One of the most often used arguments in favor of owning Johnson & Johnson (NYSE:JNJ) is its diversity. JNJ stock isn’t just an investment in some of the pharmaceutical industry’s most critical drugs. It’s also an investment in some of the market’s most basic off-the-shelf personal care goods as well as a stake in a medical equipment business most investors simply forget about.

Diversification in and of itself doesn’t inherently make a company worth buying into, however. It’s still entirely possible all of a company’s revenue streams could be running into a headwind.

That certainly seems to be the case for Johnson & Johnson, with no real end in sight.

Shampoo and Headaches Aren’t a Huge Deal

Credit has to be given where it’s due; J&J has maintained its stature as one of the most recognizable names (if not the most recognizable name) in the healthcare arena.

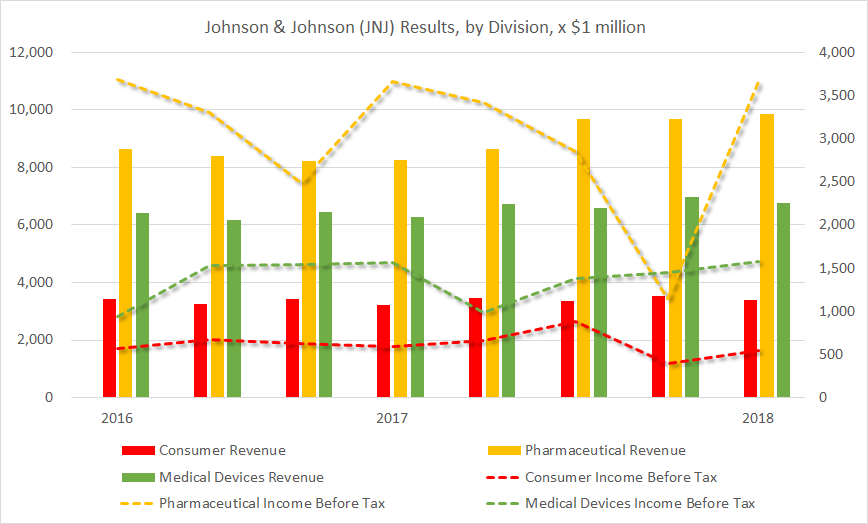

Its namesake baby shampoos are only the beginning. It’s also the parent company of Band-Aid, Tylenol, Aveeno, Zyrtec and more. Those consumer-oriented names are the smallest piece of its revenue pie though. The biggest? Prescription pharmaceuticals.

The graphic below tells the tale. Practically half of the company’s revenue is driven by prescription drugs. And, decidedly more than half of its income comes from pharmaceutical sales.

Click to Enlarge

Point being, if Johnson & Johnson is going to remain a powerhouse, and if JNJ stock is going to rebound as a blue chip worth owning, prescription drug sales are going to have to be a big part of that equation.

Those who know the J&J story well though, and those who are familiar with its pipeline, will also know the drug pipeline has proven tricky to handicap.

Nickels and Dimes Add Up

The company’s first quarter pharmaceutical sales were up 19% year-over-year. But, it’s difficult to point to one single drug, or even franchise, and say that it carried the bulk of Q1’s weight.

Darzalex saw the best year-over-year growth pace, sporting a 69% improvement. It only drove $432 million worth of sales though. The company sold $1.4 billion worth of Remicade, but that was lower to the tune of 17% mostly thanks to the loss of patent protection

So how has the company managed to reignite a pharmaceutical business that had been struggling for a little too long? One approval at a time. It works, but it’s hardly an overwhelming kind of success that most pharma companies need.

Still in Need of a “Killer App”

To borrow a phrase from the world of technology, Johnson & Johnson needs a killer app; a drug, like a red-hot program or application, that becomes a must-have on the pharmaceutical landscape.

It doesn’t have a big one right now. It’s got a bunch of respectable, but not game-changing, franchises. That is to say, it’s got quantity, but not a great deal of quality.

It’s got almost 20 different drugs driving revenue, but only two drugs are generating more than a billion dollars’ worth of revenue per quarter. One only has to look at its current late-stage pipeline to understand this might not dramatically change anytime soon without more sweeping measures.

The bulk of the company’s current trials are tests of Xarelto, Invokana, Darzalex and Imbruvica for use in slightly different scenarios than the ones they’re currently approved to treat.

Widening the usage of these therapies always helps drive incremental revenue. Make no mistake, rivals like Pfizer (NYSE:

PFE) and Merck (NYSE:MRK) do the exact same thing. Those rivals, however, are also arguably more aggressive than J&J has been of late when it comes to taking proverbial moonshots like Merck’s Keytruda.

That may be about to change, however.

Quietly Thinking About Deals

You have to read between the lines just a bit to understand what was really being said, but following the April release of its Q1 numbers, Johnson & Johnson said it could spend up to 15% more than it has been on R&D and capital investments, thanks to recent tax cuts.

That’s not exactly a commitment to the establishment of a deeper, better pipeline. It’s just an acknowledgement of the opportunity. Still, the company did make a point of saying it.

That hint was underscored in early June when CFO Dominic Caruso explained during an investor conference that J&J was “capable of doing 10 $5 billion transactions. We don’t have to do a $50 billion transaction.”

It’s a level of detail that implies the company’s been thinking about it, and mulling what an investment, or investments, in its future might look like.

It’s a start.

Bottom Line for JNJ Stock

None of this is to suggest JNJ stock is un-ownable here. Indeed, following the stock’s 15% pullback from January’s high, the value-oriented argument kicks back in. Even a ho-hum Johnson & Johnson can be appreciated while its dividend yield is just under 3.0%.

Appreciation for playing it safe only goes so far though. Sooner than later, the company is going to have to take a shot on something big.

It could be in the cards, given recent comments from the company’s chiefs. If it doesn’t happen in the foreseeable future though, and all the best R&D prospects get snatched up by rivals, it’s going to be awfully tough to choose JNJ stock over shares of its more forward-minded rivals.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.