus, The Trade Desk is still forecast to churn out 16.6% revenue growth this year. This is a company that generated about $660 million in sales in 2019 and is forecast to hit about $1 billion in revenue in 2021.

But one of my favorite things about TTD stock is that it’s profitable. Last year, the company generated earnings of $3.69 per share. That figure is forecast to fall to $3.09 per share this year — as Covid-19 dramatically shifts the advertising landscape — before rebounding to more than $4 per share in profit in 2021.

On a price-to-earnings basis, of course TTD stock is expensive. But the fact that it can grow so aggressively and do so profitably at the same time is wildly attractive. Lastly, TTD operates in China too, a country that most U.S. tech titans are banned in. Yes, that includes Google and Facebook.

A Dose of Reality

Click to Enlarge

When The Trade Desk reported earnings, it beat on top- and bottom-line estimates. However, it did not provide Q2 or full-year guidance. Combine that uncertainty with what we’re seeing at Pinterest (NYSE:PINS), Facebook and Google, and it’s clear that digital advertising is taking a hit in 2020.

Optimists will say that hit is temporary — and perhaps it is. We already know that ad spend fell off a cliff in March, but looked to be bottoming in April. If that’s the case, the impact shouldn’t be so bad and investors will likely look to the future rather than focus on the present.

That’s all fine, assuming ad sales actually do bottom in April before rebounding notably through the end of the year. The problem is, we don’t know that it will.

Los Angeles is talking about extending its stay-at-home orders through July. Companies are burdened by extra expenses and reopening costs. Those funds have to come from somewhere and marketing dollars could be hit. A recent report highlights the likely drop in TV ad spend now that certain contract options allow for cancellations.

I’m not saying this to be a doom-and-gloomer. But rather, question why TTD stock just hit all-time highs and why Facebook came within a few percent of doing so when, even under optimistic assumptions, the digital ad market will suffer in 2020.

The Bottom Line

I must reiterate that you should not interpret the last section as doom-and-gloom. Instead, it comes from a more cautious observation. Remember, I have been bullish on stocks and in particular, on tech.

In normal times, stocks that have market-beating growth are valued at a premium. However, I recently made the case that if these companies have strong growth in 2020 despite the impact of Covid-19, they are certainly worth a premium. In that light, and particularly after clarity from other digital ad companies, I don’t believe TTD deserved to fall 58%.

That said, this year is going to be worse than previously expected and we don’t know how Q3, Q4 and 2021 will shape up. Under that circumstance, it doesn’t feel reasonable to bid TTD to new all-time highs. Not in this environment.

In the long run, TTD stock is a winner, but in the short term, there is risk. I like this one a dip, but not at over $300.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. The power of being “first” gave Matt’s readers the chance to bank +2,438% in Stamps.com (STMP), +1,523% in Ulta Beauty (ULTA) and +1,044% in Tesla (TSLA), just to name a few. Click here to see what Matt has up his sleeve now. Matt does not directly own the aforementioned securities.