There’s no point in denying it. Netflix, Inc. (NASDAQ:NFLX) is a contradiction. While the top line is growing quite nicely, the bigger the company gets, the more cash it bleeds. Yet, there it is, NFLX stock just hit another record high despite investors being well aware that the company is insolvent on a GAAP cash-flow basis.

It’s a situation that vexes more than a few investors, forcing everyone to question what makes for a good investment. Must a name be profitable, or at least enjoy the prospects of profitability, or is any stock that simply moves higher a great pick?

So far for NFLX stock has been a great stock pick because it’s the latter. If you don’t think there’s a day of reckoning coming for Netflix though, you might want to digest the graphic below.

Mixed Message on NFLX Stock

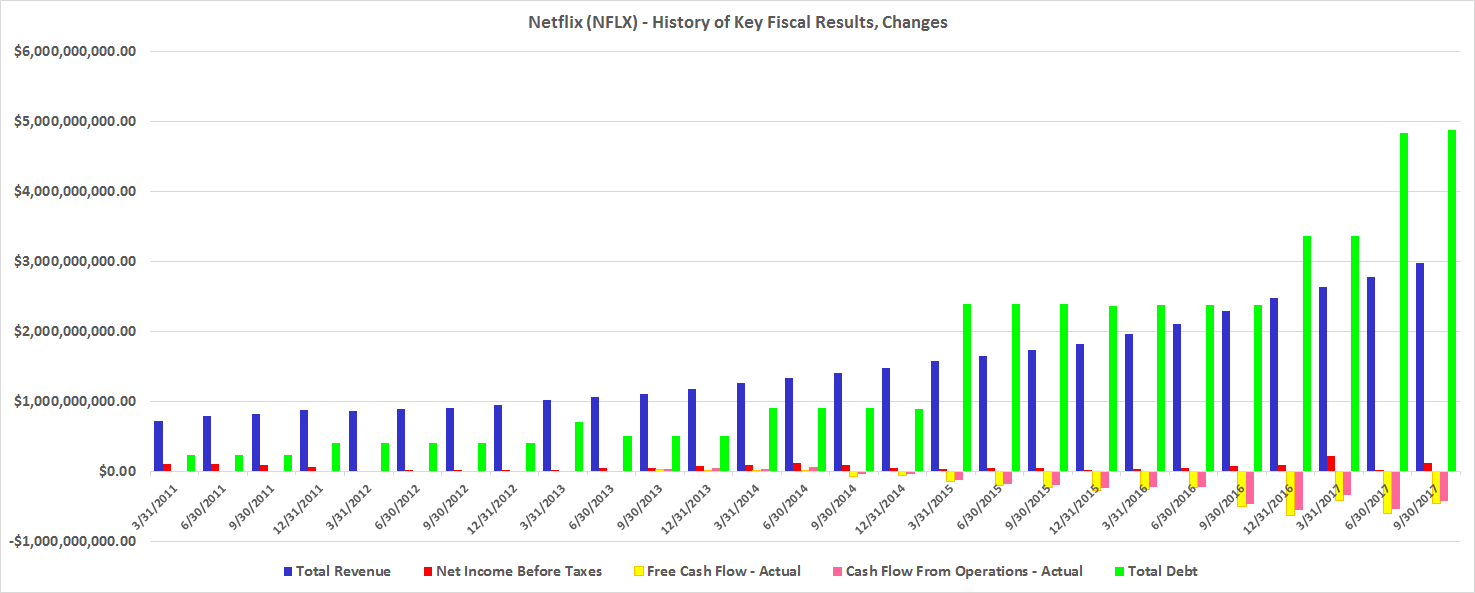

Every few months I go through the exercise of visually plotting all of Netflix’s key fiscal metrics, just so no investor can ignore some alarming realities regarding the company.

The most recent update doesn’t change anything from the previous look, making it clear that Netflix is (still) bleeding cash left and right, and is still walking deeper into debt, upping its revenue without upping its reported income nearly as much as it should be. Take a look.

Click to Enlarge

Yep, revenue is growing fast, but not as fast as debt. And, as quickly as revenue is growing on a year-over-year basis, negative cash flow tallies are becoming increasingly negative at a faster clip. Pre-tax income has barely edged higher since 2011 too.

It leaves current and prospective Netflix stock asking one key question: What’s the end-game here? Is there an end-game at all, particularly now that Walt Disney Co (NYSE:DIS) and Twenty-First Century Fox Inc (NASDAQ:FOXA) are on the verge of joining forces against Netflix.

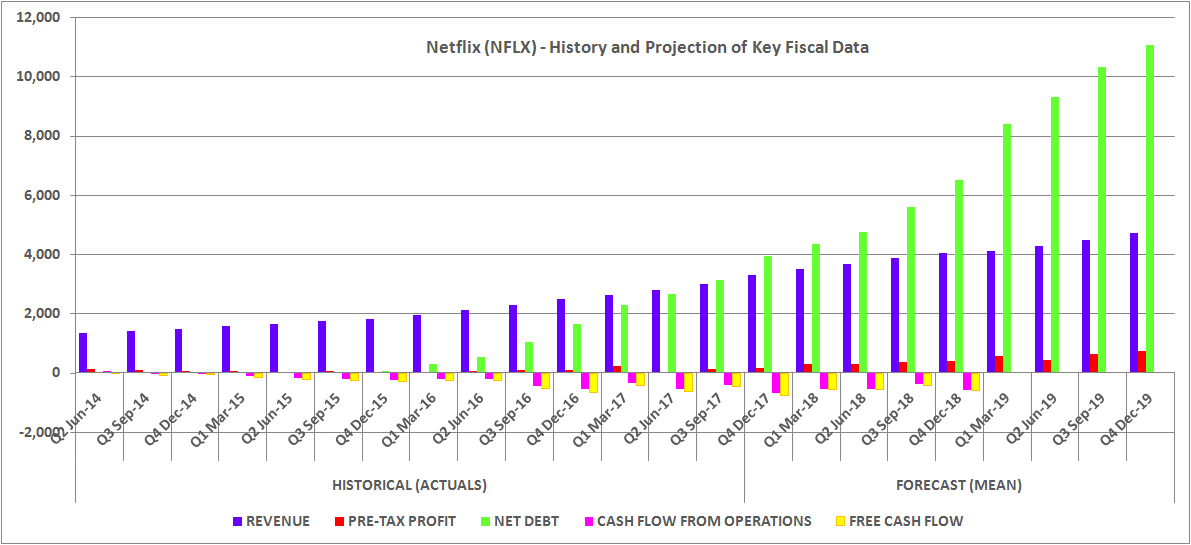

And for the record, analysts don’t expect the cash flow situation to improve significantly for the foreseeable future.

Click to Enlarge

The pros are currently modeling better pre-tax income beginning in 2019, but that’s optimism we’ve seen before. It can been and has been reined-in in the past. The widening profit outlook may also not fully reflect adjustments stemming from Disney’s deeper dive into the streaming space.

Either way, cash flow isn’t expected to meaningfully improve at any point in 2018.

Ever-Shifting Priorities

To date the bullish argument for NFLX stock has focused on the income statement, and dismissed the cash flow statement. Proponents say the former matters and the latter doesn’t. Fine.

Thing is, many of those very same investors argue that for other, similar companies.

Case in point? Amazon.com, Inc. (NASDAQ:AMZN), for one. Forbes contributor Hersh Shefrin hit the nail of inconsistency right on the head back in 2014, saying of the collective analysis of Amazon:

“When it comes to intrinsic valuation, free cash flow is king. Ultimately, the value of a stock to investors is determined by the cash flows associated with buying, holding, and selling the stock. When it comes to intrinsic valuation, earnings are not king. However, if enough investors base their decisions on earnings, and not free cash flow, then earnings will be the stronger driver of market valuations. Behavioral economists largely believe that in the long run, market prices do converge to intrinsic value, but recognize that this might take a long time to happen.”

Yes, free cash flow is king unless you’re talking about NFLX stock, where free cash flow somehow doesn’t matter. As Shefrin explained, if enough investors decide earnings matter more, “then earnings will be the stronger driver of market valuations.”

Therein lies the rub, and the frustration for all investors. Investors can deal with strange, ill-advised standards. They struggle to digest ever-changing standards, however, to reflect the prevailing rhetoric of the day concerning one stock or another.

And that’s where the crazy Netflix story turns scary. The nonsensical rules that apply today may not apply tomorrow. If the standards change for Netflix and suddenly cash flow is the bigger priority (or at least the top talking point), NFLX stock could find the rug pulled out from underneath it.

Welcome to the market.

Bottom Line for Netflix Stock

To be clear, none of this is to suggest NFLX stock won’t continue to rise, making it technically a good pick. The crowd’s sentiment is firmly bullish at this time, and right or wrong you never want to step in front of a stampede.

Still, nobody can afford to fool themselves about what NFLX stock really is. The fundamentals are lousy. The game here is riding the hype as long as it lasts, with plans to bail out before anyone else sees it coming… before the crowd decides cash flow matters after all.

That’s a very dangerous game to play.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.