Some investors ignore real-estate investment trusts (REITs) because they don’t quite understand them. After all, REITs are not the most straight-forward investment products out there. But they’re not as daunting as they may seem. It’s not as if they invest randomly in real estate — a market many deem too risky to touch ever since the Great Recession.

In fact, many REITs are very specific when it comes to their exposure. Some only invest in mortgage-based properties, commercial property, hotels, apartments, healthcare properties or data center properties.

Put simply, REITs come in many different shapes and sizes. This allows investors to gain exposure to specific sectors and industries. In order to qualify as a REIT, the company has to pay out 90% or more of its taxable income as a dividend.

One more key attribute to REITs? They’re different. Often times, they can buck stock market trends. As with everything, this can be both good and bad. Perhaps some REITs don’t participate as much during bull market runs. However, on bad days, these stocks can stay afloat. Take for instance Tuesday’s price action on September 5th. The Dow Jones Industrial Average fell more than 1%, while the Nasdaq dropped 93 basis points. However, names like CyrusOne Inc (NASDAQ:CONE) and Realty Income Corp (NYSE:O) all finished higher on the day.

That’s the kind of stability I like to see from my REIT holdings — a rare piece of green in my portfolio amidst a sea of red. Let’s take a look at our list of three REITs to buy, (hint, we just named one of them).

REITs to Buy: Omega Health (OHI)

Click to Enlarge

Omega Healthcare Investors Inc (NYSE:OHI) is a name many investors may glance over. With its near-8% yield, OHI stock is bound to catch the eye of a few income-hungry investors. I know it caught mine. This is further boosted by the fact that OHI operates in an attractive industry: medical real estate.

Specifically, Omega Healthcare operates in the U.S. and U.K. in skilled nursing facilities and assisted living facilities. As Baby Boomers continue to age, the demand for these types of facilities continue to increase. While in-home services could rival this on-site format, I would suspect that the latter will still continue to grow for decades to come.

Dealing with OHI specifically, it’s one of the most profitable REITs in the medical space thanks to its adjusted funds from operations (AFFO) margins. The company has raised its dividend 20 quarters in a row and upped its payout for 14 years straight. Long-term contracts help insure that that dividend payment continues to grow.

However, Omega’s AFFO isn’t growing much in 2017. That has caused its dividend payout ratio to climb, something that on the surface may concern investors. In my view, the company is still digesting its acquisition of Aviv REIT for $3 billion. In 2018, AFFO growth should accelerate, allowing Omega’s payout ratio to steady or perhaps even decline, even if management again raises its payout.

Omega Healthcare isn’t without risk. While it has a high yield, low valuation and strong industry trends, there are concerns. In-home patient care innovations could pinch margins at healthcare facilities. So too could government decisions surrounding Medicare and Medicaid, for which OHI has exposure to. Additionally, a few of OHI’s tenants have had trouble paying their rent on time, although management has downplayed this issue.

Every company has concerns and Omega Healthcare isn’t exempt. The bottom line? Omega is a lean operator with a high yield in a growing space. It deserves a place in any income investors’ portfolio.

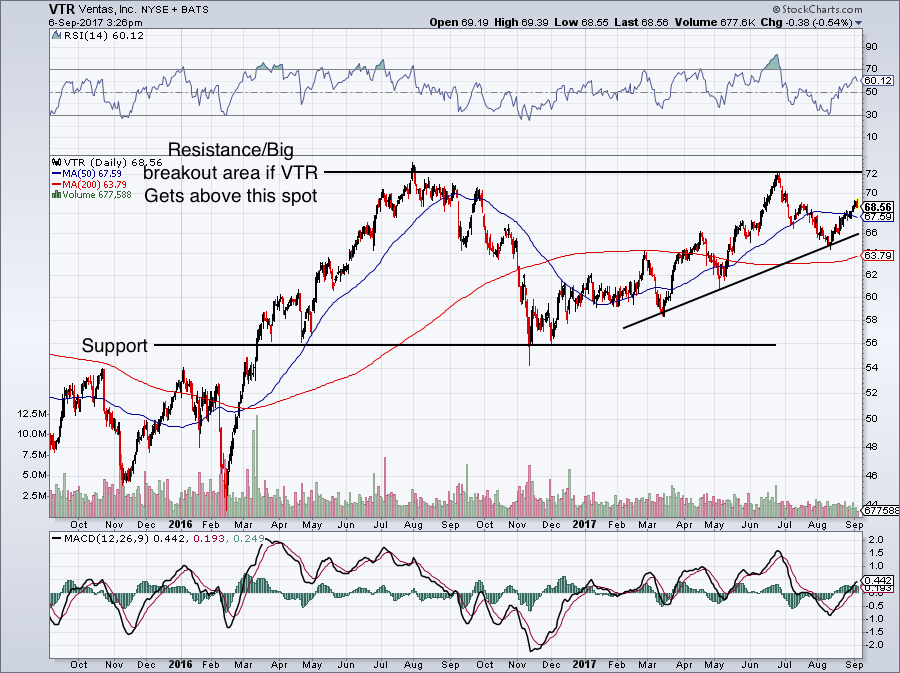

REITs to Buy: Ventas (VTR)

Click to Enlarge

Ventas, Inc. (NYSE:VTR) is another healthcare REIT. While OHI is considered a solid pick, many consider Ventas the blue-chip of healthcare REITs.

Despite the volatility that began the first two days of the Labor Day-shortened trading week, VTR stock is up almost 1% through Wednesday. For the year, it’s up an impressive 10.8% and currently yields a healthy 4.5%.

However, these numbers are nothing new to long-term investors. In fact, VTR has a compound annual return rate of 25% since 2000. It has grown its dividend by 8% per year for more than 15 years. While these figures are impressive, it may be unrealistic to expect it to continue going forward. That doesn’t mean Ventas is a bad investment, though.

Just like Omega Healthcare, VTR is poised to benefit from the surge of aging Boomers. While that’s an unfortunate part of the world, it’s also a realistic one. The 65-and-older population is forecast to double in the next 35 years, while the 85-and-older is set to triple.

Even in healthcare, REITs can differ quite a bit. Unlike OHI, Ventas has become less reliant on Medicare and Medicaid funding for its patients. In fact, they barely play a role in VTR’s operations. Instead, it utilizes higher-scale properties, many of which are paid for privately by patients and their family. Additionally, VTR also has very low exposure to the skilled nursing facilities, which make up a large portion of OHI’s business model.

So while Ventas investors may reap a smaller dividend than Omega Healthcare investors, many will argue that its business is of more sound quality. Still, it can be hard to turn away OHI’s dividend yield (which is nearly double VTR), so perhaps a combination of the two is warranted.

REITs to Buy: CyrusOne (CONE)

Click to Enlarge

CyrusOne Inc (NASDAQ:CONE) has been on fire this year. Those waiting for the pullback have not been satisfied as CONE stock continues to soar, up 45% on the year. As a result, it yields just 2.6%.

Who wants to buy a REIT that doesn’t even yield 3% right now?

Generally I’m in the same boat. If I want that kind of yield, there’s plenty of blue-chip stocks I can go to that have decent growth and a strong brand name. In this case though, CyrusOne may be an exception. The company is a data center REIT and as customer data, cloud and data storage becomes more important in businesses’ and consumers’ everyday lives, so too does CONE’s business model.

Last quarter, CyrusOne beat on revenue estimates, growing sales more than 28% year-over-year. In short, CONE is building out new facilities as fast as it possibly can, as it’s got a backlog of new tenants ready to “move in.”

This has led to strong dividend growth over the past few years. After growing the dividend 31% in 2014 and a whopping 52% in 2015, the payout has grown by “just” 19% and 10.5% in 2016 and 2017, respectively. The great thing about CONE’s business is that it’s centered in the middle of a huge, secular trend. Demand for data storage won’t fall anytime soon.

In REIT-land, just single-digit increases to the dividend are generally lauded by investors. So CONE’s double-digit growth, coupled with its monstrous revenue growth and the waiting list for its tenants has created a lot of demand for its stock. Hence, shares yield less than 3% and are up more than 40% in 2017.

After such a strong run, it’s only prudent that investors wait for a pullback. If CONE’s yield were to climb to 3% to 4%, I would certainly consider it a buy. Management expects to grow revenue to $1 billion by 2020 — almost double its 2016 results — and EBITDA to $550 million. Incredibly, it could exceed those lofty expectations.

This is why CyrusOne is a REIT to buy, but wait for a pullback first.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, he did not hold a position in any of the aforementioned securities.