Let’s not mince words: There’s little reason to bet against Microsoft Corporation (NASDAQ:MSFT) at this point. While some may be hesitant to plow funds into MSFT stock after its 22% year-to-date gain, there are reasons to stick with the tech giant.

On Thursday, MSFT stock hit an all-time high at $76, gaining 32% in the last year. However, there’s a reasonable case for it to climb another 13% over the next 12 months, to $86. That’s the new price target the analysts at Canaccord Genuity are using.

They upgraded MSFT stock to a buy, based on investors underestimating four main segments: Gaming, cloud, office productivity, and marketing. These segments should set up Microsoft for an extended period of growth. The most important part of the note to me?

“Revenue is split roughly evenly between marginally declining assets and high teens growth segments. As the faster growth segments increase as a percentage of the total, aggregate revenue growth should accelerate, which is generally a driver of multiple expansion.”

Valuing MSFT Stock

Why does this line mean so much? Because as Microsoft’s faster-growing businesses become a larger piece of the total pie, they will no longer be a footnote on the income statement. They will “move the needle” as investors like to say, especially when referring to new businesses for companies like Alphabet Inc (NASDAQ:GOOGL), Apple Inc (NASDAQ:AAPL) and others.

Here are the numbers: Microsoft trades with a price-to-earnings (P/E) ratio of 28. It has a forward P/E ratio of 21 and trades at 6.5 times sales. Analysts expect Microsoft to grow sales 8.1% this year and 7.6% in 2018. They expect earnings to grow 12.8% in 2018.

The valuation may not seem cheap at first glance. But I would look at some of Microsoft’s competitors. Namely, I would look at big-cap tech and the cloud. Names like Alphabet, Alibaba Group Holding Ltd (NYSE:

BABA) and Amazon.com, Inc. (NASDAQ:AMZN) come to mind.

Amazon does not have a comparable valuation footprint. Alibaba has a forward P/E ratio of 27, but will grow earnings and sales at a faster clip than Microsoft.

Alphabet perhaps draws the closest comparison, in my opinion. GOOGL stock trades at 24.5 times forward earnings and 6.83 times sales. In my view, Alphabet is worth more than MSFT, as it does have faster growth. While MSFT may not be worth 24.5 times forward earnings, it’s reasonable to say it’s worth 22.5x or 23x. Where does that put MSFT stock? Somewhere between $81.50 to $83.25. If revenue accelerates, MSFT could warrant a higher valuation.

Another way to look at it? Microsoft is the cheapest large-cap tech stock with a significant position in the cloud.

The Bottom Line for Microsoft

Click to Enlarge

If MSFT is growing earnings faster, it could push MSFT stock higher even with current valuation figures. Given that Microsoft has beat earnings estimates for eight straight quarters, this wouldn’t be too much of an ask. Additionally, it’s beat revenue in seven of those quarters. We have been a big advocate of Microsoft, and a large part of our case has been valuing it higher thanks to its cloud business and other robust segments.

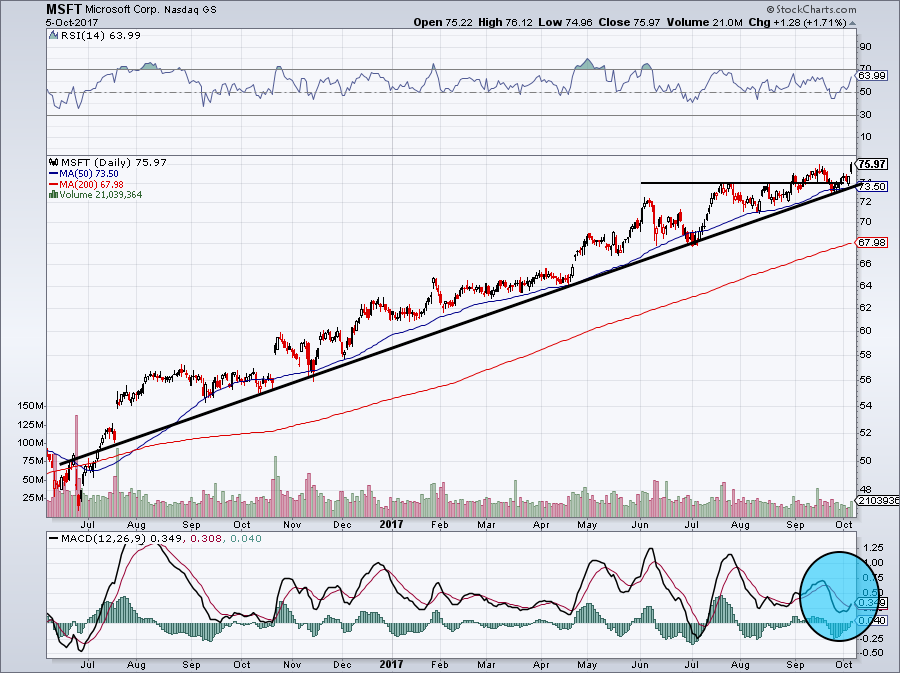

What do we do with MSFT stock at 52-week highs? I expect $74 to act as support going forward, as it was prior resistance. Additionally, the 50-day moving average (blue line) and strong trend-line support (black line) should act as support near that level. Additionally, we can see the MACD is turning bullish (blue oval) while the stock is not yet overbought in the short term.

Investors have a lot of support beneath current levels. Holding a long position here can be justified, as risk-adverse investors can bail on a break below these support lines. Its 2.2% dividend yield offers a small cushion as well.

It would be really constructive if we could get MSFT stock to consolidate between $74 and $77 for a few weeks ahead of its earnings on Oct. 26. Good news could send shares higher if that’s the case, especially if MSFT stock has had time to consolidate its recent gain.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.