Alibaba (NYSE:BABA) stock has not had a good run lately. In fact, BABA stock is now down almost 20% from its all-time high on Oct. 27. For long-term investors, this is an excellent buying opportunity.

The big setback here was the Ant Group initial public offering (IPO).

Ant was set for a record IPO as it prepared its dual-listing in Hong Kong and Shanghai. The company was looking to raise between $34.5 billion and $39.7 billion — a record — valuing the company at more than $300 billion.

Why does this matter for Alibaba? Because the e-commerce juggernaut has a one-third stake in Ant.

Ant IPO Derailed

Given the size and the robust demand for the Ant offering, one can see why BABA stock was hitting new highs in late October. Coming into the event, investors were bullish, as the value for one of Alibaba’s prized assets continued to swell.

But the air quickly went out of the stock when the Ant IPO went off track. On Nov. 2, regulators met with Ant, as the former looked to tighten regulations around financial companies.

A day later, Ant pulled its Shanghai listing and paused its Hong Kong listing. The latter was eventually pulled as well. In response, BABA stock fell more than 8% on Nov. 3 and another 8% a week later on Nov. 10.

The damage has been done, as investors fear that Ant’s valuation has declined. And the IPO may be off for more than a year. That’s why BABA stock is down 17% from the highs. However, that’s also where the opportunity is.

Why BABA Stock Is a Buy

Think if the largest e-commerce stock in the U.S. fell 20% in a couple of weeks because it had a stake in a U.S. payment processing firm. That firm’s IPO was delayed, and its valuation took a dent. Wouldn’t you consider the larger company — with fundamentals intact — an opportunity for long-term investors?

It’s the same situation with Alibaba.

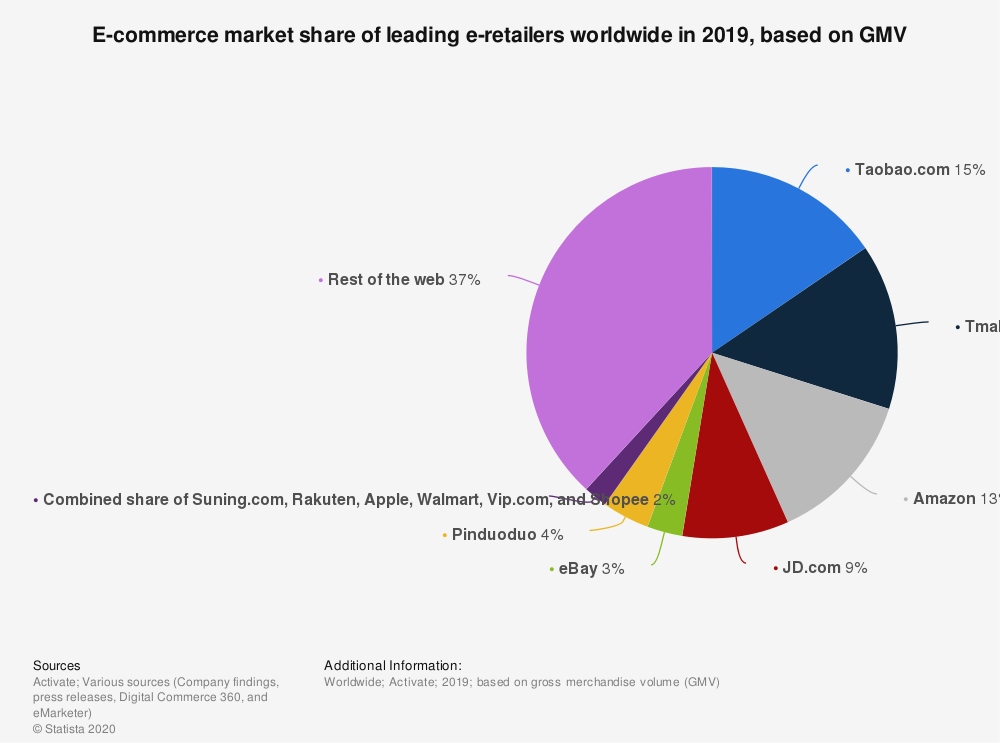

The company holds a dominant position in China’s online market. Not only does Alibaba have its flagship site — Alibaba.com — but it also owns Tmall and Taobao. For a look at their dominance, simply reference the chart above.

With robust growth in e-commerce sales, Tmall alone makes Alibaba undervalued. Then, you consider the firm’s growing Cloud-computing operation and its digital entertainment business. Alibaba is far more than an online wholesaler, it’s an undervalued conglomerate operating in one of the world’s strongest economies.

With a population of 1.4 billion people, China continues to swell. Its economic growth outpaces most of the developed world, while its middle class is roughly the size of the entire U.S. population. In my humble opinion, the average U.S. investor with little or no experience in China continues to undervalue this region as a whole, simply because they do not grasp the size of its potential.

The growth is right in front of our eyes.

BABA’s current-year estimates call for 47% year-over-year revenue growth to $107.4 billion. In 2021, estimates call for another year of strong growth. On the earnings front, consensus expectations call for growth of 37% and 20.7% this year and next year, respectively.

With earnings estimates of $10.36 a share this year, BABA stock is trading at less than 25 times earnings. That’s quite cheap for a company of this high quality.

Bottom Line on Alibaba

The Ant IPO fiasco is certainly not a positive for Alibaba. However, it doesn’t change the investment thesis, which is based on a long-term growth approach in e-commerce. Alibaba is dominating that space and will continue to dominate that space with or without a stake in Ant.

Its assets — did I mention Tmall and Taobao are the third and eighth most visited sites in the world? — combined with its growth creates a unique opportunity for investors. The fact that the valuation is reasonable is, quite frankly, very surprising.

Shares are pulling back to the 200-day moving average and are down roughly 17% from the highs. That is an opportunity to begin accumulating the stock. It’s possible shares see more short-term turbulence, dipping to the $230 area and retesting the breakout zone.

In the long-term though, it won’t matter. I’m a buyer of the current dip.

On the date of publication, neither Matt McCall nor the InvestorPlace Research Staff member primarily responsible for this article held (either directly or indirectly) any positions in the securities mentioned in this article.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. Click here to see what Matt has up his sleeve now.