TJX Companies Inc (NYSE:TJX) reported earnings on Tuesday morning, missing analysts’ estimates for the bottom line. However, top-line results came in ahead of expectations and investors generally viewed the report as good. That’s giving a boost to TJX stock.

The Quarter for TJX Stock

Earnings per share of 96 cents came up six cents per share short of expectations. However, revenue of $8.7 billion grew almost 12% year-over-year and came in more than $200 million ahead of analysts’ estimates.

Not included in the headline number was TXJ’s $1.13 in earnings per share, which includes a 17 cent per share gain from the Tax Cuts and Jobs Act. There’s more good news though. Comparable-store sales results came in at 3% for the first quarter of fiscal 2019. Estimates were only calling for comp-store sales of 2.5%.

Further, TJX increased its quarterly dividend by 25% to 39 cents per share. That gives TJX stock a yield of 1.8% and marks the 22nd consecutive year of dividend increases for the retailer. Finally, management increased its full-year earnings guidance.

Valuing TJX Stock

It’s worth noting that management tends to be somewhat conservative.

That’s usually good for investors, as the company under-promises and over-delivers. However, it’s also worth noting that guidance for next quarter and the full year came in below expectations. Given how good the company’s first-quarter report was, that’s likely the only thing keeping a lid on the reluctantly rising TJX stock at this point.

Management expects full-year earnings to come in between $4.75 and $4.83, or about $4.80 at the midpoint point. Analysts’ current expectations stand at $4.85 per share. At the midpoint of management’s guidance, this would represent year-over-year growth of 19%. Management is also looking for comp-store sales of 1% to 2% for next quarter and the full year. That’s even after the 3% comp they did in the first quarter and the better-than-expected gross margins.

Like I said, conservative.

In any regard, we’re paying a little under 17 times forward earnings for TJX stock. While that may not be a screaming bargain, it’s definitely not a big overcharge for what investors are getting — especially considering the near-20% earnings growth this year and double-digit earnings growth next year to go along with mid-single-digit sales growth each year as well.

Positive comp-store sales growth (which will likely come in ahead of management’s 1% to 2% outlook) along with a 1.8% dividend only adds to the bullish story.

Trading TJX Earnings

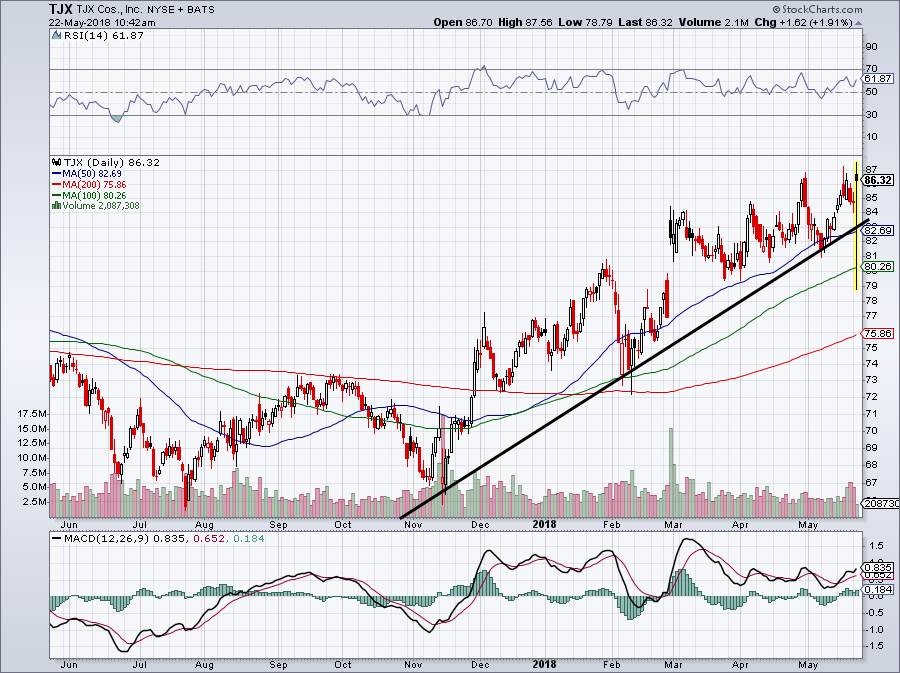

Click to Enlarge

Following TJX earnings, shares hit new 52-week highs in the pre-market trading session, before getting off to a slow start in Tuesday’s regular-hours trading session. However, shares eventually made new highs in the session.

It’s important to note that the chart above includes the immediate knee-jerk reaction in the pre-market trading session. It also includes the new 52-week high set in the pre-market, although that level was eclipsed a few hours into the sessions. Given the results, I expect TJX stock to churn out more new highs.

If TJX stock fails to push to new highs, look for support to come into play around $84. Management’s outlook could have been stronger, but make no mistake, TJX Company is one of the better retailers out there at the moment. I would put it up there with Home Depot Inc (NYSE:HD) and Costco Wholesale Corporation (NASDAQ:COST).

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.