On Tuesday, Medtronic plc (NYSE:MDT) reported its fiscal 2018 third-quarter results. Earnings were in-line with expectations while revenue grew 1.2% and topped analysts’ expectations. However, the quarterly report wasn’t enough to jolt Medtronic stock higher, with shares falling 2%. Should investors flock to MDT stock or should they look elsewhere?

Medtronic stock is far from a bad pick. In fact, Medtronic is a very good company. MDT stock has a 2.25% dividend yield, makes quality products and trades at a reasonable valuation. But, in my view, there are other, more attractive alternatives out there.

Let’s look at Medtronic stock more specifically, though.

Analysts expect earnings of $4.77 per share this year, which is up about 3.7% from last year. Further, analysts expect sales to fall about 1% this year. It’s worth pointing out that management expects sales to grow 4% to 5% in constant currency terms. They also expect non-GAAP earnings to grow 9% to 10% this year on a constant currency basis.

So, even though on paper it doesn’t look like things are going well for this Dublin-based company, it’s actually not going as bad as it may seem. For the record, analysts expect a better fiscal 2019. They’re forecasting for earnings and sales growth of 8.6% and 3.4%, respectively.

While all of that may be true, the reality is that Medtronic stock trades at about 17 times this year’s earnings and 16 times fiscal 2019 earnings. This valuation isn’t horrendous by any means, but I’m not overwhelmingly attracted to it, given MDT’s growth.

If Not MDT Stock, Then What?

If we’re not buyers of MDT stock, then what do we like instead? We could compare it to stocks like Boston Scientific Corporation (NYSE:BSX) or Abbott Laboratories (NYSE:ABT). But instead, I’d suggest

Johnson & Johnson (NYSE:JNJ). While JNJ stock may not be a direct comparison to MDT stock in the form of an industry-to-industry peer, the two companies do have some overlap. Further, they’re both in the same sector and that makes it a viable comparison in my eyes.

I recently did some research on JNJ stock and found that it was a definite buy. Shares fell 1.7% on Tuesday, giving investors a chance to do just that. I find JNJ attractive on a number of metrics.

J&J vs. Medtronic Stock

Entering the first quarter of fiscal 2018, analysts expect JNJ to grow sales and earnings 6.1% and 11% this year, respectively. Next year, those figures fall to 3.7% and 5.6%, respectively. However, given that JNJ has beat earnings expectations for at least 17 straight quarters, I’m willing to bet that estimates for 2019 may be too low.

JNJ pays a 2.5% dividend yield, which slightly edges the 2.25% yield from MDT stock. Further, J&J has a slightly better valuation based on both 2018 and 2019 earnings (trading at ~16 and 15 times those estimates). I’ll admit, it’s very close. But consider which company has the better margins? Which has the better cash flows?

While MDT tops JNJ on gross margins, as that money makes its way down the line, JNJ does a better job of retaining the most of each dollar. JNJ sports stronger operating and profit margins and its cash flows are better too. JNJ obviously generates larger cash flows because it’s a much larger company. That being said, though, both operating cash flow and free-cash flow are trending higher for JNJ, while the opposite is true for MDT.

For all of these reasons — growth, valuation, dividends, margins and cash flow — I see little reason to buy Medtronic stock over J&J.

One last note to consider? The brand strength. It’s hard to top J&J as one of the world’s leading blue-chip brands.

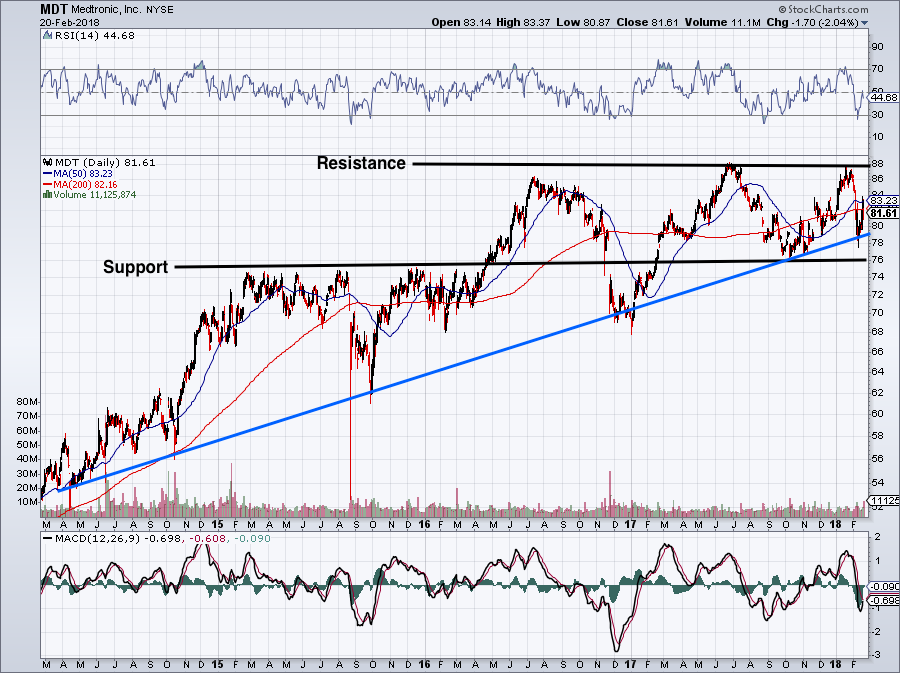

Trading MDT Stock Price

Despite the favoring of JNJ stock over Medtronic, MDT stock price actually has a pretty decent chart. You’ll notice the level of support in the $74 to $76 area, as well as trend-line support (blue line). Resistance rests at $88.

Click to Enlarge

Investors can try buying near these support levels, or on a breakout over resistance.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell held a position in JNJ.