Sometimes, events arise when even hyperbole is a severe understatement. That’s how I feel about Rite Aid Corporation (NYSE:RAD). RAD stock has one of the ugliest chart patterns for a NYSE investment, if not the ugliest. If you didn’t know any better, you’d assume that Rite Aid was a fly-by-night operation on its ways towards bankruptcy.

That’s not quite the case here, but who are we kidding? Long-term holders of RAD stock have been taken on a bloody ride, and the forecast calls for more pain.

Year-to-date, Rite Aid stock has dropped a sickening 54%. But the intense volatility is only half the story. RAD has drifted well outside any established technical support line. Any more bad news, and the pharmacy retailer could potentially end up on the dollar menu.

With fourth-quarter earnings looming, this is not the setup Rite Aid management was hoping for.

The Ups and Downs of RAD Stock

Wall Street is a brutal place, and it rarely cuts anyone slack. But you got to feel for the company — seemingly everyone is out to eat its young. And on Tuesday when it releases its Q4 results, I’m expecting nothing but a slaughterhouse.

Of course, my forecast is hardly groundbreaking. At best, recent earnings performances for Rite Aid stock are mixed. In Q1 and Q3, shares badly missed their respective earnings targets. For the upcoming report, consensus estimates for the quarter and the full year have declined sharply. To top it off, InvestorPlace ranks RAD stock as an “F” due to poor scores in sales and profitability.

Only a miracle could save Rite Aid stock under these circumstances, but unfortunately, Easter has passed.

Now to be fair, the vast majority of the pharmacy retailer’s woes centers on the “will it, won’t it” merger drama with Walgreens Boots Alliance Inc (NASDAQ:WBA). The matter has been discussed extensively by my InvestorPlace colleagues so I won’t dive into extraneous details.

However, I will point out that Dana Blankenhorn captured the mood accurately. Whether Rite Aid succeeds depends upon the

WBA merger. And that largely hinges on the divesture of a vast chunk of RAD stores to Fred’s, Inc. (NASDAQ:FRED). Also, regulatory authorities and perhaps the Trump administration will have to play nice. Mr. Blankenhorn insists its 50/50.

But as Ian Bezek notes, RAD stock has a tremendous, near-imminent upside. The latest terms for the merger calls for $6.50 a pop. At the current price of $3.80, the stock would enjoy a 71% boost. The sweet deal that Mr. Bezek referenced in his article just got sweeter in a mere 24 hours.

So, should you take a shot at Rite Aid stock?

Pharmacies Are Struggling

I will initially answer that question with a cheesy caveat — it depends. If you’re looking strictly to gamble on the Rite Aid merger and nothing else, Blankenhorn is correct. While President Trump wants to reduce regulatory burdens, our Commander-in-Chief has substantially more important issues to worry about.

From a longer-term investment point-of-view, I don’t need to hedge my bets. RAD stock is a stinker in a stinking market.

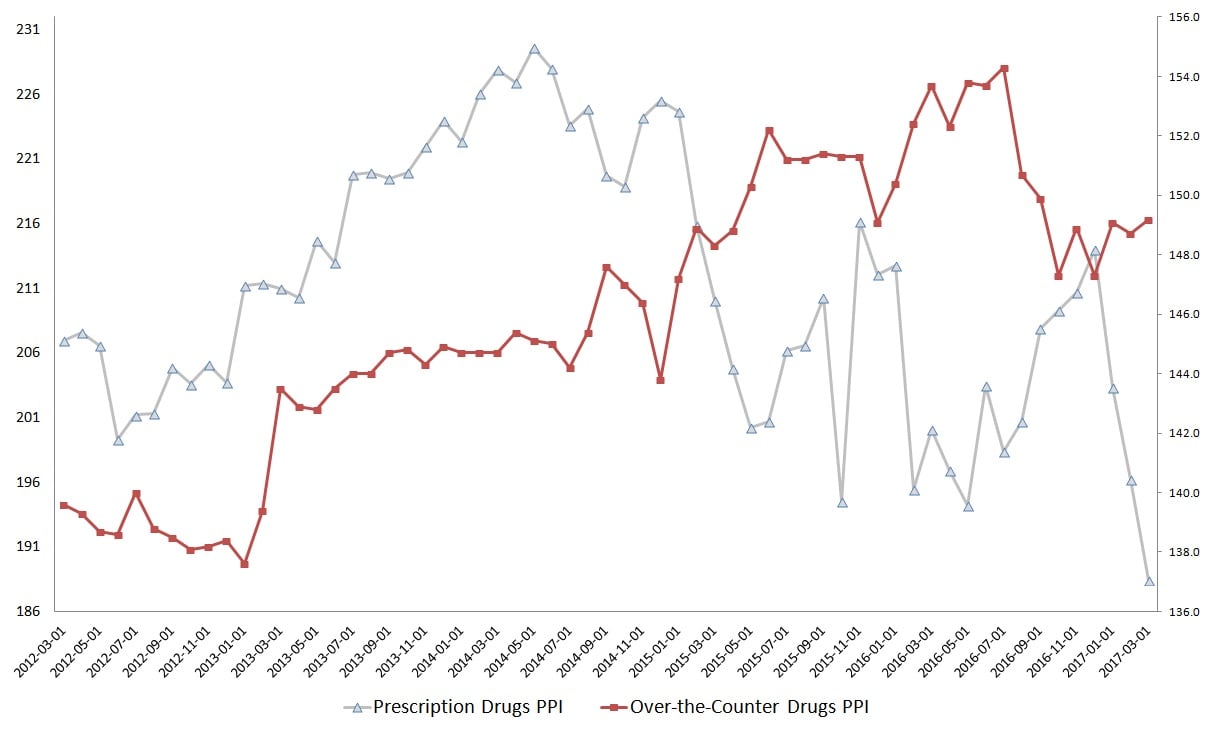

Click to Enlarge

Even worse, the allocation of the decline implies bad things for Rite Aid stock. Demand for prescription drugs fell sharply since the general election. Between November 2016 to March 2017, retail prescription PPI dropped 10.6%. The irony is that President Trump’s abrupt policies (relative to the prior administration) are causing Rite Aid heartache, yet they represent the best chance for survival.

Still, even if prescription demand started to pick back up, demand for over-the-counter drugs has softened in the past year. Thus, RAD stock faces a double-edged challenge. It has to win customers with serious medical issues, as well as those looking for a remedy for the sniffles.

To address this obstacle, Rite Aid would need to do something about its pricing. That runs counter to its profitability goals. Since the market itself is declining, the challenge is further exacerbated. In such circumstances, you want to go with your best option. Hint: it’s not RAD stock.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.