To an investor not looking for any nuanced clues, comments made by Nvidia Corporation (NASDAQ:NVDA) CFO Colette Kress at this week’s technology conference hosted by Goldman Sachs would have been easy to look past. Current and would-be owners of NVDA stock understand that such events are more for the purpose of public relations and less about a tech-centric pow-wow.

This time around, however, Kress made a subtle but repeated point that would have been easy to overlook without a thorough understanding of the company’s revenue mix and how that mix is changing. As it turns out, artificial intelligence and all that goes with it is a huge deal.

Problem is, Nvidia is relying on a relatively unreliable gaming GPU market to carry the company’s fiscal weight until AI is a big enough market in and of itself to do so.

It could be a long and frustrating wait for NVDA stock holders in the meantime.

NVDA Stock Ups and Downs

It’s not exactly a secret that Nvidia is winning the artificial intelligence hardware wars.

Though rival Advanced Micro Devices, Inc. (NASDAQ:AMD) also makes graphics processing cards (which have been surprisingly successful when it comes to the number-crunching needed to make machine learning work) Nvidia saw the advent of AI over a decade ago, and planned appropriately.

The artificial intelligence market’s surface has only been scratched too. International Data Corporation recently opined that by 2025, spending on AI systems would total $57.6 billion. That’s up from 20017’s estimate of $12 billion.

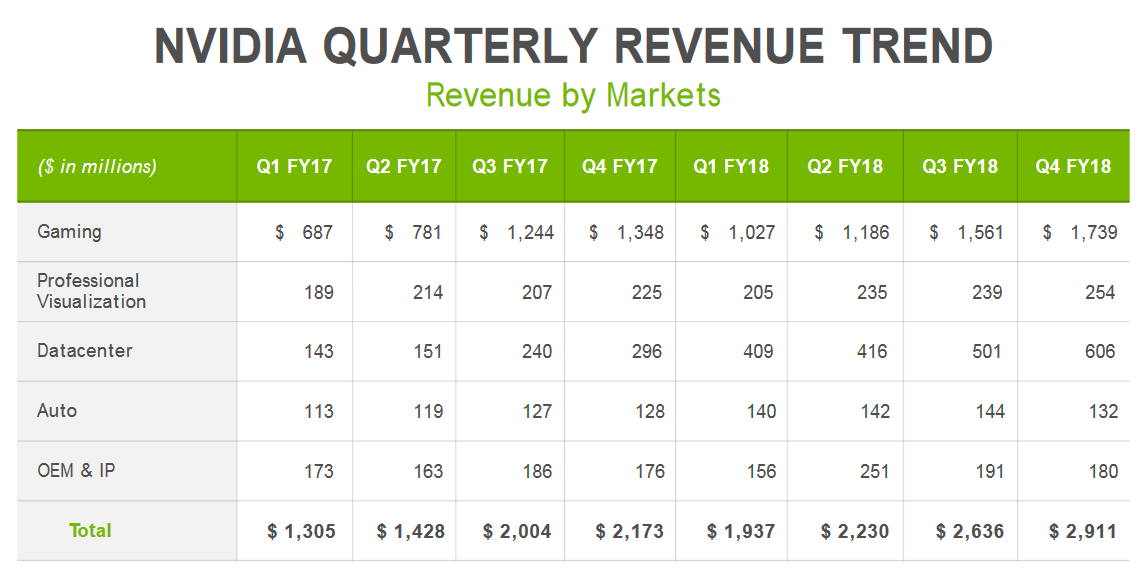

It’s certainly plenty for investors in NVDA stock to look forward to. Indeed, they’ve already gotten a taste. Last quarter’s data center revenue grew a whopping 105% year-over-year, as customers tap into the company’s CUDA-based stack and developer options that facilitate deep-learning.

Problem is, even with that rapid growth, this arm still only accounted for about a fifth of the $2.9 billion Nvidia reported in its fourth fiscal quarter of last year. Gaming made up about 60% of the top line, and this year’s AI spending isn’t likely to be enormously better than last year’s.

Most AI-spending forecasts suggest its growth is weighted towards the back-end of the timeframe in question.

Click to Enlarge

It’s not the end of the world. Nvidia is the market leader on that front despite new GPUs from AMD that were supposed to (and did) turn a few heads. The entry from

Intel Corporation (NASDAQ:INTC) into the discrete GPU market isn’t a viable threat to Nvidia yet either.

There’s also the stunning growth of cryptocurrencies, which are best “mined” and readily managed by graphics cards. Digital currencies aren’t going to go away anytime soon, even if they are poised to lose much of their value.

In both cases though, the supercycle that catapulted each use of GPUs (gaming and cryptocurrencies) are likely to hit a serious headwind sooner than later. The initial rush into cryptocurrency mining has cooled now that flag-bearer Bitcoin has lost half of its value since December’s peak.

And, it’s unlikely any gamer that shelled out a few hundred bucks for a new GPU from Nvidia last year is ready to spend another few hundred bucks on another upgrade so soon.

A slowdown for Nvidia’s biggest and best market will more than offset the continued acceleration of the company’s most promising opportunity, which has yet to reach its full stride.

Bottom Line for NVDA Stock

The irony is, Nvidia didn’t do anything wrong. In fact, it did everything right. It was arguably more ready for the rise of AI than any other player.

It also knew that it would have to keep making gaming GPUs between now and the time when data centers and artificial intelligence could mean more to the bottom line, even if the cryptocurrency tide was a pleasant surprise.

It’s not clear, however, if fans and followers of NVDA stock are really ready for the “in the meantime” lull we’re apt to see over the course of the coming quarters. Priced at 33 times next year’s expected earnings, traders are clearly expecting a lot. Any stumble en route to those results could be interpreted as more troubling than it really is.

Fair? Not in the least. Nvidia is a fine company with a bright future. Investors arguably should make a long-term holding of it.

This isn’t about fair, however. This is about figuring out what the market is going to do with NVDA stock when gaming-based demand for GPUs wanes before demand for its data center products takes off. There’s a risk there wise investors can’t afford to ignore.

Just something to think about.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.