Many analysts and journalists routinely talk about the CBOE Volatility Index (INDEXCBOE:VIX), but few seem to have any idea of just what exactly it is that they are talking about. The VIX seems to be everybody’s favorite indicator. I am not exactly sure why. Maybe they think it makes them sound smart when they discuss it.

Let’s clear a few things up.

First of all, the VIX is most often cited as measuring the volatility of the market. But this is wrong! The VIX is actually a measure of implied volatility … it does not measure the actual volatility. So just what exactly is implied volatility? It is an estimate of what the market expects the volatility to be. And as we all know, expectations and reality are often quite different.

The implied volatility number is derived from the Black-Scholes formula. Black-Scholes is used to determine the correct price of an option, as opposed to the price that the option is trading at.

The formula suggests that the price of an option is basically a function of five parameters. These are the difference between the price of the underlying security and the strike price of the option, the price of the option, the time to expiration, interest rates and the volatility of the underlying security.

We know what the first four are so the unknown fifth parameter — the volatility — can be calculated.

The VIX index measures the implied volatility of the

S&P 500 Index and it is derived from S&P options. Roughly speaking, it shows what the market thinks the annualized volatility will be in percentage terms. For example, if the VIX is at 25, it means that the market expects 25% annualized change over the next 30 days.

Second, this is the key to the whole VIX issue. When markets become volatile, options will become more valuable. When the market sells off, traders are willing to pay higher premiums to enter positions. In this case, they are willing to pay higher prices for put options because they believe the market will continue to head lower. These puts provide protection because if the market goes lower the price of the puts will rise. That’s why when the market sells off dramatically the VIX index soars. That’s why this index is referred to as the “fear index.”

But this is yet another misunderstanding!

Think about this. If the market was in a bubble and traders were euphoric and afraid that they are going to miss a big move upward, they would also be willing to pay higher premiums to enter bullish positions. This would cause the VIX Index to soar. I suppose that at this point it would probably be incorrectly referred to as the “hope index.”

There are many misunderstood aspects of technical analysis, and the VIX is certainly one of them. In my view, analysis of this indicator in order to predict future market movements is a useless waste of time. What it shows is a current snapshot of the market. It is essentially like trying to predict who is going to win a race by standing at the finish line and seeing who crosses first. It may have some value as a trading or hedging tool, but indicators need to be predictive and this one isn’t.

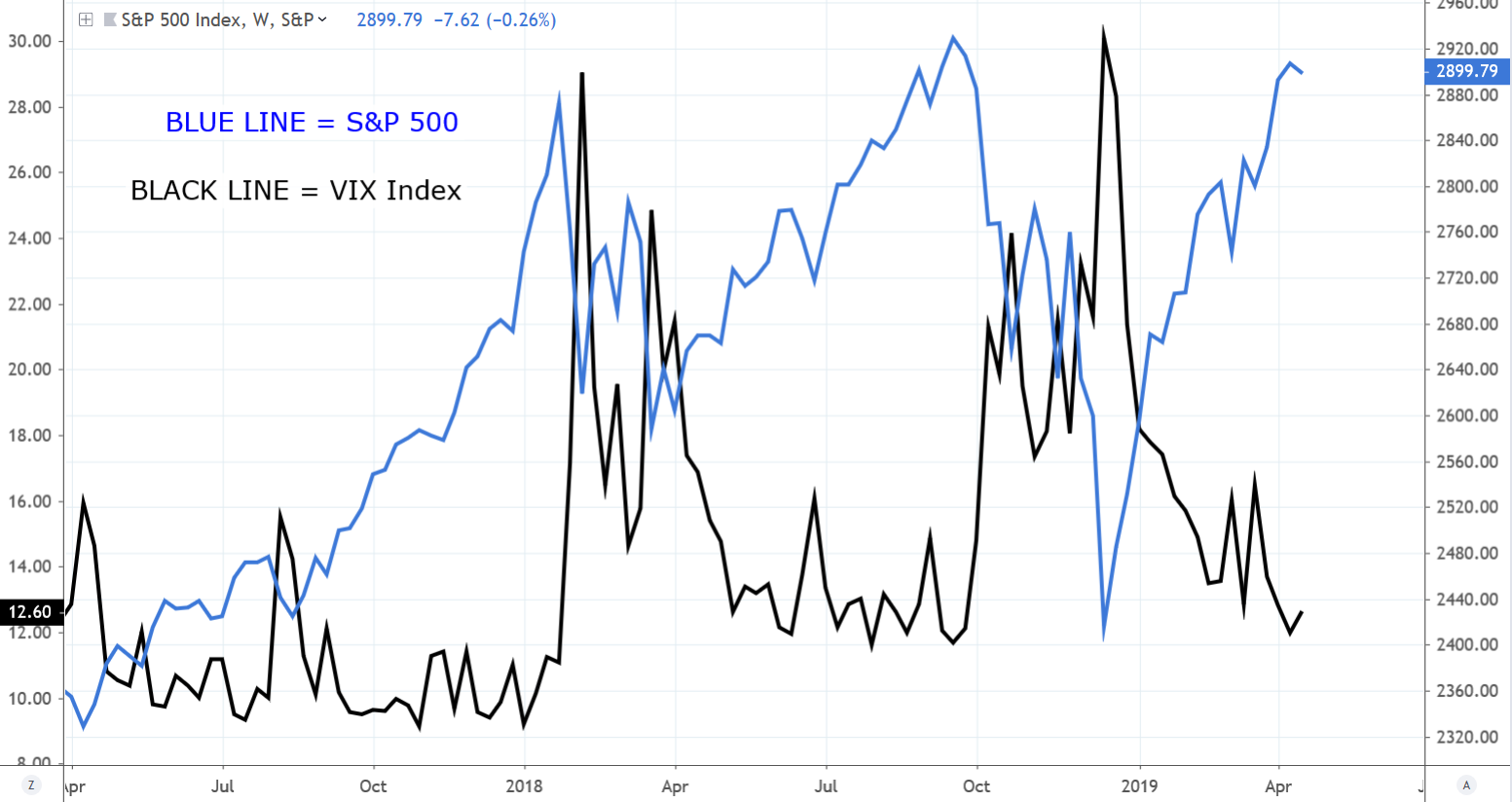

This chart shows the S&P 500 and the VIX index over the past two years. Can you see if following the VIX is in any way predictive? If so, write a blog and I will subscribe to it, because even with the benefit of hindsight I can’t. It is clear that the VIX Index peaks at the exact same time that the market bottoms, so it is a coincidental indicator, not a predictive one.

As of this writing, Mark Putrino did not hold any securities that derive their value from the VIX index.