When Gilead Sciences (NASDAQ:GILD) reported earnings earlier this month, shares stagnated a bit but stayed above the 50-day moving average. That gave investors a reasonable level to measure against. However, Gilead stock is lower on Tuesday following disappointing drug data.

Specifically, Gilead’s selonsertib drug failed its phase 3 clinical trial. Even though GILD stock is off the lows, that’s causing selling pressure on Tuesday and brings up a more broad question: Which stock is better, Gilead or Celgene (NASDAQ:CELG)?

I believe the latter offers a better value right now, despite the fact that Bristol-Myers Squibb (NYSE:BMY) has already announced that it will buy Celgene

. Let’s look at both stocks more closely.

Sizing Up Gilead Stock

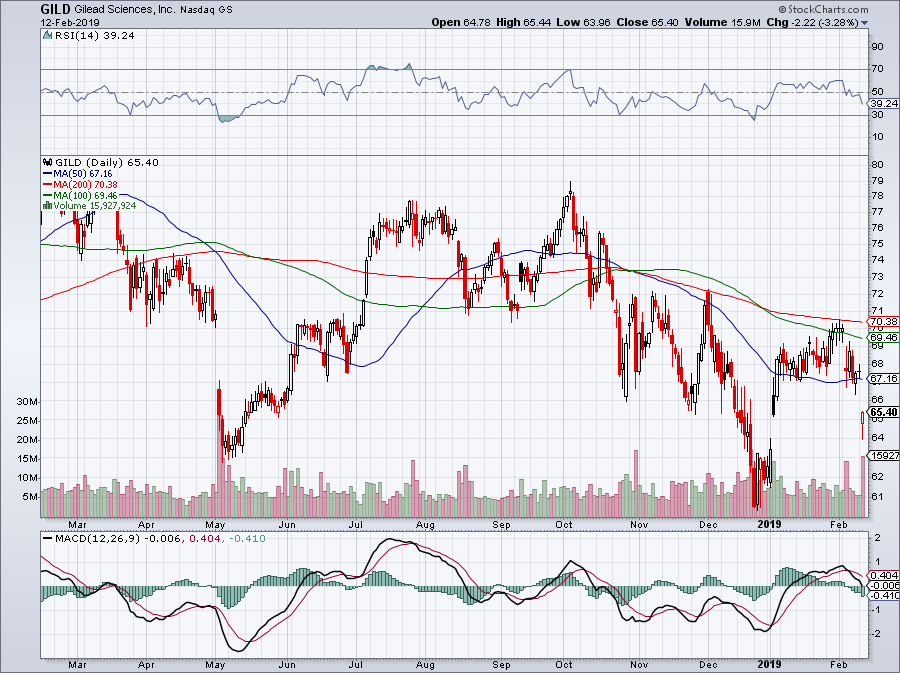

Click to Enlarge

When Gilead reported fourth-quarter earnings, it missed analysts’ earnings expectations of $1.69 per share by 25 cents and reported a 2.5% decline in sales. For 2019, analysts are currently forecasting a 30 basis point decline in sales, following a more than 15% decline in 2018. Further, they expect roughly flat earnings growth from last year’s non-GAAP earnings of $6.67 per share.

That’s not all that great, but considering the stock trades at roughly 10 times this year earnings, at least aren’t paying an egregious valuation. Further, at least the year-over-year declines are abating, unlike 2018’s haircut.

In other words, while Gilead doesn’t have an attractive growth profile, it’s likely put the worst behind it and is looking at moving forward. Plus, the stock yields about 3.75%, not bad in most investors’ eyes. The company has $31.5 billion in cash and roughly the same amount in long-term debt. Finally, while Gilead stock still kicks off a solid amount of free-cash flow, it’s been under notable pressure over the past few years.

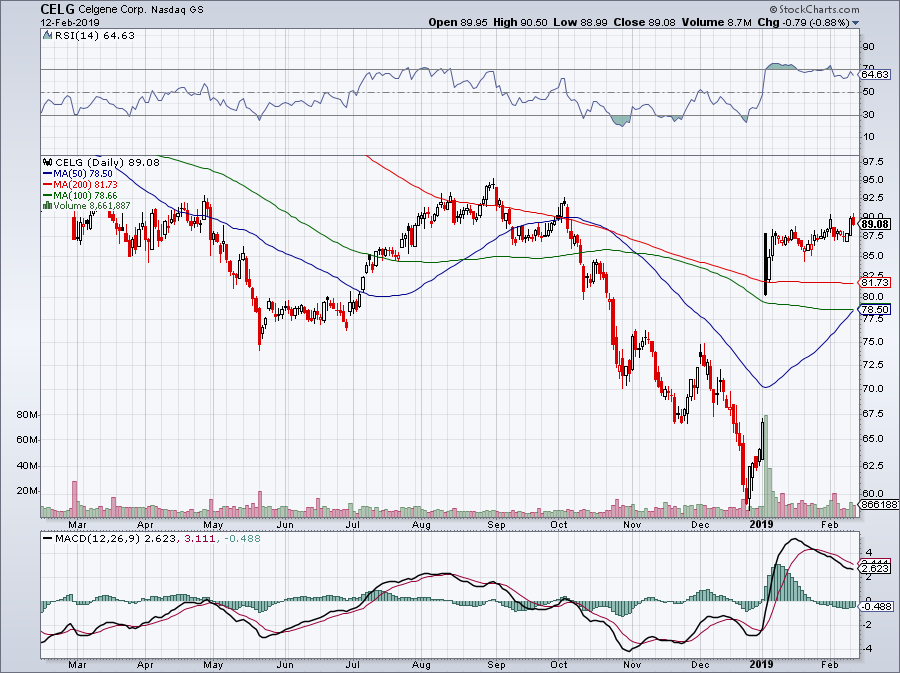

Click to Enlarge

To be fair, it’s not a simple argument that Gilead stock is trash and Celgene is great. In fact, Celgene has its own issues too, but it helps that BMY is there with a bid. It also helps that Celgene has growth.

Analysts expect Celgene to grow sales 11.7% this year and 12.8% in 2020. On the earnings front, consensus expectations call for 18.7% growth in both years. That’s pretty impressive when you think it, particularly when you consider that CELG stock trades at 8.5 times this year’s earnings estimate.

While Celgene may not pay a dividend like Gilead stock, shares are cheaper and have far better growth. Free cash flow is trending higher (not lower) as well. Now for the buyout.

Bristol-Myers will pay $50 per share in cash, plus give one share of BMY for each share of CELG. At current prices, that values CELG at about $100 per share. Celgene also receives a $2 billion breakup fee if the deal falls through and shareholders could receive an additional $9 per share should three of Celgene’s treatments achieve various milestones.

Assuming the deal goes through, let’s also not forget that converting to BMY stock wouldn’t be the worst thing the world. Either way, with CELG still trading at a discount to the takeover price, investors are getting a good deal. The big downside is if the deal doesn’t go through. That’s a risk that doesn’t come with Gilead stock and should that happen, CELG shares will likely plunge in response.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long CELG.