Credit has to be given where it’s due. Advanced Micro Devices (NASDAQ:AMD) stock has made the comeback CEO Lisa Su promised when she took over the reins in 2014. AMD stock has been a champ too, up nearly 1,500% since its early 2016 low as Su’s plans became reality.

The financial metrics further confirm the bullishness. AMD is profitable again. Last year’s top line of $6.5 billion is remarkably better than 2015’s revenue of $4 billion.

The turnaround — perhaps more of a rekindling — may prove to be the easy part of Su’s time at the helm, however. Now past the shell-shock of seeing their upstart rival become a threat again, Nvidia (NASDAQ:NVDA) and Intel (NASDAQ:INTC) have regrouped.

That’s a problem for current and would-be owners of AMD stock too. The market is pricing in a sales and earnings rebound later this year that may not take shape as expected.

No More Low-Hanging Fruit

The short version of a long story: Advanced Micro Devices got sloppy. Its string of developments that aimed to chip away at rivals’ market share ended up misfiring. Between early 2010 and late 2012, AMD stock had fallen from a price of above $10 to less than $2, reflecting waning fiscal results. Nvidia and Intel, meanwhile, came up with the right GPUs and CPUs, respectively, at the right time.

Matters have been different since 2016, when AMD’s Ryzen CPU was launched, followed by its Vega GPUs. Almost as good as its competitors’ wares in terms of performance, but at a much friendlier price, Advanced Micro Devices restored its stature as a serious player.

The next couple of years may not be as compelling as the last couple have been, though.

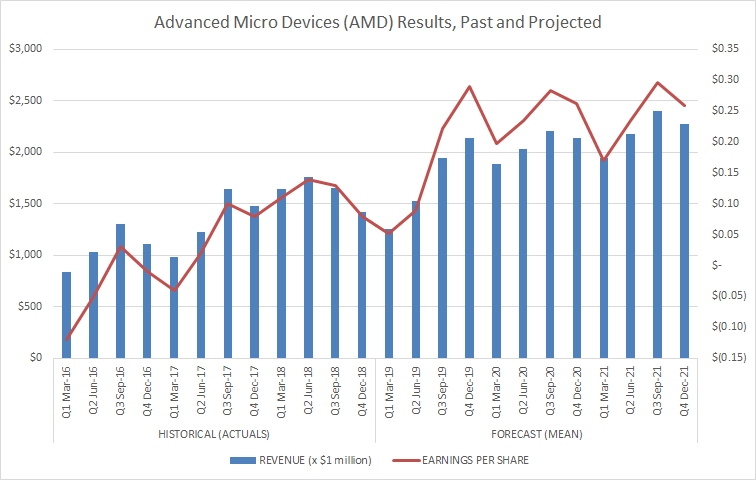

It’s difficult to pinpoint the exact cause as more than one may exist. Whatever the case, the earnings report AMD is slated to post next week is expected to log a third consecutive sequential decline in sales as well as earnings. Analysts project revenue to slide almost 24%, from $1.65 billion to $1.26 billion. Additionally, they expect profits to shrink from 11 cents to 5 cents per share of AMD stock.

Click to Enlarge

An implosion of the cryptocurrency market is a contributing factor. The upgrade cycle is also in a slow patch now. Many corporate and retail consumers shelled out cash a year ago to take advantage of some technological advances.

However, analysts don’t expect that lull to last much longer. Given the way shares are rallying now, investors appear to believe them.

There’s the rub.

High Hopes for Advanced Micro Devices

Admittedly, Advanced Micro Devices has some cool tech lined for a latter-2019 launch. Namely, new 7-nanometer chips are on the way. Its “Rome” server CPUs will begin shipping in the middle of this year, while its third-gen Ryzen processors built on Zen 2 architecture should become available later this year.

But it remains to be seen just how much pent-up demand is actually waiting for these and other new technologies. Up until the final quarter of 2018, data center spending has remained robust over the past couple of years. Consequently, for the majority of buyers, Intel was the choice provider. Furthermore, enterprises may not be ready for a wave of upgrades or additional capacity just yet. Certainly, they don’t want to switch to an altogether new architecture.

To that end, Gartner forecasted in November that spending on data centers would only grow 1.6% in 2019.

If Advanced Micro Devices is going to meet expectations for the second half of the year, it must win far more than its fair share of that tepid growth. That can only be driven by an AMD-specific feature of its server processors that no enterprise-level buyer has yet to publicly identify.

As for consumers, sales of new PCs perked up again late last year, sparking some fresh demand for GPUs.

The first quarter’s PC sales, however, renewed the years-long downtrend, reaching a multi-year low tally of 58.5 million units. Consumers have arguably upgraded their machines as much as they’re going to for a while. This is particularly true in the absence of a new operating system from Microsoft (NASDAQ:MSFT).

Bottom Line for AMD Stock

It’s not a call for the demise of AMD, though some die-hard fans will certainly interpret it as such. Rather, it’s simply a caution that the bar is set pretty high for the second half of the year. Nobody is fully fleshing out the actual demand picture that will drive 6% sales growth for 2019. Plus, the ramp-up in AMD’s revenue by nearly 21% next year when Intel finally brings its next-gen CPUs to the market seems a tad unrealistic.

Click to Enlarge

Even “only” growing at half of its expected pace would still be solid results, to be clear. But with AMD stock already priced at 29.5 times next year’s expected earnings, anything less than meeting those targets could easily upend this overheated rally.

Bottom line: Caution — even more caution than usual — is advised. Advanced Micro Devices isn’t a story stock any longer. It’s graduated to a “show me” state. More critically, it may not be showing the market enough in the very foreseeable future.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can learn more about James at his site, jamesbrumley.com, or follow him on Twitter, at @jbrumley.