If investing alongside whales is your thing, Bank of America Corp (NYSE:BAC) should be on your radar. But instead of owning BAC stock outright, let me suggest a way to go long alongside Warren Buffett with a much greater margin of safety.

Warren Buffett’s Berkshire Hathaway Inc. (NYSE:BRK.A, NYSE:BRK.B) is sinking its teeth into a massive position in BofA. But this wasn’t a major reveal from Berkshire’s recent 13F — back in June, Buffett revealed that it will convert warrants it holds on Bank of America into 700 million shares of common stock. 700 million!

The investment firm will obtain its stockpile of BAC stock by selling a well-placed preferred-share bet of $5 billion in conjunction with exercising warrants which were placed in 2011 during more troublesome times as other investors fretted over Bank of America’s capital needs.

It’s a nice swap, and the move will make Berkshire the largest owner of Bank of America. And clearly, that makes Buffett bullish on the bank’s prospects. But let’s be clear: If you want to swim alongside a whale like Warren Buffett, buying stock today doesn’t offer the massive margin of safety the Oracle of Omaha maintains.

In converting his position, the cost per share is $7.14 for each of those 700 million shares. In relation to Bank of America stock’s current price of $24.47, that’s an open profit nearing 250%!

Having said that, let’s think about the now. There’s an uncertain interest rate situation, geopolitical tensions and bearish seasonality upon the market to contend with. So if you want to invest in BAC stock, let’s look at the chart for guidance, then the options pits for a strategy.

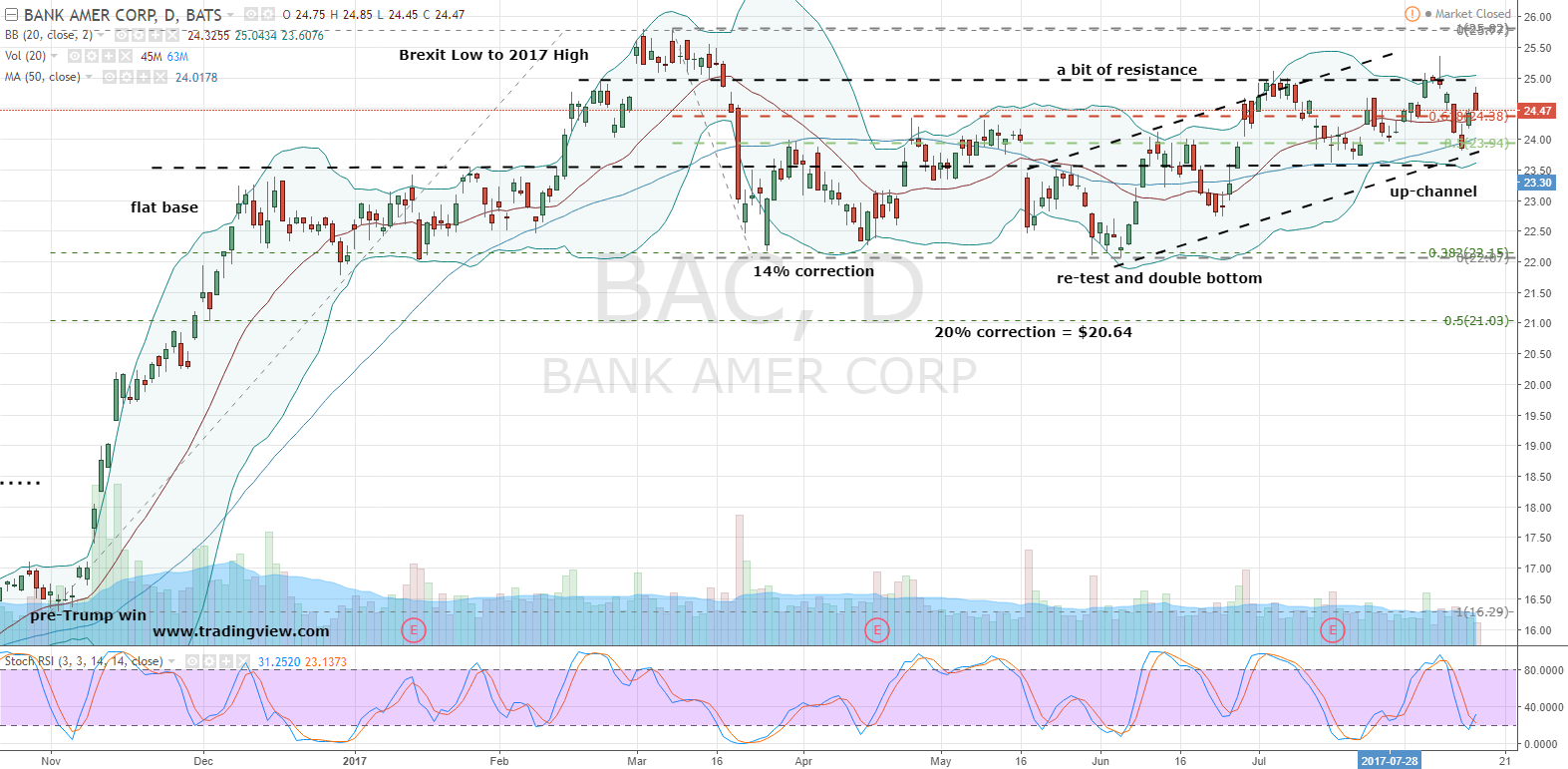

Bank of America’s Chart

Click to Enlarge

But there’s good news. A modest-but-chugging-along up-channel has formed amid 2017’s chop ‘n’ slop.

If a new higher high develops, it would put shares in a testing position of this year’s intermediate high of $25.77. Should that occur, we could see a breakout to new highs assisted by a new period of relative strength.

But let’s not get ahead of ourselves just yet.

The Play on BAC Stock

It’s not always a walk in the park to balance risk with reward. Given the circumstances surrounding Bank of America, I want to buy a moderately bullish long call butterfly.

One spread that looks good is the Sep $25/$26/$27 call combo. With BAC at $24.47, the butterfly is priced at 15 cents.

This position maintains a profit range of $25.15 to $26.85 at expiration in one month, and does so for just more than 0.5% of equivalent stock risk. The sweet spot would be if Bank of America managed to challenge the old highs. If shares landed on $26 at expiration, you would capture a profit approaching 85 cents, for a return of 567%.

Take that, Uncle Warren!

If BAC stock fails to rally by more than 2%, the entire debit will be forfeited. But again, the stakes are low. So if BofA tumbled for whatever reason, the added cost of buying physical shares would be minimal if you still want to take a long position alongside Berkshire.

Investment accounts under Christopher Tyler’s management do not currently own positions in any securities mentioned in this article. The information offered is based upon Christopher Tyler’s observations and strictly intended for educational purposes only; the use of which is the responsibility of the individual. For additional market insights and related musings, follow Chris on Twitter @Options_CAT and StockTwits and feel free to click here to learn more about how to design better positions using options!