With a $1.6 billion market cap, Aphria (NYSE:APHA) does not get the type of coverage that many cannabis stocks get. But just because a company isn’t the largest doesn’t mean it should be discarded. Is this the case for Aphria stock?

It could be, but with such a young industry at hand, there are numerous risks. As a result, many investors feel more comfortable in some of the more well-known names.

You know, stocks like Canopy Growth (NYSE:CGC) or Aurora Cannabis (NYSE:ACB). Cronos Group (NASDAQ:CRON) and New Age Beverages (NASDAQ:

NBEV).

Some of these companies, CGC in this case, sport market caps in excess of $15 billion. Others, like NBEV, have garnered attention among retail investors despite having a market cap of just $400 million.

Multi-billion dollar investments along with collaborations and discussions with prominent and well-known companies have helped these names rise to the top of the cannabis industry.

Will Aphria stock do the same?

A Closer Look at Aphria Stock

Last month, Aphria missed on earnings and revenue expectations. However, revenue of $55 million grew more than 570% year-over-year. For a $1.5 billion company in this space, that’s pretty good, especially considering its growth rate.

Of the all the stocks above — CGC, ACB, NBEV, CRON — and including Tilray (NASDAQ:TLRY), Aphria stock had the third highest revenue figure for the quarter. Its growth rate exceeded its peers too.

These companies aren’t known for profitability, but for APHA stock, it was a rarity it held over many of its peers. That is, until last quarter where it reported a net loss of roughly $50 million. Granted it came with a non-cash impairment charge and there were some supply issues in the quarter as well. But still, this caught a number of investors off-guard, as estimates were looking for a loss of 4 cents per share in the quarter, not 16 cents per share.

Later in April, Aphria completed a $300 million convertible debt investment round. This gave a boost to the company’s liquidity and should fuel future growth.

Speaking of the balance sheet, the move was likely necessary for Aphria to keep up with its peers. Cash had fallen 60% from $273 million at the end of fiscal Q1 in August to $107.50 million at the end of fiscal Q3 in February.

Not that all of that cash was going to waste necessarily — total assets increased from $1.625 billion to $2.05 billion in the same span — but it did create a pinch in liquidity. That’s underscored by Aphria’s current assets falling more than 26% from $418 million to just $308.5 million in six months. Total debt stood at $62 million before the convertible debt offering, while current assets were almost double Aphria’s current liabilities.

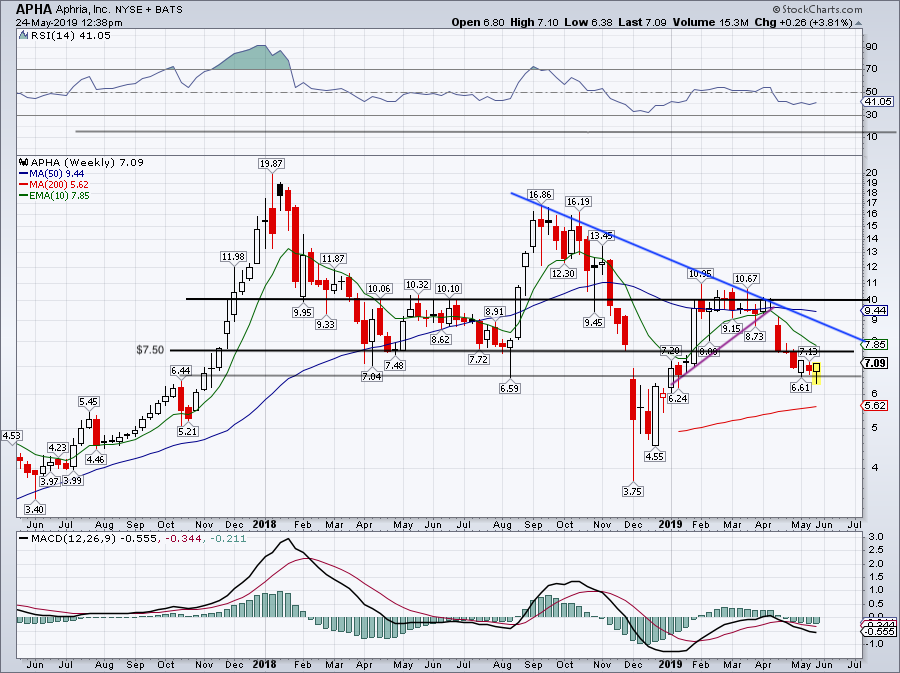

Trading Aphria Stock Price

Click to Enlarge

So where does that leave us?

Aphria quietly has a nice operation going as far as the cannabis industry is concerned. Will it be an eventual investment or takeover target by larger players? It could be, but investors need to remember the space they’re playing in. The cannabis industry is still speculative, and in particular, so is APHA stock. Why do you think we’ve seen shares go from $3.75 to $11 and back to $6.50 all since December?

According to Jefferies, the analysts are optimistic. On Friday they slapped a $15 (CAD) price target on the stock, saying there’s a “big disconnect between valuation and strategic positioning” and that we should see a “significant re-rating in shares.” That’s up 74% from Thursday’s close.

That upgrade is kickstarting Aphria into gear. It’s a good thing to, because Aphria stock was flirting with a big breakdown below this $6.60 level. Below and shares were surely heading lower. My downside targets would be (and still are if $6.60 fails as support) $6 and the 200-week moving average.

We need to see Aphria push through $7.50 and reclaim its 10-week moving average. If these levels turn to support and downtrend resistance (blue line) doesn’t weigh on APHA, a return to $10 could be the works.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell did not hold a position in any of the aforementioned securities.