There’s no diplomatic way to say it — hotel stocks have been one of the most disappointing sectors recently. Despite a supposedly recovered economy, not many folks have received the memo. After soaring for much of this decade, the PowerShares Dynamic Leisure & Entertainment Portfolio (ETF) (NYSEARCA:PEJ) has spent the last two years justifying its existence. The fund’s one-step forward, one-step backward approach has been unfortunately mimicked by multiple hotel stocks.

As anyone can imagine, the news that China’s HNA Group would buy a 25% equity stake in Hilton Worldwide Holdings Inc (NYSE:HLT) was welcome news. The deal, which is worth approximately $6.5 billion, represents about a 15% premium against the current market price.

As anyone can imagine, the news that China’s HNA Group would buy a 25% equity stake in Hilton Worldwide Holdings Inc (NYSE:HLT) was welcome news. The deal, which is worth approximately $6.5 billion, represents about a 15% premium against the current market price.

China sees hotel stocks as a viable, long-term investment, given its booming outbound tourism industry. U.S.-based Blackstone, which is on the other end of the HLT deal, apparently doesn’t share the same sentiment.

However, reading too much into HNA’s buying splurge would be a mistake. For one thing, hotel stocks barely budged on the news. Adding insult to injury, HLT shares popped up during early morning trading, but gave up virtually all of the gains by the afternoon close. The final verdict? A 3-cent rise for all its troubles.

The lack of technical enthusiasm is disturbing. For quite some time, hotel stocks have been marketed under the China banner. Home to the world’s second-biggest economy, the Asian giant has one of the fastest growing hotel markets. Furthermore, inbound tourism is sharply on the rise.

The problem is that we’ve been hearing the same jive from all international hotel stocks. Nothing has really changed. Ripping a page off a tired, old playbook won’t help matters. Here are three hotel stocks to which you shouldn’t bother checking in.

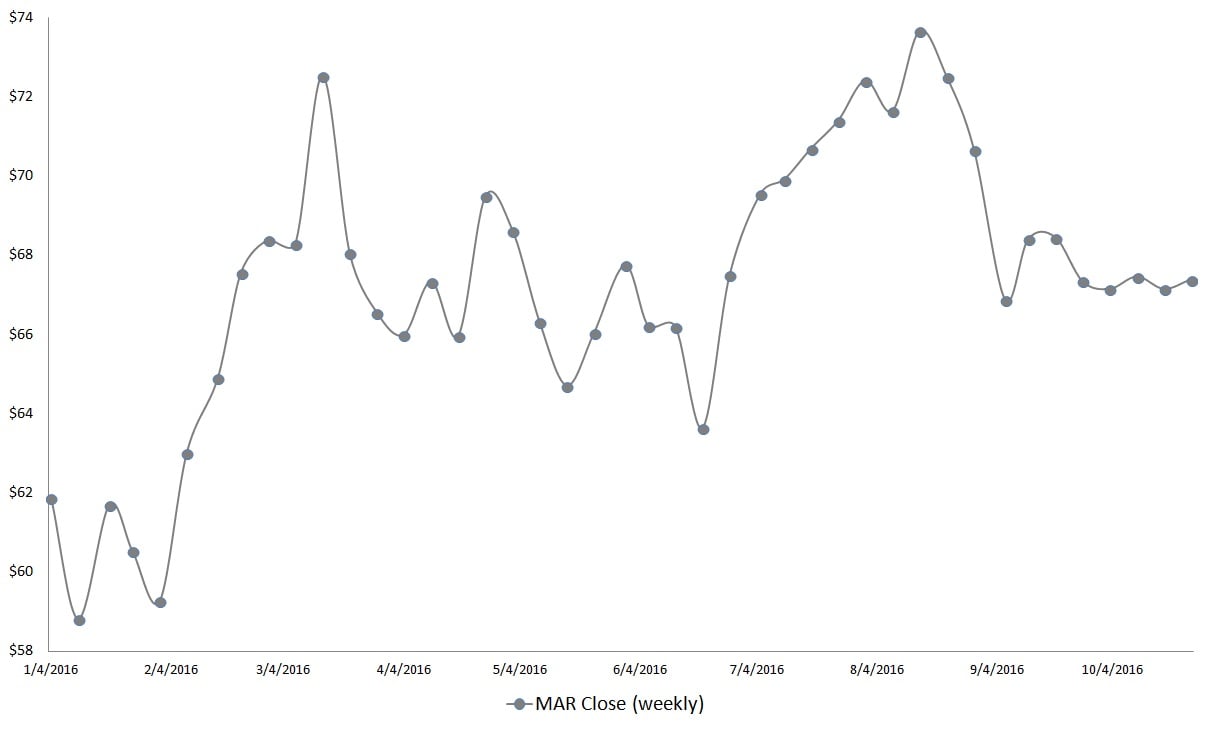

Hotel Stocks to Sell: Marriott International Inc (MAR)

Click to Enlarge

You can’t blame Marriott International Inc (NASDAQ:MAR) for trying. A few days ago, MAR, via its “Moxy Hotels” brand, hosted an “epic party” in Berlin. Celebrating the city’s notorious nightlife, the party was an attempt by Moxy to ramp up its Millennial “street cred.”

With demographics and buying power shifting towards the younger generation, Marriott sought to capitalize on the trend. But surely, the company is risking off-putting its core clientele.

MAR is a family-friendly business. This isn’t some cheap, seedy motel chain frequented by truckers and serial killers. Thus, I can’t help but view the Moxy brand as more of a liability than an asset. Apparently, I’m not alone in my opinion. Marriott has been racking up debt at a significant pace for most of this decade. Its financing has only led to mediocre growth in profitability margins compared to other hotel stocks. Additionally, its revenue performance leaves a lot to be desired.

Of course, that isn’t solely because of the Moxy stain. But if MAR was making the right calls, you’d expect to see some results in the markets. As of now, shares are essentially level for the year. Making matters worse, MAR stock has been frozen for nearly a month. The aforementioned Hilton deal barely nudged Marriott from its deep slumber.

Whether it’s deliberately hibernating, or investors can’t figure out what to do with it, MAR just doesn’t inspire confidence.

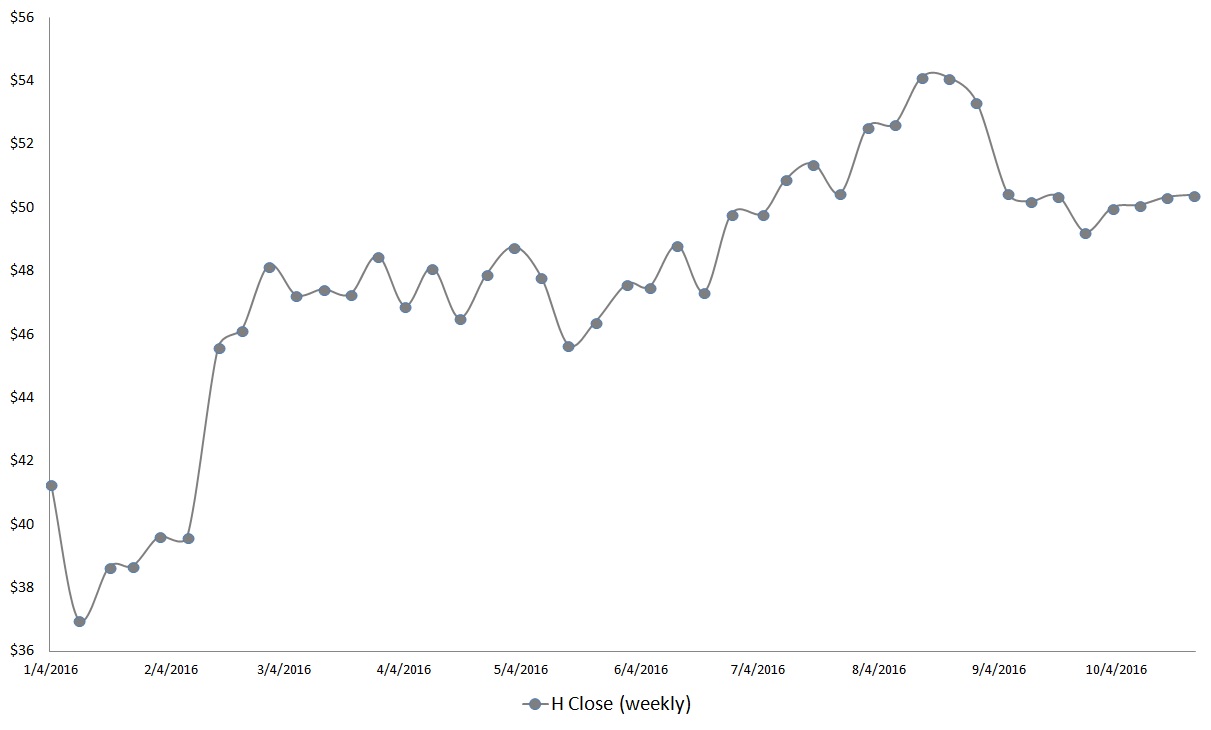

Hotel Stocks to Sell: Hyatt Hotels Corporation (H)

Click to Enlarge

One of the great thinkers of our time, former President George W. Bush once remarked “Fool me once, shame on you; if you fool me, you can’t get fooled again!” And I reckon I’d be a fool for not getting apprehensive about Hyatt Hotels Corporation (NYSE:H).

People may argue that H shares are up over 3% year-to-date — pretty good for hotel stocks. Yet Hyatt has the appearance of a drunkard walking on a precarious ledge.

My first concern is to point out the massive selloff that occurred early this year. Between Jan. 4 and Jan. 20, H stock lost nearly 21% in the markets. One could say that most other industries did poorly as well. However, it reinforces the idea that hotel stocks are very much dependent upon a healthy consumer base. If that goes awry — and let’s face it, there’s a lot wrong with this “economic recovery” — shares of Hyatt could slip again.

I could be proven wrong, but I don’t see where the enthusiasm would originate. At best, the financials for H stock are okay. The debt level is fairly high compared to its equity, and it doesn’t really have much to show for it with a mediocre return on equity ratio. Profitability margins are also middling, and its three-year revenue growth is better than average, but that’s about it.

If you’re looking for fireworks, Hyatt stock is not it. If you have a longer-term outlook, it still wouldn’t do. Bottom line — it’s time to check out.

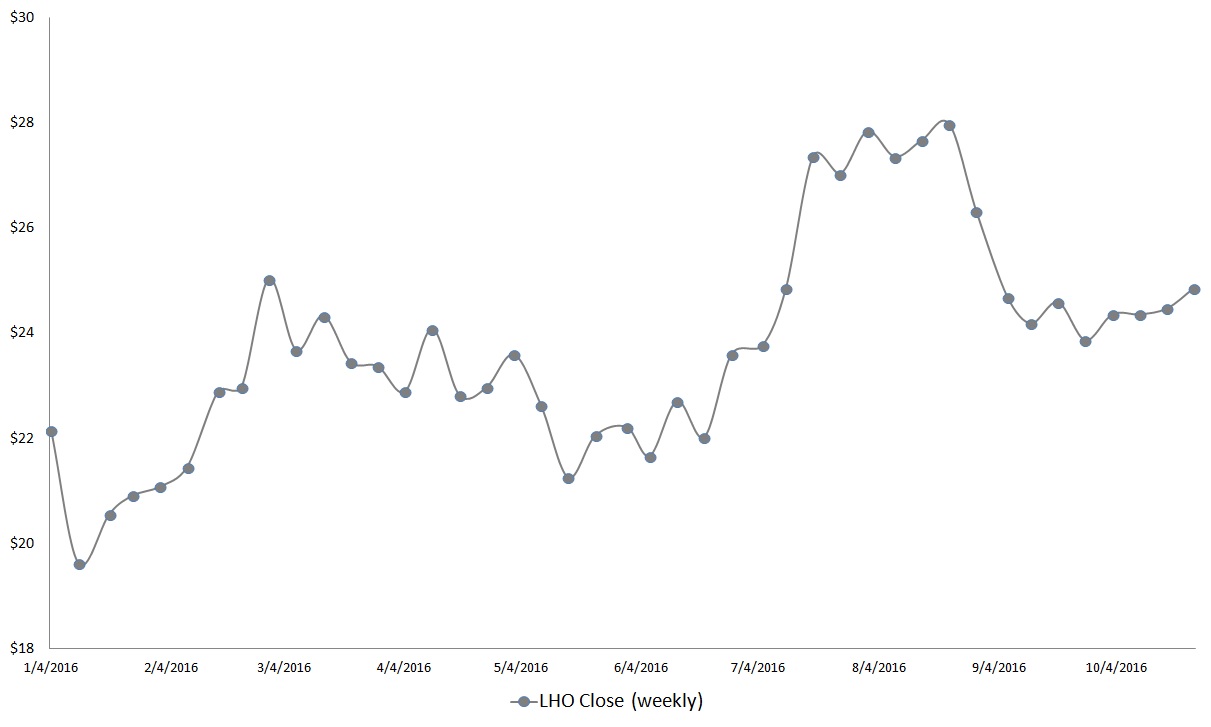

Hotel Stocks to Sell: LaSalle Hotel Properties (LHO)

Click to Enlarge

Unlike the “pure” hotel stocks mentioned on this lineup, LaSalle Hotel Properties (NYSE:LHO) is a real estate investment trust that owns interest in roughly 50 hotels across ten states.

Although it is limited in coverage, LHO focuses exclusively on prime investments, including Hotel Amarano Burbank and Hilton San Diego Gaslamp Quarter. However, serving an affluent clientele hasn’t exactly given LaSalle the upper hand against hotel stocks.

Like so many in the hospitality business, the financials for LHO are a mixed bag. On the positive end of the spectrum, LaSalle has a solid balance sheet backed by efforts to reduce its liabilities. That has given LHO a favorable return-on-equity ratio. However, the not so positive side is that profitability margins are very poor compared to the hospitality REITs. Also, quarterly revenue trends have declined significantly, which is a red flag.

The perception problem is obvious. If hotel stocks are supposed to be so great, why aren’t the top-tier channels outperforming? And if the economy has recovered, why aren’t the rich spending money? This confusion is reflected in the technical charts of LaSalle. I see plenty of ups and downs for the year, netting a disappointing 1% loss.

Similar to the underlying sector, LHO has spent too much time running in circles. I fail to see how that would be attractive to a Wall Street fat cat.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.