JPMorgan Chase & Co. (JPM) reported earnings for the first quarter of 2016 this morning, kicking off the earnings season for the banking sector. JPM earnings were a beat; revenues for the quarter hit $24.08 billion, compared to the $23.39 billion that Wall Street was expecting. JPM posted an EPS of $1.35, beating the Street’s estimates as well, with consensus expectations at $1.26.

But while earnings were a beat, they were still worse than both the top line and bottom line from Q1 2015, and that is somewhat ironic.

But while earnings were a beat, they were still worse than both the top line and bottom line from Q1 2015, and that is somewhat ironic.

The earnings beat points to the strength of JPM, i.e. to its disciplined cost control efforts. Meanwhile, the deterioration from the parallel period last year highlights JPM’s “Achilles Heel,” i.e. its investment banking unit.

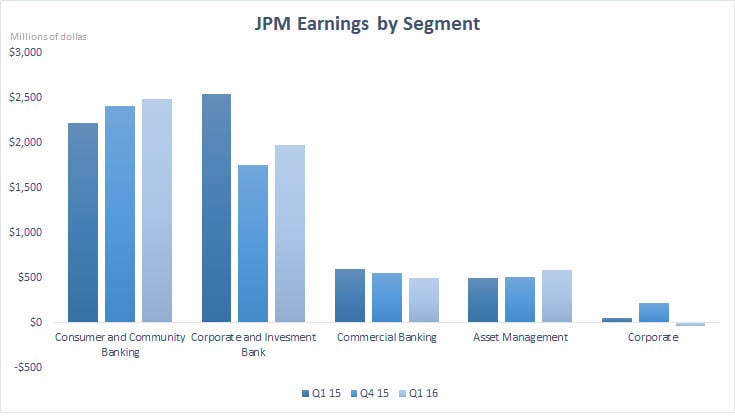

When we examine JPMorgan’s earnings per segment, the contradicting picture becomes clearer. On the one hand, we can see consumer banking is getting stronger with a steady rise in profits from Q1 2015 to the latest report of Q1 2016. On the other hand, we can see how corporate and investment banking took a plunge.

It’s as if all the increases in earnings from consumer banking — by all accounts a solid sector — are countered by the deterioration in the investment banking segment. And that deterioration comes in spite of JPMorgan being among the top investment banks. JPMorgan is not losing to competition; it is simply a victim of a weak sector, in general.

Click to Enlarge

JPM Stock Needs to Split

In 2012, it was the so-called “London Whale,” aka Bruno Iksil, which hit JPM’s investment arm. JPM is still feeling the effects. Now, there is weak demand for underwriting debt and securities that is creating a $1.2 billion shortfall. And that is before we count the burden of regulation that keeps making the investment banking business more expensive to maintain.

All the while, consumer banking is growing and turning stronger. And with both business segments running at different spreads and having different regulatory requirements, it’s fair to ask the question: Why doesn’t JPMorgan spin off its Investment Banking arm? That would let JPM shareholders benefit from its strengthening consumer business and the relative stability in its other segments.

In fact, Goldman Sachs had already made a much bolder call for that, back in January 2015. They recommended that JPMorgan split, not to two but to four pieces, which could make JPM much more profitable and thus, JPM stock much better to own.

Nonetheless, JPMorgan’s CEO, Jamie Dimon, insists on maintaining JPM at its whale size. Even though that’s a significant burden with the costly business of investment banking, he believes in the potential of the investment banking segment.

But the problem, as we can see from the latest reports, is that the recovery in investment banking is not coming. Rather — and every time, it seems — there’s one more, different reason for a disappointment and the shortfall in earnings.

If the investment banking arm would have delivered growth, Dimon would win his argument. But, as things look at the moment, JPM results are not good enough to counter the weakness in investment banking. Ultimately, that hurts shareholders and undermines the case for buying JPM stock.

Unless JPM stock delivers substantially better results, the split question will once again be asked and other banking stocks could be seen as much better alternatives.

As of this writing, Lior Alkalay did not hold a position in any of the aforementioned securities.