Visa (NYSE:V) beat expectations on Tuesday, expectations that were relatively high to begin with. The transactions processor reported revenue of $5.8 billion for the June quarter versus analyst projections of $5.7 billion. Earnings of $1.37 per share topped the consensus forecast of $1.33 per share of Visa stock.

Revenue was up 11% year-over-year, and income grew at roughly the same pace.

Yet, there’s a reason shares didn’t budge in response to the good news, however, even if current and would-be shareholders don’t consciously realize it. As reliable as the payment middleman has been, there are too many headwinds blowing at this time.

Four stand out among them, even if none are particularly noticeable liabilities.

Strong Dollar Hurts

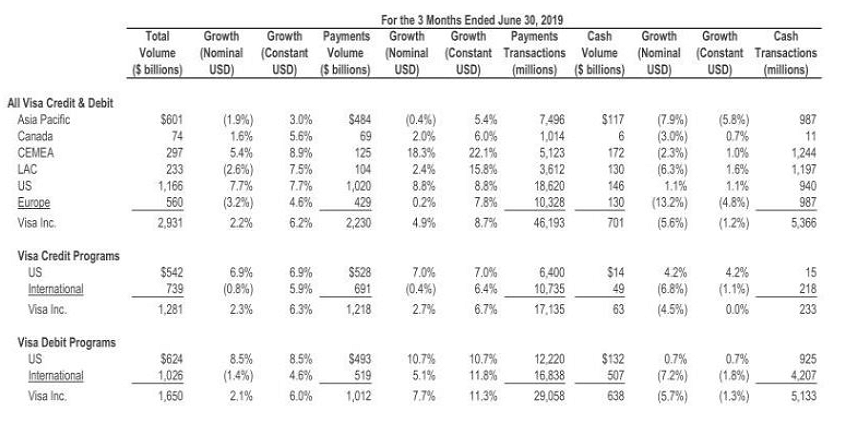

While it’s true for chief rival Mastercard (NYSE:MA) as well, and by and large, Visa has steered investors past the reality. Nevertheless, the strength of the U.S. dollar relative to year-ago levels is weighing on results. Last quarter’s per-share earnings, for instance, would have been up 18% on a constant-dollar basis. As Visa increasingly looks to overseas markets for growth, the adverse impact of a strong greenback — measured as nominal results compared to constant-dollar results — will grow.

Click to Enlarge

The prospect of lower interest rates could help soften the blow, which admittedly hasn’t become a stumbling block, yet. Neither is it a new dynamic.

Still, should the Fed be mistiming its plans to drag interest rates lower and ultimately set the stage for an unexpected and unintended inflation/dollar surge, Visa’s nominal results are increasingly vulnerable.

Overvalued at Current V Stock Price

Wall Street traditionalists are fond of saying, “you have to pay for quality” and Visa has unarguably delivered quality results. The premium that newcomers would have to pay for that quality right now, however, is significant.

As of the latest look, Visa stock is priced at 37 times

its trailing per-share earnings, and nearly 29 times its projected profits.

Those aren’t entirely outrageous figures. They’re at the upper, extreme end of the valuation range V stock has been able to sustain since 2017 though, leaving shares open to at least a modest rethinking of what Visa stock is worth.

Shares are Technically Overbought

One has to take a big step back and look at the weekly chart to realize it, but with this month’s gains, the rally that’s been underway since late last year has bumped into a resistance line that extends back to early 2017. Visa stock has been able to push through overbought conditions before, but hasn’t proven it can push this deep into overbought territory.

Click to Enlarge

Payments are Becoming a Commodity

Finally, although hardly a ticking time bomb, the former underpinnings of the payment business are shifting in a way that actually doesn’t favor Visa.

In its infancy, digital payments middlemen like PayPal Holdings (NASDAQ:PYPL) were a boon for card companies like Visa and Mastercard, which were given business they might not have otherwise garnered. The advent of Square (NYSE:SQ) only expanded the use of cards rather than cash, in that it catered to small and micro-sized businesses that had previously been unable to accept card payments of any type.

Technology is now being leveraged in ways that effectively circumvent the likes of Visa and Mastercard altogether. So-called peer-to-peer (P2P) payments leave traditional credit card companies entirely out of the loop.

Visa has pushed back against this trend where it could apply its best leverage, introducing a business-to-business (B2B) tool that has been given a reasonably warm reception.

Like it has on most other fronts though, the internet is democratizing payments, establishing ways to drive costs to make and receive payments to an absolute bare minimum.

Looking Ahead for Visa Stock

The first three concerns are more immediate; the fourth is a longer-term issue. All are working against the company and Visa stock investors, however.

Still, perspective is needed. The near-term headwinds are purely transitional or situational ones that have nothing to do with Visa’s performance; there’s nothing the company can do to address them. As for the commoditization undertow, it will become a bigger issue, though it’s a paradigm shift that will take years to fully play out. Visa will be fine in the meantime.

For traders wondering when and where Visa stock may be a name to step back into, however, the $156 area would be a line in the sand to note. V stock found a floor there several times during the second quarter, and the forward-looking P/E would be a more palatable (though still premium-priced) 25x at that level.

Anything less than $156 could be considered a bargain.

As of this writing, James Brumley did not hold a position in any of the aforementioned securities. You can learn more about James at his site, jamesbrumley.com, or follow him on Twitter, at @jbrumley.