Being a long-term shareholder of PayPal Holdings Inc (NASDAQ:PYPL) isn’t the easiest thing in the world. Although it’s one of the leading innovators in the markets, PayPal stock hasn’t quite lived up to expectations. Year-to-date, PYPL is up 2.9% — not bad, but certainly not great. Since its initial public offering, early investors have added 10% to their portfolio.

Again, it’s better than the spectacular implosions we’ve seen among new IPOs, but where’s the meat?

Part of the problem is valuation. Currently trading at over 34 times trailing earnings, the price-to-earnings ratio for PYPL stock is over twice the median value of the global credit services industry.

Despite producing solid quarterly reports — it has an average earnings surprise of 4.4% — its net margins are middle of the ground compared to the competition. Also, growth trends in the bottom line have been erratic.

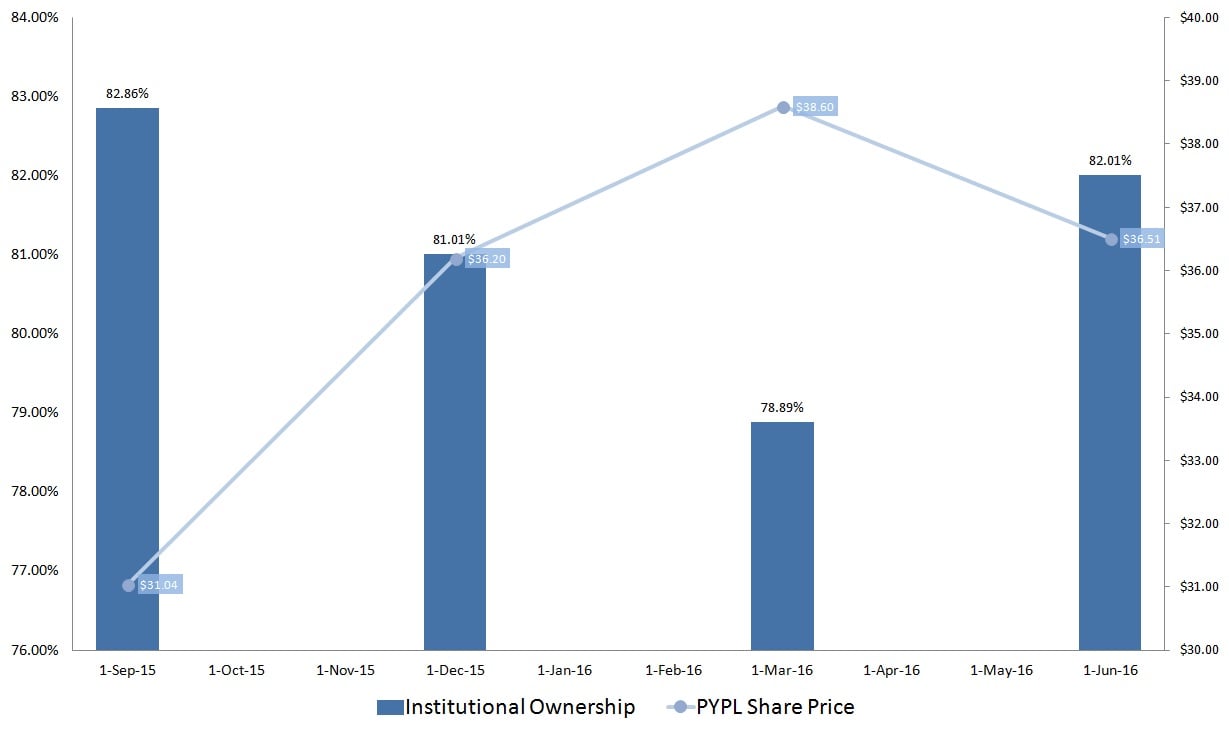

Another problem is institutional ownership of PayPal stock.

At its current read of 82%, that’s a bit on the high side. Although it’s not a deal-breaker by any means, excessive institutional ownership can produce counterintuitive dynamics. As in horse racing, too many people on one side of the trade produces a lesser payout.

Click to Enlarge

Interestingly, there is an exceptionally strong negative correlation between institutional ownership and the PayPal stock price. This indicates that Carl Icahn trimming his exposure to PYPL stock isn’t necessarily bearish.

It goes without saying that there’s a potential for a mismatch between fundamental strength and technical performance. The ebb-and-flow of institutional money in PYPL is clouding what should be a steadily rising stock.

PYPL by the Numbers

The facts speak for themselves. Based on its customer account balance of $13 billion, if PYPL were a bank, it would be the twenty-first largest in the U.S. Another interesting statistic is that the average balance for a PYPL user is $70.

While that sounds like a petty amount, consider this: According to a consumer survey by Alphabet Inc (NASDAQ:GOOG, NASDAQ:GOOGL), a majority of Americans have less than $1,000 in their savings account. The company penetrated the financial services sector much more than most people realize.

PYPL stock is also the beneficiary of a macro trend in consumer spending habits. According to American Consumer Credit Counseling, 80% of Americans prefer to use their debit cards for frequently recurring purchases. Only 14% used physical cash for such transactions. Even more astonishing, virtually all of young Millennials — those aged 18 to 24 years — used debit cards for everyday purchases. It’s no longer an anecdotal observation. Cash is quickly going out of style.

On top of all that, the company has three digital wallets: PayPal, Xoom and Venmo. The latter, a money-transferring app, is especially causing headaches for the big banks. In response, a group of large lenders, including names such as JPMorgan Chase & Co

. (NYSE:JPM) and Bank of America Corp (NYSE:BAC), have teamed up to create clearXchange. This is a payments network that facilitates convenient money transfer services among different banking accounts.

PayPal Stock Can’t Be Caught

To be chased by some of the biggest institutions in the country is a major bonus for PayPal stock. What’s an even bigger bonus is that these large lenders may not succeed in their endeavor.

Millennials just don’t trust the institutions that prior generations once did. According to Time, young Americans are much more likely to trust the advice of their peers, using social media as way to convey that faith. Hence, the rise of bitcoin, and not so much stodgy firms like JP Morgan.

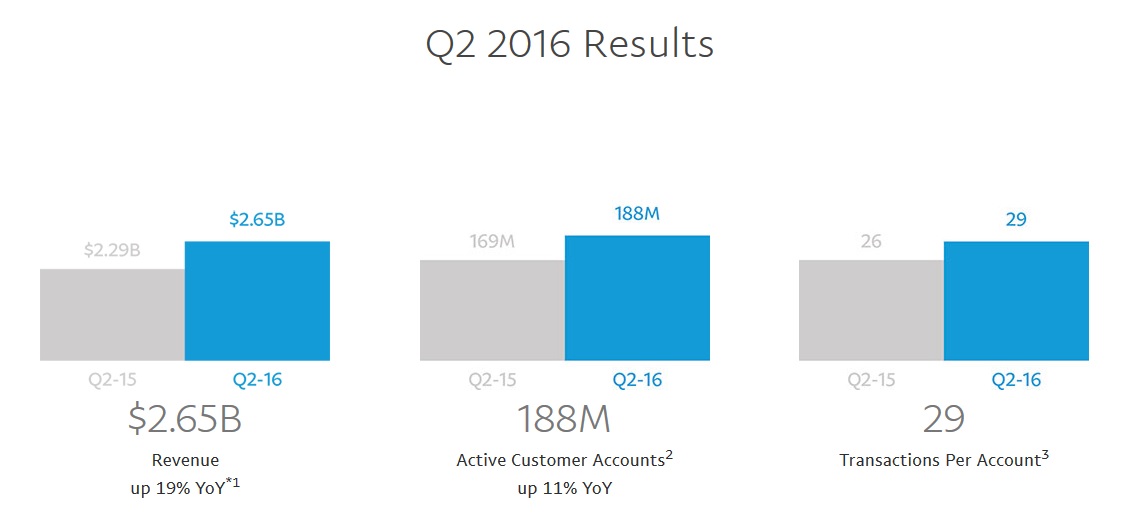

Again, the hard numbers are impossible to ignore.

Click to Enlarge

Not only does PYPL stock continue to impress against earnings expectations, other key metrics are out of this world. Active users have grown to 188 million, up 11% year-over-year. Each of those accounts averages 29 transactions, up another 11% YOY.

That’s especially important, as it proves new account growth isn’t just nominal, but substantive. Additionally, Venmo payment volume is rapidly approaching $4 billion, which has grown 141% from the year-ago level.

The bull case for PayPal stock is admittedly difficult from a technical perspective. Since its IPO, PYPL has basically ping-ponged its way to mediocrity. I argue, though, that factors outside of the company’s financials or industry fundamentals are responsible for the unexciting returns.

Against the vast majority of data, I believe PYPL stock stands on favorable ground. The world is steadily becoming cashless. PayPal is a trusted leader in digital payments. The math really solves itself.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.