It’s not the most common of correlations but at least one prominent analyst has sounded a major warning for the broader economy.

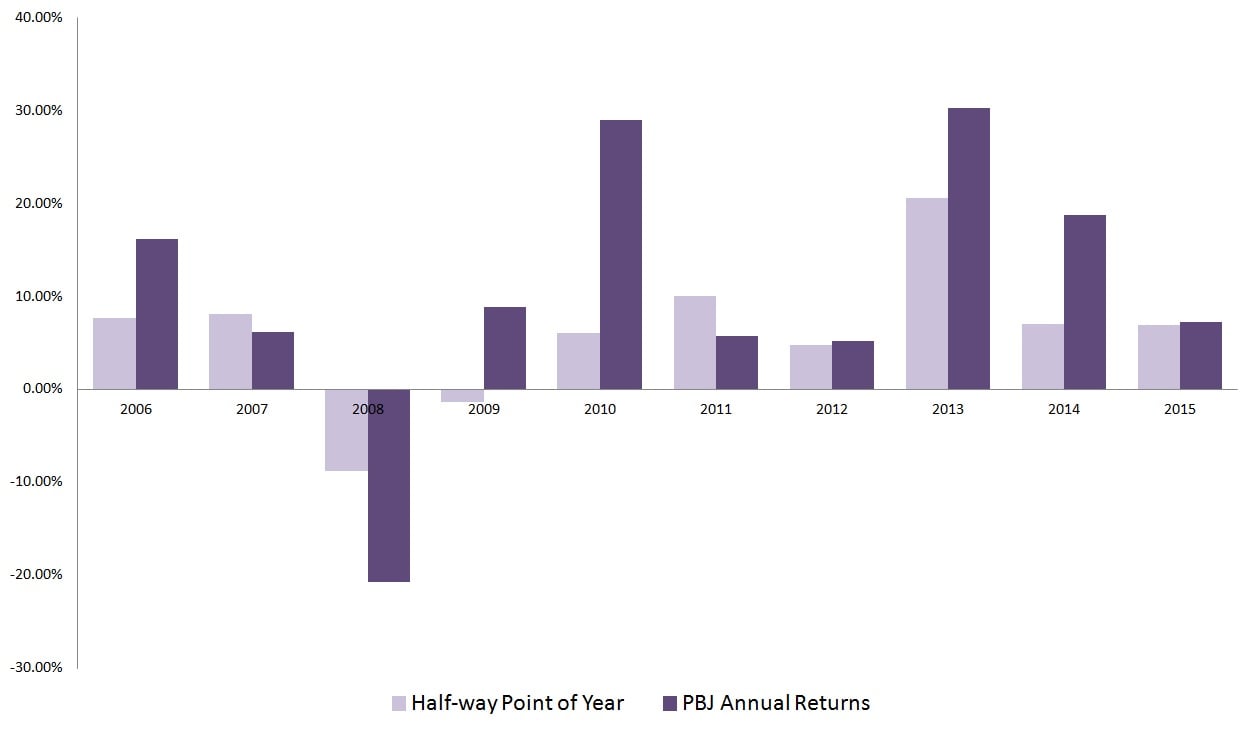

According to Stifel Financial Corp.’s Paul Westra, same-store sales for restaurant stocks have been struggling recently. This mirrors the troubles in the consumer retail sector, and potentially points towards an economic recession.

Stifel’s data suggests that the earliest a recession could come is 2017. Should investors be worried, or is this just another high-profile example of fear-mongering?

The news reel does seem to align with the bearish report. Restaurant stocks have stunk up the second quarter earnings season as several well-known names missed expectations.

Even fast-food restaurant stocks, such as McDonald’s Corporation (NYSE:MCD), fell short of sales growth estimates. More disconcerting is Starbucks Corporation (NASDAQ:SBUX) — corporate America’s drug of choice. Despite meeting consensus earnings forecast, SBUX failed to hit sales targets in every market. That possibly sets the stage for a global recession, not just an American one.

Click to Enlarge

While an outright recession may not be guaranteed, the slowing momentum of PBJ does point to concern for most restaurant stocks. However, if Americans are leaning back on discretionary spending, that’s hardly a positive sign for any industry. In addition, the University of Michigan’s Index of Consumer Sentiment is down 4.3% in the current month, and down 3.9% year-over-year.

Recession or not, eating out has become a hazardous journey in the markets. Here are three restaurant stocks you may want to avoid.

Rotting Restaurant Stocks: Darden Restaurants, Inc. (DRI)

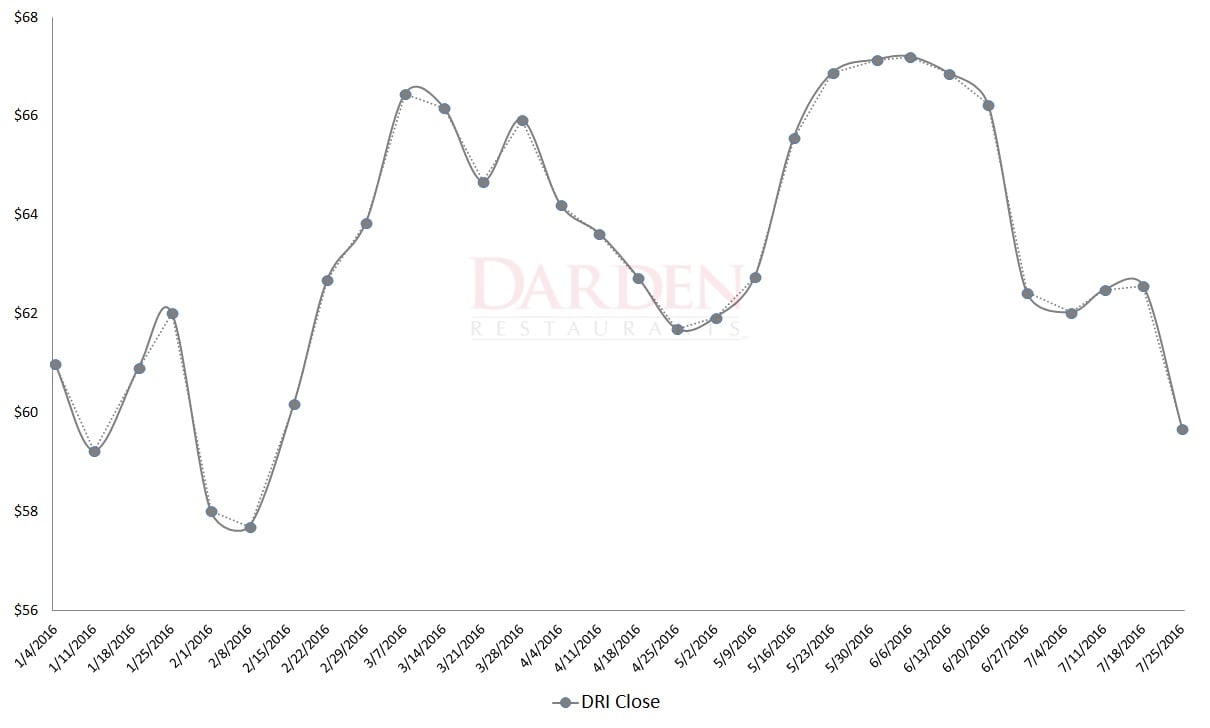

Stifel is definitely not showing any love whatsoever to restaurant stocks, as Darden Restaurants, Inc. (NYSE:DRI) can attest. After announcing the possibility of both an industry-wide and nationwide recession, Westra swiftly dropped DRI stock to a “sell” recommendation. Further adding salt to the wound, the Stifel analyst slapped DRI with a price target of $53. That’s about 11% off the current market value.

Click to Enlarge

The technical performance is where it looks really ugly for DRI stock. Year-to-date, Darden shares are in the red by more than 4%. But just in a two-day span this week, DRI lost more than 5% of market value. With shares below both its 50- and 200-day moving averages, Wall Street needs a compelling reason why it should take a risk on restaurant stocks.

Unfortunately, DRI isn’t what it used to be, and that’s got quite a few folks heading for the exits.

Rotting Restaurant Stocks: Chipotle Mexican Grill, Inc. (CMG)

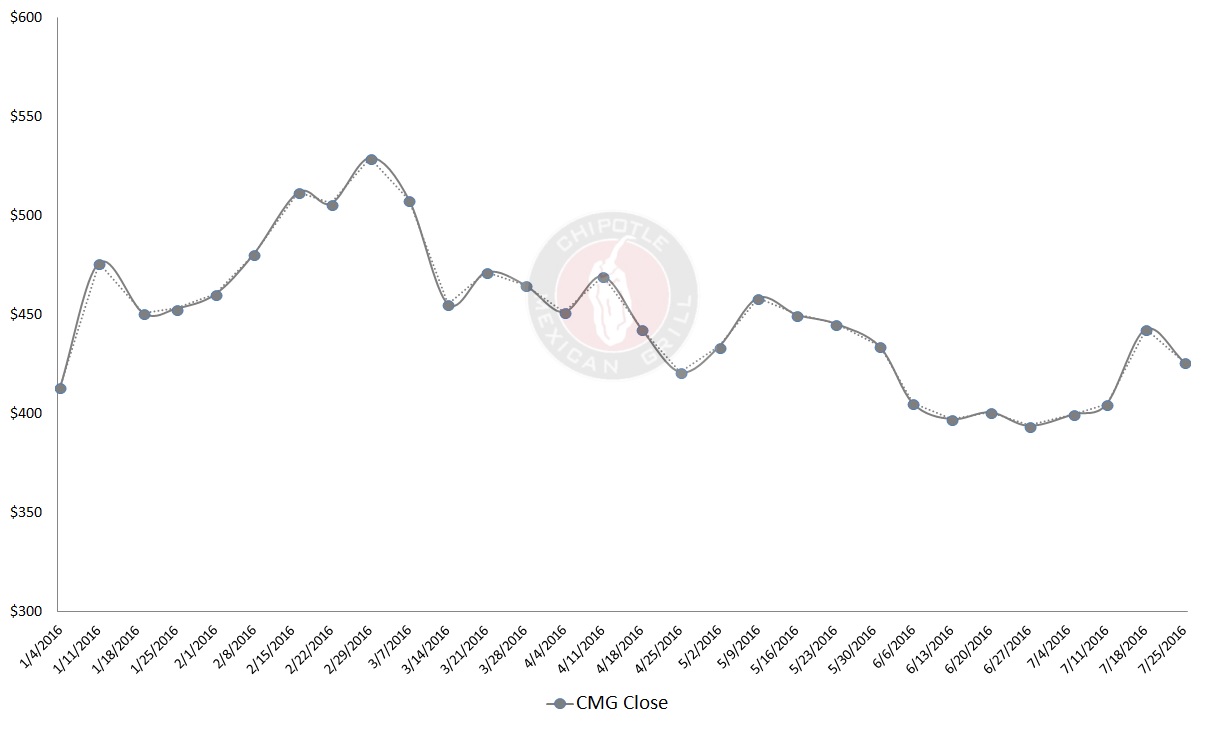

Among fast casual restaurant stocks, none have more to prove than Chipotle Mexican Grill, Inc. (NYSE:CMG). After getting slammed by a food poisoning controversy, CMG is throwing everything at efforts to rejuvenate itself. Unfortunately — by a cursory glance at both the technical and fundamental picture — those efforts seem to be going nowhere.

Last week, CMG reported earnings for Q2. The results, like the tainted food it had earlier served, were not good.

Click to Enlarge

It’s the same old story, and that should worry investors. Revenue growth for CMG in Q2 did pare back some of the losses experienced in the prior quarter, but not by much. Since Q4 of last year, sales growth is negative at 15.6%. Worse, margins across the board continue to decline thank their various “BOGO” promotions, which is killing profitability and not doing much in winning back customers.

It’s harsh, but CMG shouldn’t be viewed as a recession barometer — they’re more than busy shooting themselves in the foot.

Rotting Restaurant Stocks: Panera Bread Co. (PNRA)

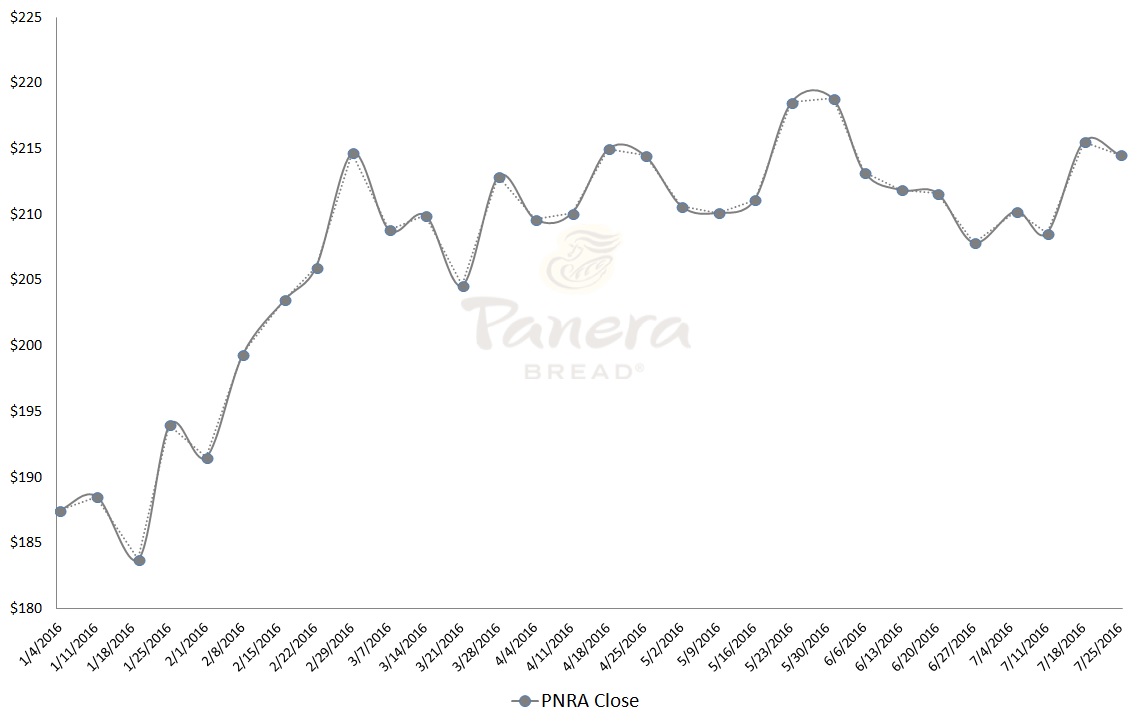

Another popular eatery among fast-casual restaurant stocks, Panera Bread Co. (NASDAQ:PNRA) may look like the epitome of success. PNRA is up double-digits this year at a time when things aren’t looking so great in the global financial markets. And over the trailing decade, PNRA shareholders have added 330% to their portfolio. But the good times can’t last forever, and Panera might be due for a tough lesson.

Admittedly, there’s nothing that PNRA has done that would immediately cause investors to lose faith. Their Q2 earnings released earlier this week showed that same-store sales were continuing to move in a positive direction. Margins up and down the income statement have demonstrated signs of stability. In addition, free cash flow has stayed relatively consistent over the long term.

Click to Enlarge

Yes, the majority of analysts are bullish on PNRA. However, with Panera’s price earnings ratio well above the median for restaurant stocks, it’s going to be harder to justify taking a risk. Plus, the threat of a recession — either within the industry or the economy — doesn’t make PNRA any more compelling.

Certainly, PNRA has earned everyone’s respect as a top performer, but even the best can’t float above market pressure indefinitely.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.