When Cisco Systems, Inc. (NASDAQ:CSCO) reported its fiscal second-quarter earnings results, investors were quick to bid up the stock. Although shares pulled back a bit from that rally in the ensuing days, they are back on the move. Cisco stock hit fresh 52-week highs and its highest level in almost two decades on Feb. 27.

With analysts hiking their price target, many are wondering if there’s still time to get long. On the flip side though, CSCO stock is up 50% from its August low, how much upside could really be left?

According to recent analyst moves, about 11% seems right. Of the last five price target assignments, we have three $50 targets, one $51 target and one $48 target. Investors are getting excited as CEO Chuck Robbins transitions the company toward better growth markets.

Moves into security, software and subscription revenues not only boost growth, but they are good for margins too.

Valuing Cisco Stock

Accelerating top line growth while expanding the bottom line is key to commanding a higher valuation. If CSCO is able to that, its stock price should have no trouble moving higher. Let’s take a closer look at where this stock stands now.

Despite Cisco stock rallying 50% from mid-August, its valuation is actually quite reasonable. The company is halfway through its fiscal 2018 and analysts expect earnings of $2.58 per share this year. That’s up about 8% from fiscal 2017. Next year, they expect 10.5% growth.

On the revenue front, forecasts call for 2.3% growth this year and an acceleration to 2.8% in 2019. Admittedly, these are not huge growth numbers. We have high-single-digit to possibly double-digit earnings growth and low single-digit revenue growth.

However, when you consider that Cisco trades at 17.4 times this year’s earnings and 15.7 times 2019 earnings, it’s not so unattractive; it’s at least not expensive.

Further, Cisco stock pays a 2.6% dividend yield and has a mountain of cash it can deploy. Tax reform will bolster the bottom line, while CSCO is sitting on more than $70 billion in cash and short-term investments.

In other words, while Robbins continues to push the company into better growth channels, he can afford to either buyback a ton of stock or make some noteworthy acquisitions. These acquisitions can help accelerate growth.

Cisco right now reminds me of companies like International Business Machines Corp (NYSE:IBM) (although it’s starting from a better position) Intel Corporation (NASDAQ:INTC

) or Microsoft Corporation (NASDAQ:MSFT).

In other words, a management team looking to transition away from its legacy business into better growth opportunities.

Trading CSCO Stock

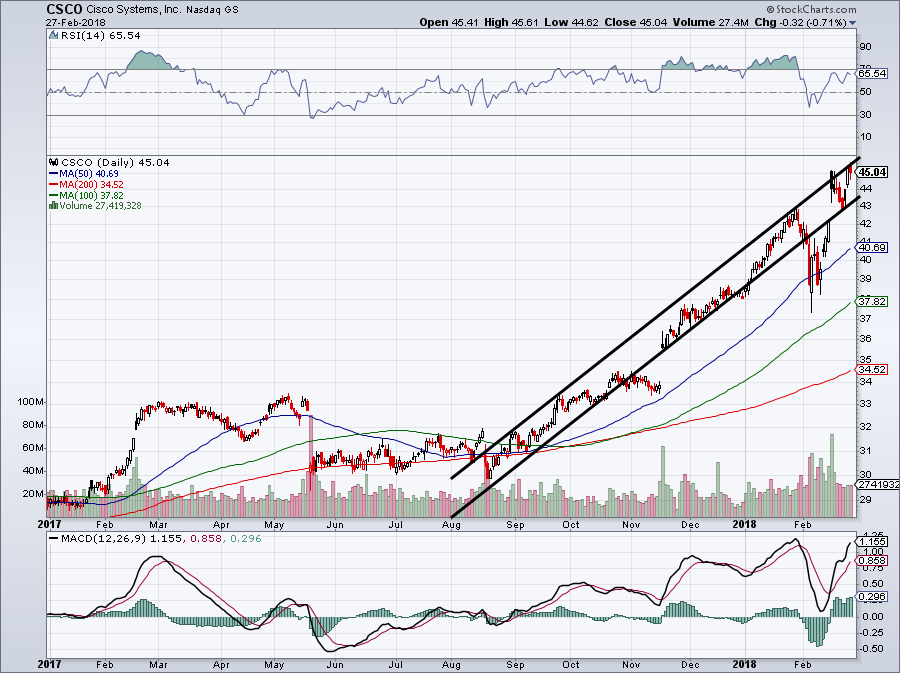

While the company may be executing on its transition plans, Wall Street hasn’t let its progress slip by unnoticed. Back in January, we took a closer look at Cisco stock. Shares were heavily overbought and sitting near $44; $1 per share below current prices. We said investors should wait for a pullback before getting long, preferably buying near $36.50.

The stock ultimately fell to ~$37 before shooting back over $40 just a few days later. Many investors may have missed their chance, as the market was under severe, albeit temporary, selling pressure.

Click to Enlarge

The average analyst price target now stands at $49, up about 9% from current levels. Frankly, it leaves us in a tough spot.

Fundamentally, Cisco is doing great. It’s finally making the turn with faster-growing businesses and its cash flow is monumental. Heck, just last quarter it churned out operating cash flow of $4.1 billion, a second-quarter record. Margins are expanding too.

All of this leads me to believe CSCO is heading higher. Cisco stock hasn’t given us many chances to buy though. Perhaps on a pullback to $43, bullish investors could consider a starter position and then add to that position near $40 or $41. A pullback into the 50-day or 100-day moving average should also be good buying opportunities.

The truth is, if you missed Cisco it’s hard to chase right now. The buying levels aren’t set up yet, so it’s hard to say where to start buying. As a trade, Cisco stock is a coin toss. As an investment though, investors should consider nibbling, adding on declines and riding Cisco higher.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell held no position in any of the aforementioned securities.