Costco Wholesale (NASDAQ:COST) is an anointed retailer — there’s no other way to put it. While COST stock may go through ebbs and flows, it’s a long-term stalwart fit for any portfolio.

At the end of the day, investing is not that hard. It’s simply identifying the culmination of several factors, including management, past performance, quality financials and superior operations compared to its industry or sector. Emotions cloud our judgement though, making this “simple” task a very difficult endeavor.

In the case of Costco, it’s been an impressive performer for decades. As a result, it commands a premium valuation and that may bother some investors. But that’s just the way the world works. A Mercedes costs more than a Kia because it’s of higher quality. And a Lamborghini costs more than a Mercedes for the same reason.

Costco’s not some flimsy mall operator with a levered up balance sheet, so it shouldn’t be valued like one either. Here’s why it’s worth its premium.

Breaking Down Costco

Let’s look at Costco amid the pandemic. The company was deemed essential for obvious reasons. As consumers stocked up on everything from beverages to toilet paper, Costco was there checking out full carts worth of goods.

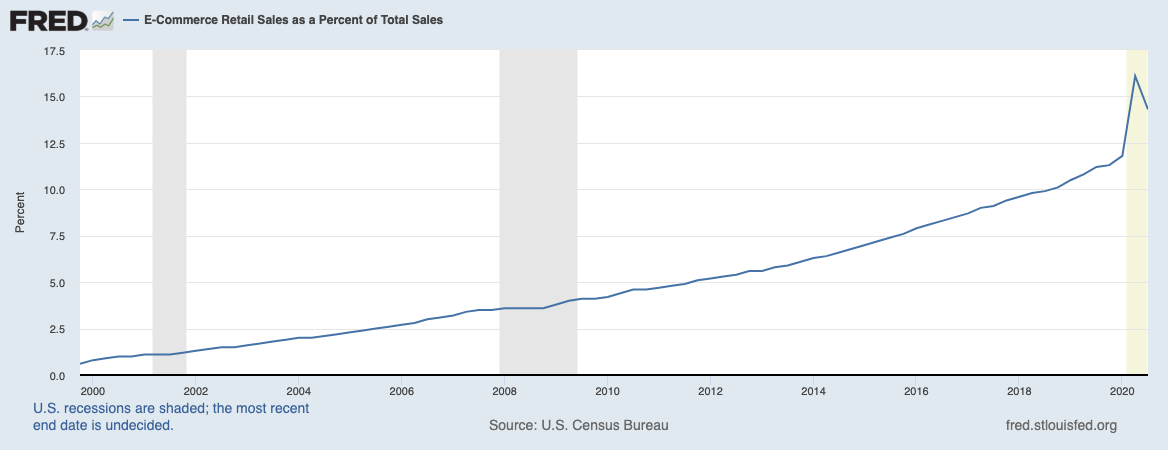

At the same time, e-commerce sales were booming, as illustrated above. The pandemic shuttered physical retail locations and thrust e-commerce platforms into the spotlight. This killed off some brick-and-mortar locations, while others thrived under a omni-channel operation.

So not only were consumers flooding Costco’s still-open locations (because it was essential), but its online operations have been going strong. March sales climbed 17.6% year over year, while e-commerce sales erupted 54.5%. Interestingly, those numbers include one fewer shopping day than the same period last year.

When the company last reported earnings on March 4, revenue of $44.77 billion grew 14.6% year over over and beat expectations by more than $1 billion. While earnings missed consensus expectations, management’s outlook was solid and sales were strong.

On April 14, the company gave a ~13% bump to its dividend, (although its yield is still less than 1%).

Going forward, investors aren’t looking for a reversion year, where Costco sees a dip in sales and earnings. Instead, consensus expectations call for double-digit growth, with 12.4% revenue growth and 14% earnings growth.

The one knock against COST stock is its valuation.

While the company is a clear leader in retail, it doesn’t come cheap. Trading at about 37 times earnings with a sub-1% dividend yield will surely turn off a lot of conservative investors.

The reality is that Costco has routinely sported a P/E ratio north of 30 over the last 10 years. That doesn’t mean it will always trade at 37.84 times earnings. It may trade sideways until earnings catch up. Perhaps it will pullback once more.

The point is though, quality businesses don’t come cheap — and they shouldn’t.

Bottom Line on COST Stock

Click to Enlarge

Steady, steady, steady. That’s all I think when I look at the long-term chart of COST stock. Shares are up 18.67% in the past 12 months, 51.75% in the last two years and 150% over the last five.

That’s what I mean by high-quality companies and their past performance. Many will look at that kind of performance and conclude, “Well it can’t last forever!”

Not only can it last, but it can continue.

Costco’s unique business approach, where it sells a high-margin membership and passes along attractive deals to consumers, will not fade away. Its adoption of e-commerce will only fuel its relevance with consumers.

If you look at the chart above, notice how COST stock still follows its longer-term trends. The stock toyed with breaking below the 21-month moving average, but ultimately held and rallied hard. Keep the bigger picture in mind when looking for buyable dips.

Stick with Costco.

On the date of publication, neither Matt McCall nor the InvestorPlace Research Staff member primarily responsible for this article held (either directly or indirectly) any positions in the securities mentioned in this article.

Matthew McCall left Wall Street to actually help investors — by getting them into the world’s biggest, most revolutionary trends BEFORE anyone else. Click here to see what Matt has up his sleeve now.