Shares of Costco Wholesale Corporation (NASDAQ:COST) have not had a great 2017, but it has outperformed most of retail. Costco stock is up 1.3% so far this year compared to an 8% loss for the SPDR S&P Retail (ETF) (NYSEARCA:XRT). Many investors have come to know Costco as a blue-chip retail stock, but some may be wondering if that’s still the case.

Earlier this month, Costco earnings were released and the results were great. Sales grew 15.7% year-over-ear as earnings and revenue came in ahead of consensus expectations. Comp-store sales were up 5.7% for the quarter, but September was even better. The company (perhaps surprisingly in this day and age) still provides monthly sales figures for investors and in this case, released them on the same day as earnings.

Comp-store sales accelerated in September, climbing 8.9%. That’s much better than the comp-store results in the quarter and far better than its full-year comp-store sales growth of 4.1%. Despite this acceleration, shares fell from $167.50 to sub-$155 in two days.

What to Do with Costco Stock Now?

The fall seems short-sighted. I recently took a look at a research report from Cowen, which highlighted the growing overlap between Costco members and Amazon.com, Inc. (NASDAQ:

AMZN) Prime members. The concern is that as spending goes up at the latter, the former will see lower sales growth. It already sees less traffic from this particular demographic, so these concerns are legitimate.

The threat of e-commerce is real and given that threat, I found COST stock to have a rich valuation. I’m not the only one. Costco stock price trades at 28 times last year’s earnings and 23 times forward estimates. Sales are forecast to grow just 6.1% in fiscal 2018 (just starting Q1 now) and 6.4% in fiscal 2019. Earnings growth of 10.5% and 9.3% is forecast for those respective years.

That valuation is a tad lofty for essentially 10% earnings growth, but admittedly, it’s not the worst I’ve seen. I was hoping for a pullback to $150, as it would lower the valuation and be at a previous support level. Should we get a decent pullback in the market, perhaps Costco stock will eventually find its way down to that level.

In that previous article, the one linked above to Cowen, I said I would be more supportive of Costco if it were to elevate its e-commerce efforts. While it may be more costly than investors care for, it’s the company’s only chance at remaining atop the retail pyramid in the next generation of commerce.

Costco is rolling out two-day and same-day delivery and is partnering with Instacart in some circumstances. This is good Costco news. It will never be Amazon, but that’s not the point. And unlike Wal-Mart Stores Inc (NYSE:WMT), at least Costco has membership prices it can raise to help offset these costs.

Trading Costco Stock

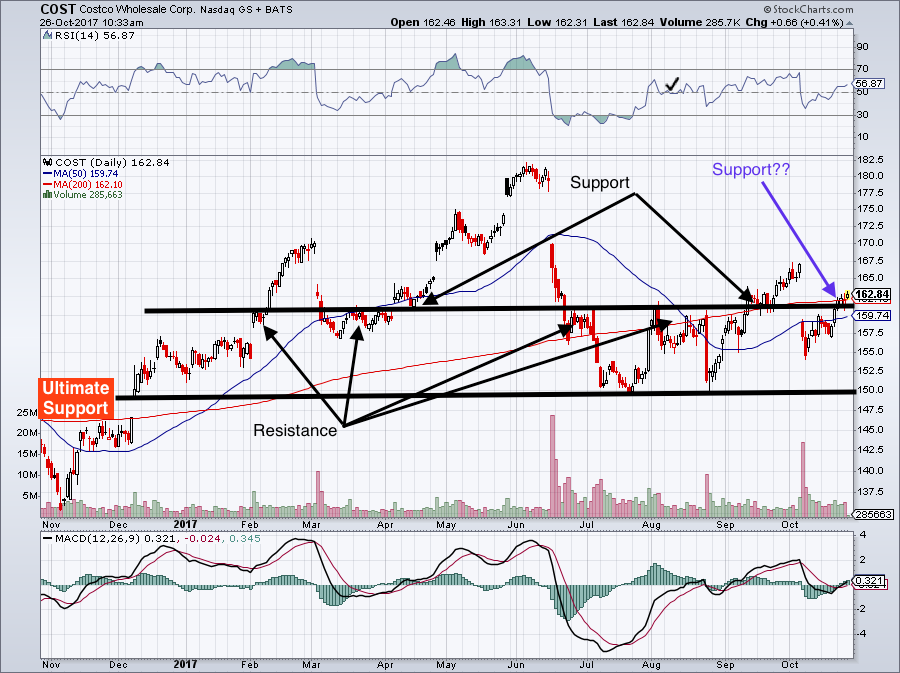

Click to Enlarge

COST stock has had a pretty bumpy year. But it’s firming up above the $160 level. This level has been both support and resistance throughout 2017. For bulls, it’s important for Costco stock to stay above this level. If not, the $150 to $155 level comes into play again. I would certainly be a buyer near the former, as $150 offers a low-risk long play.

While not big, there’s also the Costco stock dividend to consider. Currently yielding 1.25%, it’s a decent payout for someone willing to hold stock in a high quality company. Costco has consistently bumped its annual payout by more than 10% over the last several years, too. So while the payout may not floor investors, knowing they are getting a 10% or more raise each year is satisfying.

The Bottom Line on COST Stock

I know Costco is a high quality company that treats its employees and customers well. It’s also dependable for investors, offers a unique shopping experience for customers and can weather the retail storm. Its recent improvements to its e-commerce game make that last point especially true.

Admittedly, the valuation is only so-so in my eyes. I want to ignore it, but it’s just not that attractive. That’s why I want the stock on a deal. Previously we said to buy a pullback toward $150 and if you’re long, stay long unless it breaks below that level. We’re sticking to that plan, especially as the seasonally strong fourth-quarter is upon us.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.