Apple (NASDAQ:AAPL) has been rapidly increasing its research and development budget for the last few years. In the recent earnings report, Apple reported R&D expense of $3.9 billion. This was a 16.5% year-on-year growth. This has caused a fall in margins and puts pressure on the growth of Apple stock.

At the same time, the revenue reported by the company has dipped by 5%. This has led to a big increase in the R&D expense as a percent of the revenue. This metric increased from 5.53% in the year-ago quarter to 6.81% in the recent earnings.

Other competitors, including Huawei and Samsung, are also increasing their R&D expenses at a rapid pace. This will force Apple to further ramp up its efforts. The long-term impact of this trend is that Apple’s operating margin is getting squeezed due to higher expenses. It has also led to a fall in net income and EPS. Investors should keep an eye on the growing R&D bill of Apple and the impact it will have on Apple stock.

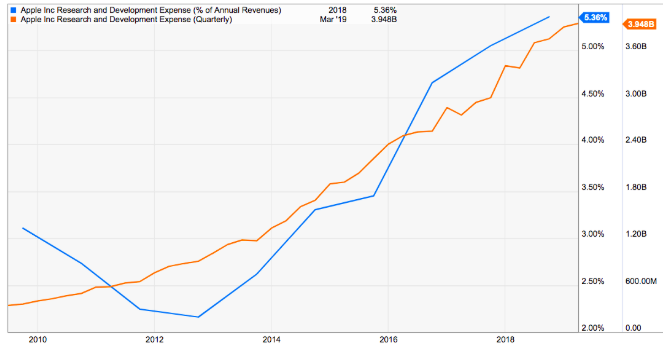

Rapid Growth Under Tim Cook’s Leadership

There has been a rapid increase in R&D expense since soon after Tim Cook took the CEO position.

The percentage share of R&D within the overall revenue has now increased to 5.36%. While this is much lower than other tech giants like Alphabet (NASDAQ: GOOG, NASDAQ:GOOGL), Facebook (NASDAQ: FB) or Intel (NASDAQ: INTC), it is still quite high compared to Apple’s historic R&D expense.

The R&D as a percentage of revenue saw a big jump in the recent quarter due to a slowdown in revenue and a big jump in R&D expense. If we continue to see a slowdown in revenue, this metric can easily increase by another couple of percentage points within the next few quarters.

It should be noted that Apple and the entire smartphone industry is preparing for a major tech change with the launch of 5G. This should force all the big tech giants, including Apple, to ramp up their R&D efforts.

Where Are the Competitors?

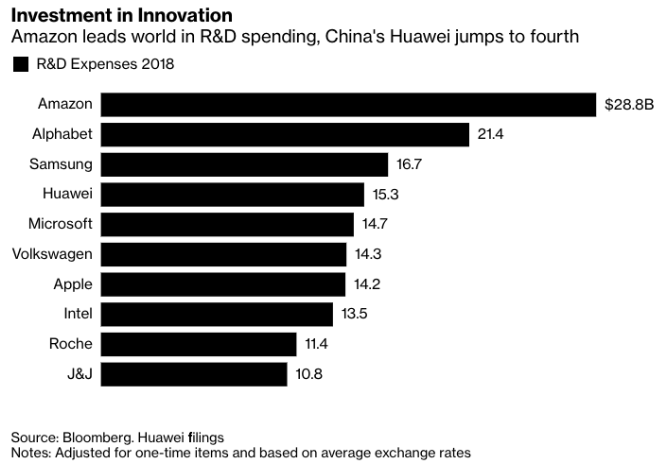

Despite Apple’s size and the rapid growth of R&D expense, it is surprising that other competitors have outspent the company. According to a Bloomberg report, Samsung has spent $16.7 billion on research in 2018. This is higher than $14.2 billion spent by Apple. Even Huawei, which has spent $15.3 billion, is ahead of Apple.

Source: Bloomberg

Apple also faces a challenge from Amazon and Alphabet, which are the main competitors in smart speaker category. Both of these companies are well ahead of Apple. As we see the rollout of 5G network and the launch of new devices relying on this tech, the research bill for these tech giants should grow massively. Apple stock is still dependent on the wow factor created by Apple products. More research spending by competitors can hurt Apple in the long run.

Impact on Margins

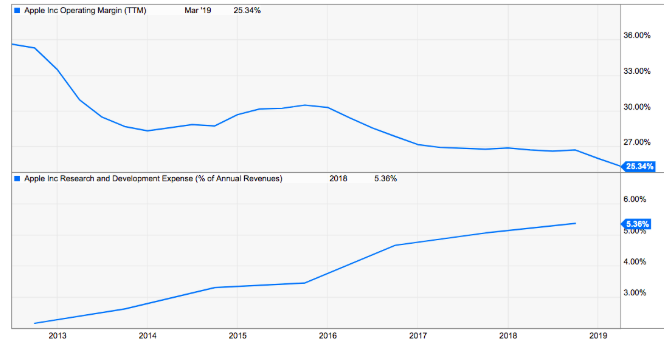

While Apple has been able to manage its gross margins in the 37%-38% range, the operating margin has slipped continuously for the past few quarters. In the latest quarter, operating margin fell by 288 basis points compared to year-ago quarter. This has had an adverse impact on net income and EPS. At the same time, Apple is facing pricing pressure on its flagship products. It is aggressively promoting trade-in programs and discounts in international regions.

Increase in R&D expense and fall in pricing power have pulled the margins lower. A fall in EPS ends up increasing the valuation multiple of Apple stock.

The R&D expense as a percent of revenue increased by 127 basis points in the latest quarter. This was one of the biggest items which led to a 288 basis point decline in operating margin. It is likely that we will see a much bigger ramp up in R&D expense from Apple in the next few quarters. Apple is also looking to have in-house chip development. There are several other new initiatives which could increase the research expense.

Long Term Benefits

An increase in R&D expense is always taken as a big positive for the long-term product pipeline of any company. And the secretive nature of Apple prevents us from knowing the products it is working on. But there are some negatives to the increasing research expense. For the past six years, Apple has increased its research expense rapidly, but its innovation lead over competitors isn’t huge. Huawei and Samsung have launched their foldable smartphones. They will also take the lead in the launch of 5G phones.

Apple has made a big dent in the wearable segment, but it has also performed poorly in the smart speaker segment. It remains to be seen how well the company can perform in the new services announced a few weeks back.

Research initiatives have a long gestation period. Apple could still show some new products which can spur sales. But, at least in the short term, investors should buckle up for further operating margin declines as the research bill eats up Apple’s healthy profits. A continuous fall in margins with stagnant sales should put pressure on any bullish sentiment for Apple stock.

Investor Takeaway in AAPL Stock

Apple has been investing heavily in research for the past few years. In the recent quarter, the research expense increased by 16.5% over the previous quarter while the revenue dipped by 5%. We can see a continuation of this trend in the next few quarters as iPhone sales are forecasted to be sluggish.

A rapid increase in research expense has reduced the operating margin. Apple has shown a year-over-year decline in operating margin in 13 out of the past 14 quarters. The operating margin decline in the recent quarter was a staggering 288 basis points. We should see further decrease in margins as the company increases research investment for the launch of 5G phones, chip production, new services, and other initiatives. A rapidly growing research expense and falling margins does not bode well for Apple stock in the near term.

As of this writing, Rohit Chhatwal did not hold a position in any of the aforementioned securities.