Sears Holdings Corp (NASDAQ:SHLD) has been the laughing stock of the retail sector for years now. But with the space under so much pressure and SHLD stock consolidating, some investors are wondering if it’s time to buy. Let’s take a closer look at the stock and see if the worst is over with.

If you began following stocks this year with no regard to the past, one might think Sears is doing okay.

Shares are down just 8% in 2017 (which is good for SHLD, honestly). The company has teamed up with Amazon.com, Inc. (NASDAQ:AMZN) to sell its Kenmore brand exclusively on the latter’s platform.

Why Sears, Why?

But Sears made that deal in a position of weakness, not strength. It’s not as if home improvement retailers like Home Depot Inc (NYSE:HD) or Lowe’s Companies, Inc. (NYSE:LOW) are hurting. Heck, they’re some of the few retailers actually doing well right now!

Building on that point, Sears sold its Craftsman brand to Stanley Black & Decker, Inc. (NYSE:

SWK) for $900 million earlier this year. But again, the home improvement trend is strong.

Sears has this nasty trend in its management team, which is to sell off its best assets in order to keep the company alive. The problem? While its top assets may fetch top dollar, it leaves a carcass behind that’s rotting from the inside out. This is a poor strategy.

It’s not just Kenmore on Amazon and Craftsman to Stanley Black & Decker. SHLD spun off Lands’ End, Inc. (NASDAQ:LE) in 2014, a once strong-performing retail brand. Several years before that, Sears opted to sell off its most valuable store locations. On the plus side, this would bring in the most money. On the downside, these were the company’s best-performing locations. Had management kept its best stores (say one-third of total locations) and scrapped the rest, perhaps SHLD would be on better footing. Unfortunately, it did not.

Put simply, Sears has extended its life, but severely diminished its quality of life.

Sears Today

Today we’re looking at a stock in continual states of distress. In its most recent quarter, revenue fell by 20% year-over-year. Same-store sales fell nearly 12%. Going into the details does little good at this point. Sears reported another awful result and that’s all that really needs to be said.

The company hasn’t had positive free-cash flow in over five years. That should tell investors all they need to know right now about Sears. The same can be said for annual net income, which hasn’t been on the north side of $0 since 2011. Gross margins (since we can’t use positive operating or profit margins) have been in decline since 2007. Net cash and short-term investments stand at $236 million, a far cry from its $4.28 billion in debt. Total debt is now more than four times SHLD’s market cap.

Simply put, Sears wasn’t able to adapt. It lost its footing in the Great Recession, but it didn’t rebound like most retailers before the sweeping domination of e-commerce and Amazon rocked the sector. As a result, the situation at Sears continuously worsens — as has SHLD stock.

What’s the Move With SHLD Stock?

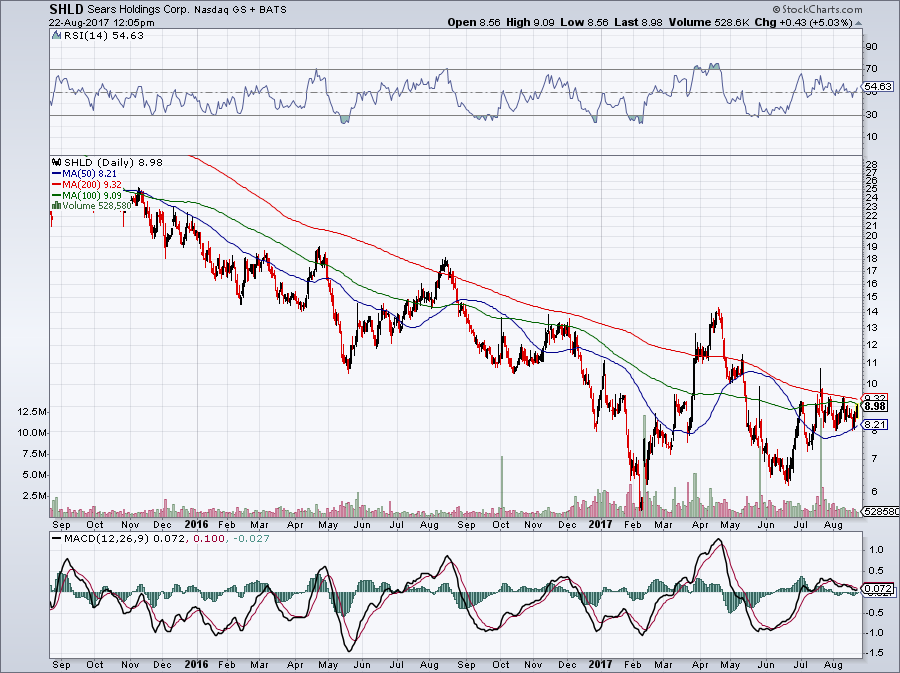

Click to Enlarge

In the short-term, SHLD stock has been consolidating near $8 per share. That’s a positive development for a retailer that has seen its stock fall from $28 to its current levels in two years.

Essentially with Sears, the longer the chart, the larger the fall. That’s definitely not a positive catalyst, even if shares are holding up right now.

All the trends are moving the wrong way for SHLD, which makes it a tough buy at the moment. But despite its dismal performance over the last decade, it’s an almost impossible short, too.

An astronomical 60% of the float is sold short, while CEO Eddie Lampert and his firm own a huge chunk of stock. Talks of going private have come up in the past and any such chatter could quickly send the stock into a short squeeze. The short train has left the station and if investors weren’t on it, it’s hard to get on now. As an example, consider that shares went from $6-and-change to almost $11 from mid-June to mid-July.

Not many could comfortably sit on a near-100% loss before SHLD stock went back down to $8. That said, buying SHLD stock is off the table as well, even with its latest licensing efforts. It’s too little, too late.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, he did not hold a position in any of the aforementioned securities.