For the record, investment bank JPMorgan has been bullish on casino names MGM Resorts (NYSE:MGM), Las Vegas Sands (NYSE:LVS) and Wynn Resorts (NASDAQ:WYNN) for a while, making MGM stock worth another look at least.

In March it recommended buying Wynn following founder Steve Wynn’s sizeable sale of his stake. And, though it view LVS as an overly expensive name, it acknowledges the company’s health.

JPMorgan seems to have something of a particularly soft spot in its heart for MGM Resorts, however, reiterating its “Overweight” rating on MGM stock earlier this week, saying things will get better for the casino operator during the latter half of 2018.

And the firm may well be right.

Tough Start Sets Up Strong Finish

The first half of the year wasn’t an easy one for casino investors. WYNN shares were all over the map (though mostly up, until June) in the wake of a scandal that ultimately ousted the founding CEO.

Meanwhile, LVS stock recently saw its year-to-date gains squashed on worries that Macau’s gambling revenue growth was slowing.

MGM Resorts, though, has had the toughest time of all this year. It was down 15% over the course of the first six months of 2018.

It could have gotten worse too, had JPMorgan not stepped in.

Although MGM stock was in rebound mode coming out of June’s drubbing, there was little guarantee the bulls would continue plowing in. The volume behind the early July advance was light, and the industry’s future still uncertain.

JPMorgan changed everything on Wednesday though, not with an upgrade (there is no higher rating than “Overweight,”) but with a simple explanation of why the foreseeable future wasn’t likely to look like the recent past.

The Word on MGM Stock

Analyst Joseph Greff made the call, explaining “We believe most of the issues that have caused 2018’s underperformance are transitory, and the picture is bright(er) heading into 2019,” adding that the current expectations of the company are “reasonably/incredibly low.”

And just to make sure there was no misunderstanding, he plainly said, “We would be buyers of MGM heading into the back half of 2018, and see the stock offering an attractive risk/reward and setup for 2019.”

Thing is, JPMorgan’s Greff isn’t alone in his optimism regarding MGM Resorts.

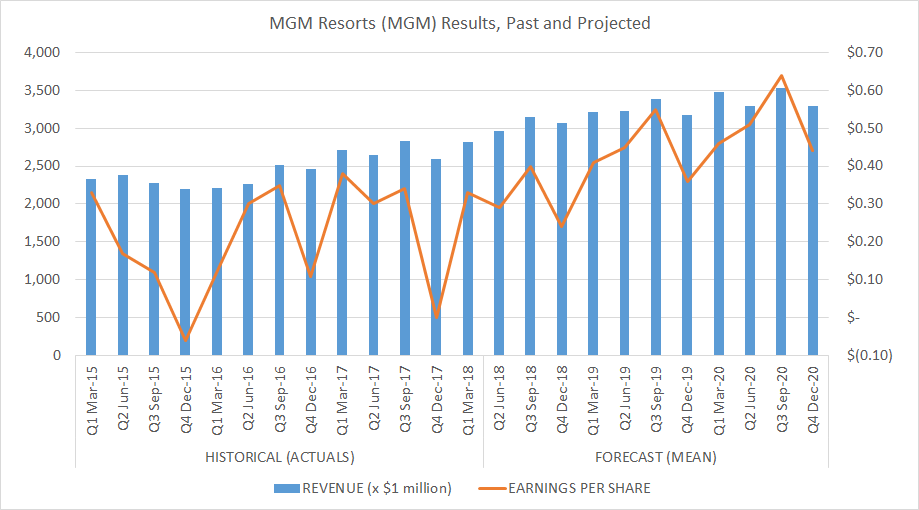

The graphic below tells the tale, plotting the company’s past and projected revenue, and past and projected per-share profits. Both have been, and continue to, rise.

Click to Enlarge

By the way, this same analyst community that’s calling for more growth mostly rates MGM stock as a “Strong buy,” and sports an average price target of a little more than $38 per share. That’s more than 25% above the stock’s current value.

Can analysts collectively be wrong? Sure. Anything’s possible. By and large though, the professional stock-picker crowd is usually on target. The company may not be making top-line and bottom-line progress in a perfect straight line. But, it has been and continues to make progress, in step with global economic growth.

But Macau’s headwind? And what about the impact of an ever-strengthening trade war?

Sure, those are concerns, but there are always concerns. Capitalism tends to find a way around them. Even then, Macau’s “slowing” growth was still a solid 12.5% in June.

And as far as the trade war is concerned, stocks have been climbing that wall of worry since March’s lows. The S&P 500 is at multi-week highs right now, and the trade war hasn’t been any more real, nor any bigger, than it is right now.

Bottom Line for MGM Stock

The “reasonably/incredibly low” expectations Greff says the market has of MGM stock, by the way, are manifested in its valuation. Shares are trading at a trailing P/E of 8.9 and a forward-looking P/E of 17.3, lower than the market’s overall average. There’s room for the kind of price appreciation the analyst is calling for, even if he did lower his price target from $41 to $37.

Whatever the details of the case, the bigger-picture point is well made, and was already well-positioned for underscoring. Investors unnecessarily saw the glass as half-empty, coming to dire conclusions that were anything but justified. Now comes the swing of that pendulum from the other direction.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can follow him on Twitter, at @jbrumley.