I hate buying companies that have jumped substantially higher in the markets. By logical extension, I should really hate Micron Technology, Inc. (NASDAQ:MU). The semiconductor firm’s shares have gained more than 80% year-to-date. Even worse for those who like to get deals on the ground floor, MU stock doesn’t look like it’s going to fade any time soon.

The question now is, should investors bite the bullet? InvestorPlace contributor Bret Kenwell suggested that buyers should consider MU stock, with two caveats: that they’re aware of the risks; and, that they acknowledge they’re late to the game. That doesn’t sit well with bargain hunters, but being late is better than being sorry.

Of course, the real risk at buying-in at record levels in the MU stock price is gravity. If the fundamental arguments don’t pan out, you couldn’t pick a worse time to be caught flat-footed; hence, the currently declining volume against late-September’s figures.

Still, the fundamental argument is exceptionally compelling. As Kenwell articulated, MU stock crushed its fourth-quarter targets, explaining that:

“Fourth-quarter revenues climbed an absurd 90% to $6.14 billion. Earnings of $2.02 per share came in 10% higher than consensus expectations. The low end of the guidance range for both metrics next quarter came in ahead of analysts’ estimates. This was, in fact, a very good quarter.”

We’ll have to wait and see how the rest of the broader technology sector stacks up. So far, Micron stock is stacked up favorably against peers, such as Intel Corporation (NASDAQ:INTC), Advanced Micro Devices, Inc. (NASDAQ:AMD), and NVIDIA Corporation (NASDAQ:NVDA).

MU stock has strong arguments, no doubt about it. But are they enough to overcome the risks of buying so high?

MU Stock Cleared Important Test

Late last month, I made the argument that the MU stock price isn’t just the byproduct of trading dynamics. Instead, investors ought to consider the company’s entire context. When they do, it’s difficult not to envision that Micron’s fundamentals would eventually win the day.

The biggest catalyst is that the tech firm’s dynamic random access memory (DRAM) market is red hot. As the old adage goes, a rising tide lifts all boats. But MU has been steadily gaining

market share over the past few quarters. Subsequently, it’s also chipping away at Samsung Electronics Co Ltd (KRX:005930) dominance, giving Micron stock investors more reason to cheer.

Furthermore, the already-saturated smartphone sector shows no sign of decline, at least from the consumer perspective. Our own Richard Saintvilus stated bluntly that he would pay $1,000 for Apple Inc.’s (NASDAQ:AAPL) flagship iPhone. Crazy or not, that’s enthusiasm that you cannot deny, and one that Micron will take to the bank. By logical extension, the company may not be as overheated as the MU stock price suggests.

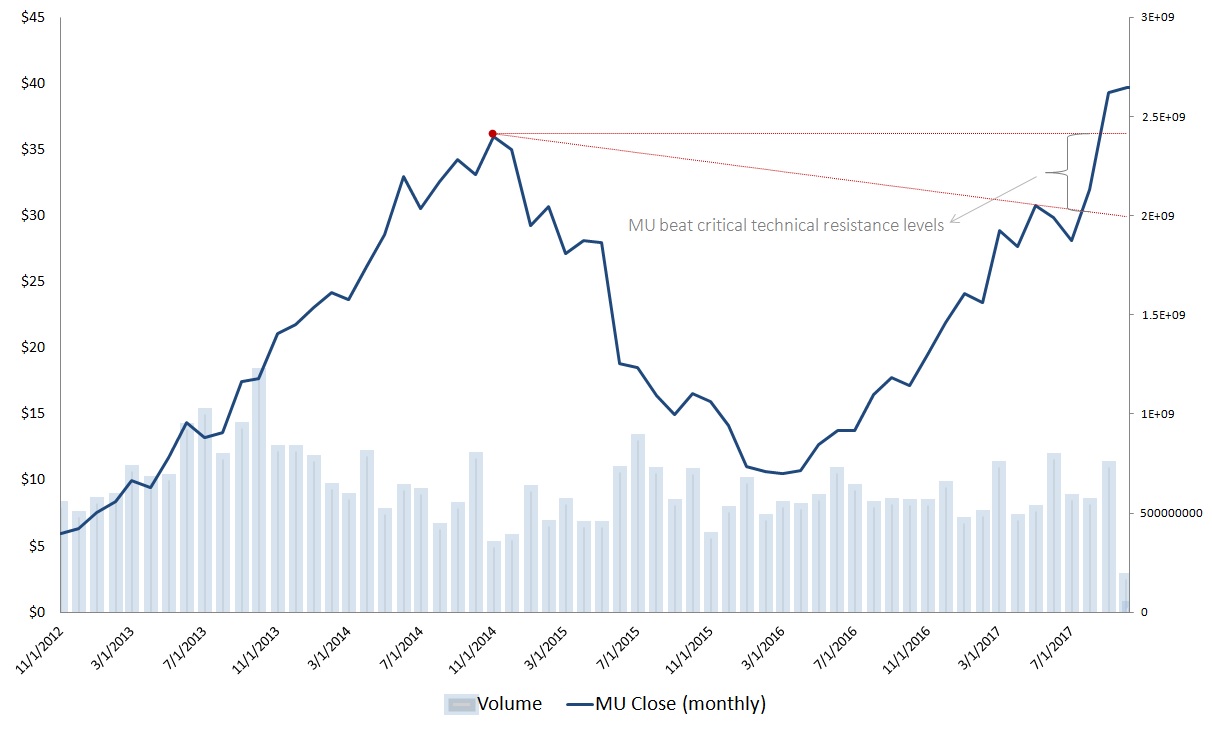

Indeed, the basis of whether Micron stock was believable depended on its recent price action. At the tail end of 2014, MU shares were struggling to break decisively above the $36 technical ceiling. Of course, they failed, which ushered in a horrific 2015 that many long-term investors are still trying to forget.

Click to Enlarge

Two weeks ago, when I wrote that “I completely sympathize and understand investors who are hesitant to jump aboard now, the MU stock price was again lurking around the $36 mark. Technical analysts call this chart pattern a double-top formation. Under the technical approach, double tops are bad news, signaling an inability for bulls to push the price higher. Psychologically, it was a make-or-break moment for MU.

Fortunately, things turned out on the right end for this once-deeply embattled firm.

MU Stock Shows Strong Signs

I’m not the only one that maintains a positive outlook on MU stock despite its exceptional gains. InvestorPlace’s Chris Fraley believes in the shares’ upside momentum, citing their resilience in the face of serious pressure.

Moreover, Fraley’s strongest argument is fundamental in nature. Referencing the Q4 earnings report, he wrote:

“Analysts foresee $2.14 EPS in the current quarter, on 60% sales growth. For fiscal 2018 (which, for Micron, began in September), the company is expected to grow EPS another 52%.

Despite such a gaudy earnings forecast, the stock trades at less than six times forward earnings estimates even after the recent jump from $34 to $40. Translation: for all its top- and bottom-line growth, Micron stock is still grossly undervalued.”

Naturally, it’s always difficult to buy something at a premium relative to historical prices. However, a good company is a good company, irrespective of what occurred in the past. In this case, MU stock has done more than enough technically and fundamentally to deserve a second look.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.