More so than many other companies, Walmart Inc (NYSE:WMT) needs to show up for its upcoming earnings report. After a standout performance in 2017 when WMT shares returned an impressive 46%, sentiment was high going into this year. Up until the end of the first month, the big-box retailer didn’t disappoint. Now, everything hinges on the Walmart earnings report.

I’m only somewhat hyperbolic in my last sentence. Sure, no one news event will make or break an entire organization, certainly not one the size of WMT. But on the other hand, Walmart stock dropped 14% on a year-to-date basis. Against this year’s all-time closing high, shares have slipped 22%. For most people’s definition, that would classify as correction territory.

Moreover, WMT is charting a series of lower highs and lower lows. It dropping below this established trend channel in recent days obviously doesn’t provide investors confidence. Thus, the faithful bulls are nervously eyeing the Walmart earnings report.

Management must say something, anything, to stop the bleeding in Walmart stock.

Of course, this is easier said than done. The biggest challenge was apparent early this year. In an effort to compete against Amazon.com, Inc. (NASDAQ:AMZN), WMT rolled out its own e-commerce business. However, a massive spike in electronics sales hampered deliveries of everyday goods last holiday season. As a result, the big-box retailer lost significant ground.

Heading into the Walmart earnings report this Thursday, all eyes are still on the company’s e-commerce venture. Unfortunately, the specter of Amazon looms. The e-commerce giant is aggressively targeting government-aid recipients through discounted Prime memberships. That being the case, Wall Street may consider WMT’s guidance for the year overly optimistic.

Substantive results would go a long way, but can WMT deliver?

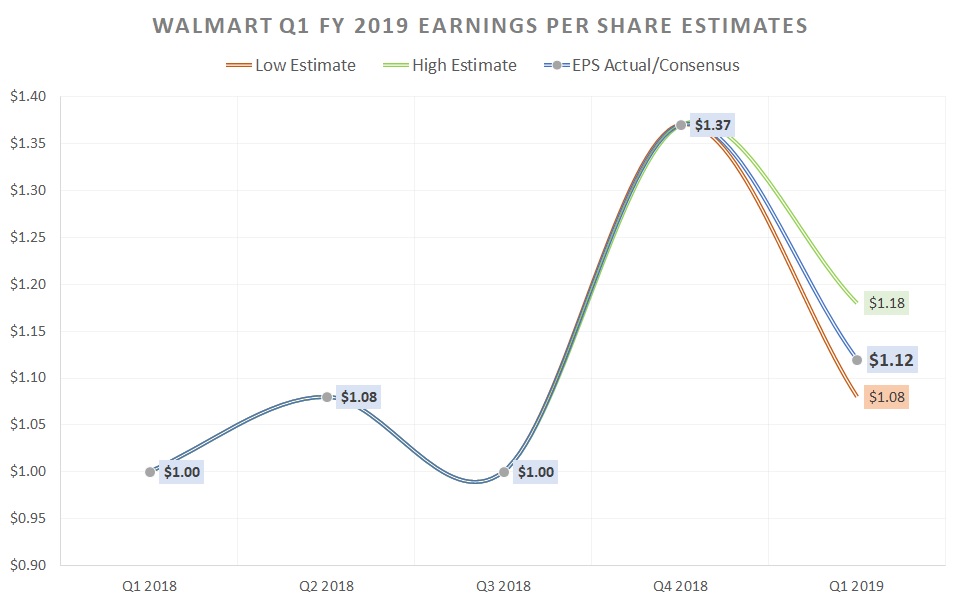

A Critical Showdown for the Walmart earnings report

Click to Enlarge

In the year-ago quarter, consensus estimates anticipated a 96-cent EPS, while actuals came in at $1. Should Walmart stock hit its target this time around, this would represent 12% year-over-year growth.

However, a historical challenge is that in recent years, Q1 Walmart earnings performance lacks decisiveness. For both fiscal 2015 and 2016, the company missed the initial quarter. Given significant question marks heading into the upcoming report, I’m not particularly bullish on Walmart’s chances.

On the

revenue side, analysts target $120.5 billion. The estimate spectrum ranges from $119 billion to $121.7 billion. In the year-ago quarter, the big-box retailer raked in $117.5 billion.

As mentioned previously, Wall Street will keenly note whether the company has made headway against Amazon. That’s going to be a massive undertaking and not just because the e-commerce innovator has so many Prime members.

In my recent write-up for Amazon, I mentioned that Prime active users cover the entire income spectrum. Like you would expect, the affluent love their membership privileges. But a significant percentage of middle to lower-income consumers also wear the green jacket, so to speak. That tells me that Amazon directly engages their customers in ways that WMT does not.

Not to pour salt on festering wounds, but big-box rival Target Corporation (NYSE:TGT) is performing well this year, up 11%. Certainly, a risk exists that if Walmart earnings fall short, the resultant selloff could be more severe than usual.

What to Do With Walmart stock?

Again, I’m not very bullish on Walmart hitting its EPS target given the resistance it faces. But what about Walmart stock? Here, I have a more nuanced approach.

If the company fails to bring home the bacon, and if Wall Street punishes WMT shares, I’m interested. Primarily, my logic is that Walmart is too much of an industry stalwart to continue falling. At some point, I think management will get its stuff together.

The other reason is that fundamentally, the company is doing exactly what it must. Revenue growth isn’t sexy, but it exists. E-commerce had some hiccups, but I appreciate management’s hunger and drive to try something different.

Most importantly, WMT isn’t a bloated entity. For instance, in the past three years, it has steadily improved its inventory turnover rate while keeping on-hand levels reasonable.

In the nearer-term, I wouldn’t bet the house ahead of the Walmart earnings report. But should the retailing giant slip-up, it’s an opportunity to turn lemons into lemonade.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.