Analyst opinions about Twitter Inc (NYSE:TWTR) stock are a lot like the weather in [insert your state here] — if you don’t like today’s, just wait until tomorrow, because it’ll be something else.

Case in point: On Wednesday, GBH Insights analyst Daniel Ives suggested Twitter, along with Snap Inc (NYSE:SNAP), would benefit at the expense of Facebook, Inc. (NASDAQ:FB). Then, on Thursday, MoffettNathanson’s Michael Nathanson made a point of reiterating the firm’s “Sell” rating on Twitter stock, suggesting shares were overvalued relative to past and projected results.

The mixed messages are nothing new to long-time followers of TWTR stock. In fact, it would be unusual to

not see such mixed messages.

Thing is, with the dust finally settling and the key players in the social networking game finally securing their sliver of the social media space, it’s not crazy to start handicapping these names like regular companies. And as it turns out, Twitter stock isn’t a bad bet.

What They Said

On Wednesday, GBH’s Ives opined “We believe there are a confluence of factors that have catalyzed the growth prospects of both Twitter and Snapchat in the near-term, with some of this momentum clearly happening at the expense of the Facebook platform.”

On Thursday, Nathanson countered with “Snap and Twitter have likely run too much on already stretched multiples. As the market, fresh from all-time highs, recovers from a massive correction, we think the premium placed on owning strong businesses increases, while the risk of owning those with zero valuation support becomes even more pronounced.”

The two points of view aren’t necessarily mutually exclusive. Nathanson’s comments are more about Snap and Twitter stock, while Ives is talking about a paradigm shift in social media preferences.

Still, in a market environment where analyst commentaries often become de facto Rorschach tests — testing the market’s true opinion of a particular stock — the dichotomous ideas simply extend a long-standing debate.

As was noted, though, no war of words lasts forever. Sooner or later, one way or another, the truth becomes undeniable.

Reality, Past and Projected

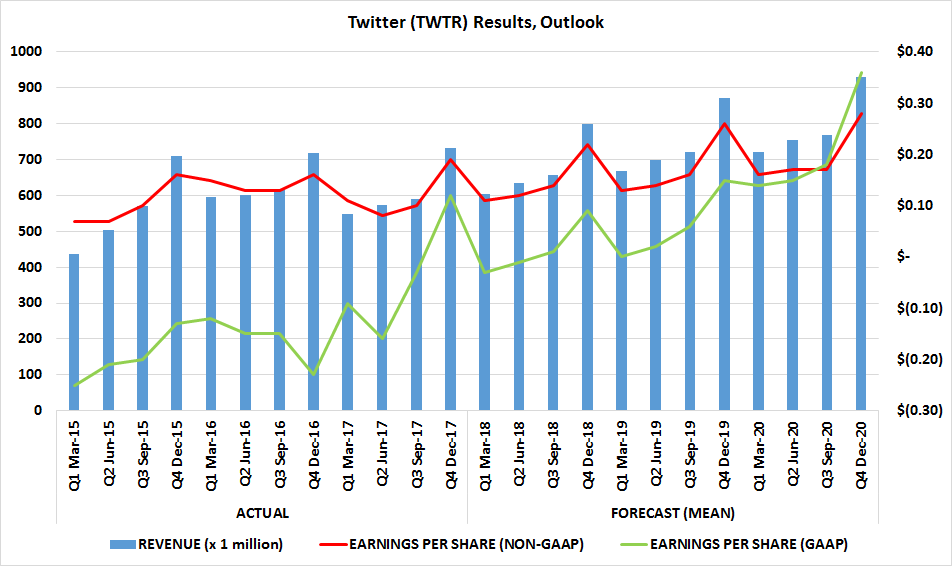

The bit that’s largely been lost in the debate? Twitter has swung to an actual profit, and is expected to widen its profit margins going forward now that it’s figured out a winning formula with users and advertisers.

The graphic below tells the tale. For all of its user-growth problems and the drama that’s perpetually been packaged with TWTR stock, Twitter has become a viable business.

Click to Enlarge

Though the analyst community acknowledges the improvement of the top and bottom lines and is calling for more of the same going forward, in light of last quarter’s pleasant surprise, it’s not a stretch to say the collective outlooks underestimate Twitter’s profit potential.

However, the bigger point is: Don’t let analysts’ observations and opinions distract you from factual information, and don’t confuse a company’s stock with the company itself. The former is a short-term battleground, while the latter is looking for ways to last for the long haul. Nathanson’s comments point to the short-term battleground, while Ives’ take is about the bigger-picture undertow, acknowledging Twitter’s revenue and earnings trends already in place.

Bottom Line for Twitter Stock

This isn’t to suggest you should ignore the inevitable short-term gyrations Twitter stock is almost certain to exhibit going forward. Indeed, you should be using those extreme swings as entry and exit points.

More important though, you have to recognize that, more often than not, you’re only getting a small taste of everything an analyst may be thinking about a particular stock. Indeed, it was only last month Nathanson acknowledged things were getting better for Twitter, when he explained:

“We heard from multiple checks that Twitter’s results are stabilizing as its sales team has tightened its pitch as a brand messaging platform and live TV extension product. In addition, the platform is benefitting from the influx of dollars to social as advertisers are increasingly taking a portfolio approach to social budgets.”

It’s not exactly a resounding bullishness on Twitter stock, but it certainly adds some much-needed perspective on the company’s bearish stance on the current TWTR stock price. The issue is with the stock’s valuation, not the company itself.

Perhaps that’s the long way of saying Twitter is a name to buy on any healthy dip.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.