If you were sage enough — or just gutsy — to buy railroad stocks near their bottom, life is good! The benchmark Dow Jones U.S. Railroad Index is up over 21% year-to-date. For those that timed it perfectly at the spike low of January 25, the index gained an impressive 41%. But just like anything in the markets, what goes up will eventually come down. For railroad stocks in particular, the challenges are hefty.

There’s no doubt about it — railroad stocks are on a tremendous run. However, even a cursory look at the Dow Jones sector benchmark implies caution. At its current level, the index is down nearly 21% from its high point of November 2014. Also, the average of the highs and lows of the year prior is roughly where the sector index stands today. Railroad stocks have reacted splendidly against what was looking like a catastrophe. But the question remains, where will they go from here?

There’s some logic associated with the bullish argument — the labor market on paper is improving steadily, and the broad commodity sector is clawing back earlier losses. Even the much maligned coal industry is witnessing a remarkable recovery. Because of these developments, investors have pushed up railroad stocks on the speculation that the worst is over.

That doesn’t necessarily equate to a bonanza for railroad stocks. One of the primary challenges is that macroeconomic shifts have caused massive changes in the competitive landscape. For example, lower fuel prices have caused trucking companies to steal cargo volume, and thus, profitability. In response, earnings for railroad stocks have been supported by sharp cost controls. But doing that caps growth potential, and also signals a pessimistic forecast for the industry.

While the sector won’t collapse outright, there’s far better opportunities available. Here are three railroad stocks that have likely reached their best destination.

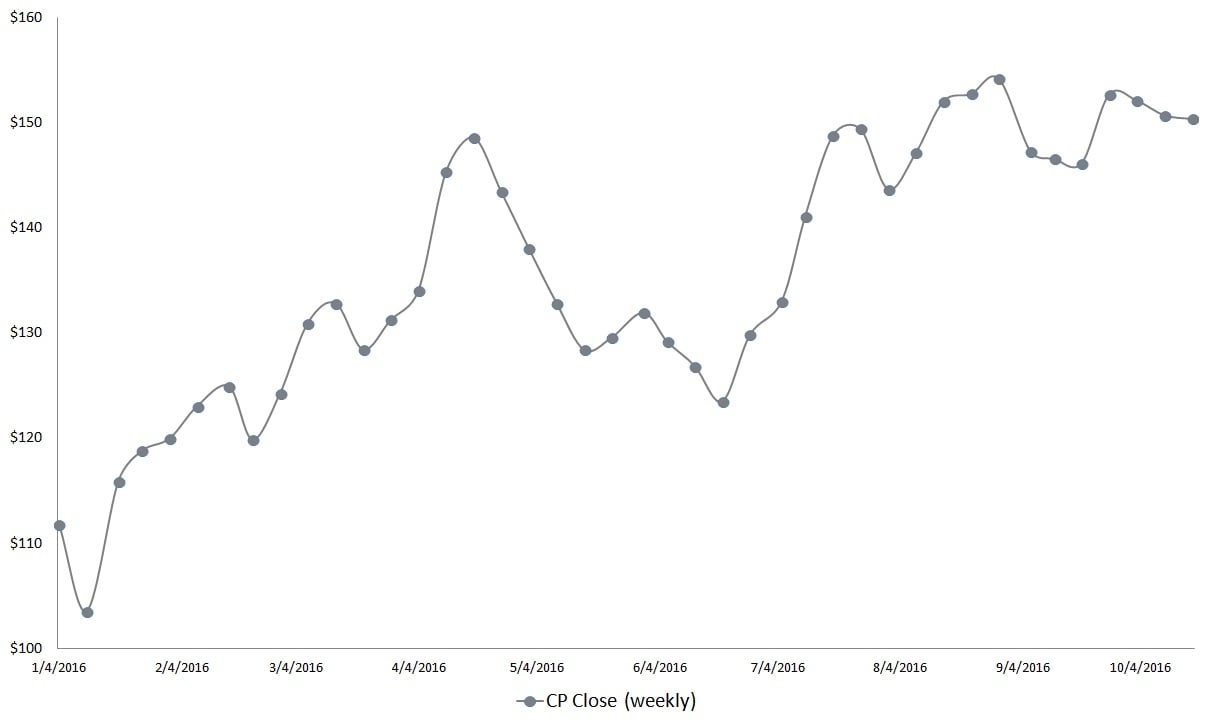

Railroad Stocks to Sell: Canadian Pacific Railway Limited (USA) (CP)

Click to Enlarge

By most measures, Canadian Pacific Railway Limited (USA) (NYSE:CP) is a success story. Activist investor Bill Ackman bought CP stock in 2011, which proceeded to nearly quadruple returns.

But Canadian Pacific lost some traction earlier this year compared to other railroad stocks, and Ackman responded in kind. Later in August, the Ackman-owned Pershing Square Capital Management would jettison its entire position in CP. If that’s not enough of a warning, I don’t know what is.

Renowned investors like Ackman see things for what they will be, not what they are. And the evidence shows that Canadian Pacific may be losing some of its charm. Sequentially, revenues over the past four quarters have been hurt by substantially reduced shipments of coal. For the upcoming third quarter of fiscal year 2016, CP is expected to turn in earnings per share of $2.80. That’s a sizable jump from the $2.67 that was forecasted one-year ago.

Some analysts are bullish on Canadian Pacific beating its earnings target due to an increase in grain exports. The issue of course is whether that’s enough to offset other areas in its business. But I think you have to follow the smart money here. There’s a reason why Ackman was so bullish earlier on CP and railroad stocks in general, and why he’s done a complete 360.

Actions speak louder than words, and the actions here tell me that Canadian Pacific may have peaked.

Railroad Stocks to Sell: Union Pacific Corporation (UNP)

Click to Enlarge

The common argument in support of railroad stocks is that the broader economy has stabilized. However, recent traffic volume in the U.S. and Mexico suggest otherwise.

While shipments for grains and automobiles have gone up, all other commodity groups — most notably petroleum products and coal — have gone down on a week-over-week basis. That sets a fairly pessimistic tone for Union Pacific Corporation (NYSE:UNP), which releases its Q3 earnings this Thursday.

Wall Street has toned down its expectations for UNP, which has an EPS target of $1.41. That’s two cents below the year-ago quarter’s estimate, which UNP handily beat. However, the company has had mixed performance over the past year-and-a-half period. This is essentially the new normal for railroad stocks. But for UNP in particular, the industry spiral has been rough. Over the last three quarters, revenue growth rates slid down 14%. That compares very unfavorably to rival CSX Corporation (NASDAQ:CSX), which is only at an 11% drop.

I can certainly understand and appreciate the technical argument. YTD, UNP is up 24%, well exceeding the return on the S&P 500. But even here, we have to be cautious on railroad stocks. United Pacific jumped 12% in the first half of the year. But over the past three months, shares have decelerated sharply. Whether it beats on earnings or not, the lack of nearer-term momentum reflects investors’ concerns.

UNP should be applauded for its strong burst right out of the gate. But going the full distance is another story altogether.

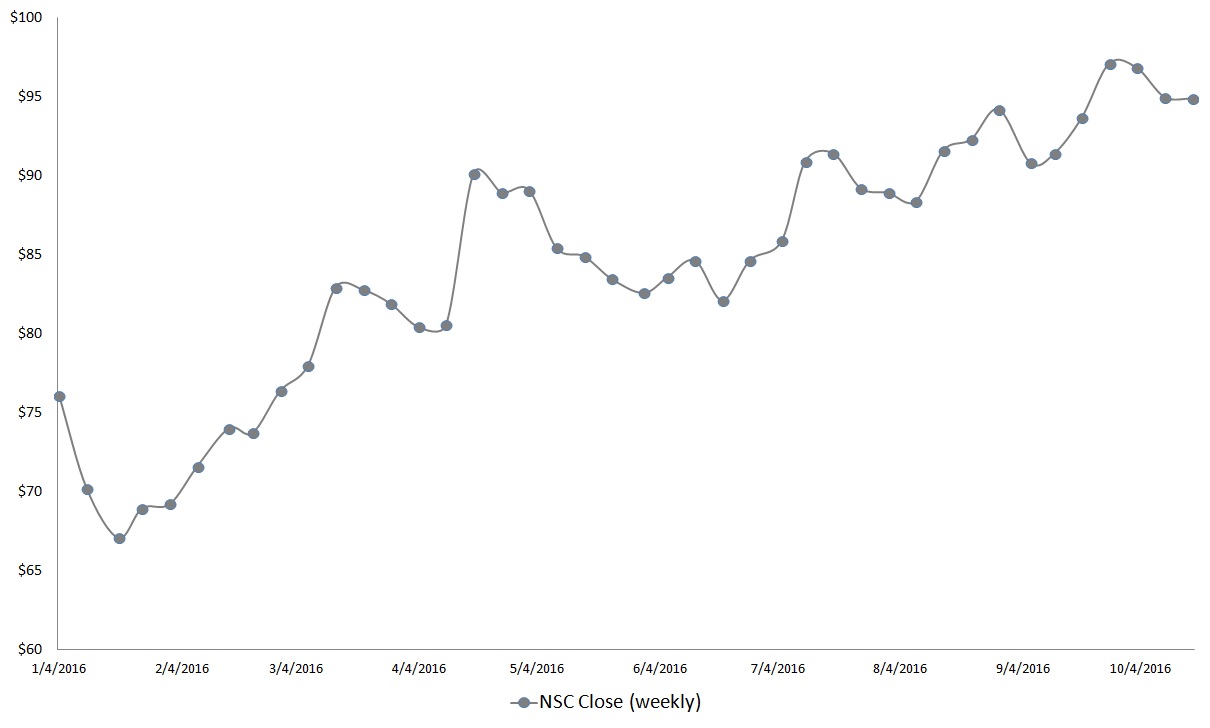

Railroad Stocks to Sell: Norfolk Southern Corp. (NSC)

Click to Enlarge

Among the featured railroad stocks, Norfolk Southern Corp. (NYSE:NSC) likely has the best opportunity to convincingly beat its Q3 earnings test next week. So far this fiscal year, the sales growth rate for NSC has declined 7.6%, which compares favorably against the competition.

In addition, Norfolk Southern is one of the few railroad stocks that has seen a recent lift in gross, operating and net margins. That led analysts at Bank of America to upgrade NSC to “buy” from “hold.”

Although these stats look promising, I would caution reading too much into it. Norfolk Southern could easily meet its $1.45 EPS target if grain shipments offset losses in petroleum, minerals and coal. The consensus is four cents higher than the year-ago quarter, but NSC had a solid beat that time. But riding on one sector to make up ground lost in a majority of other businesses is a tall order. I don’t think the modest improvements in profitability margins is enough to change minds.

Where the discussion ends for most people is in the markets. Like most other railroad stocks, Norfolk Southern is up double-digits for the year. But its returns during the last 30 to 90 days have slowed down. While it’s true that NSC is trading much better than the S&P 500 over the same time frame, it’s hard to imagine a scenario where the underlying economy does poorly but railroad stocks do well.

As bright of a star Norfolk Southern is in comparison to its peers, there are simply too many question marks hanging over the railroad industry.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.