As a bellwether to the broader economy, transportation giant CSX (NASDAQ:CSX) attracts for its historical stability. Though it incurred heavy losses during the 2000 tech bubble and the 2008 financial crisis, the company has found a way to come back twice as hard. Today, CSX stock is still trading relatively near its all-time high.

However, because the company is a bellwether, it raises questions when it doesn’t perform to expectations. Unfortunately, CSX received a painful reminder regarding this lesson.

On late Tuesday afternoon, management disclosed its second quarter 2019 earnings results. Although per-share profit was up 7% against the year-ago quarter, the transportation firm missed Wall Street expectations. That sent the CSX stock price down more than 6% during after-hours trading.

On paper, it wasn’t a terrible hit. Prior to the disclosure, consensus estimates pegged earning per share at $1.10. The actual tally was only two pennies shy of the forecast. By itself, this miss doesn’t warrant such extreme volatility toward the CSX stock price.

However, the revenue haul was a different story. Analysts expected the organization to bring in $3.16 billion in top-line sales. As InvestorPlace writer Karl Utermohlen noted, that would have represented a 2% lift on a year-over-year basis. Instead, the transportation firm rang up only $3.06 billion, a nearly 1.4% slide. Naturally, several stakeholders panicked out of CSX stock.

To be fair, CSX has delivered outstanding revenue performances over the past few quarters. Specifically, between Q2 2018 through Q1 2019, sales growth YoY averaged 8.6%. Therefore, it’s possible that investors expected too much out of the organization, and unfairly punished CSX stock.

Caution Is Key for CSX Stock

2018 was a banner year for both CSX and CSX stock. The company generated nearly $12.3 billion in annual revenue, up 7.4% from 2017 results. Moreover, it was the biggest sales haul since 2014. Thus, CSX had the disadvantage of a tough year-earlier comparison.

Another factor (and a bullish one) to consider is the underlying economy. Despite fears about a coming recession, key metrics such as the unemployment rate and consumer confidence

indicate that the economy is robust. If accurate, this dynamic has positive implications for the CSX stock price.

Let’s face it: you probably wouldn’t even consider this name if we were in a recession.

With all that said, I believe investors should adopt a cautious approach with CSX stock. A major red flag that I see with shares is a clear disconnect with the fundamentals.

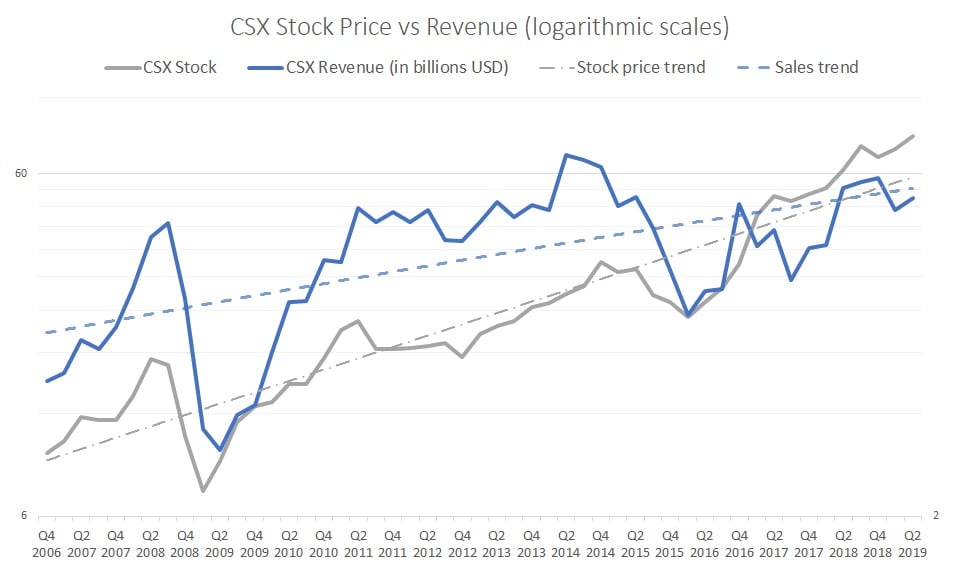

Between Q4 2006 through Q4 2015, the CSX stock price had an 86% correlation coefficient with the underlying firm’s revenue. Stated differently, as revenue increased, so too did shares. And the opposite dynamic was also true.

Click to Enlarge

But from Q1 2016 onward, the correlation strength dropped to 80%. That’s still a statistically significant rate. However, revenue and the CSX stock price didn’t always match up as neatly as they did in the past. Particularly, shares jumped considerably while the company made mostly modest (notwithstanding 2018 results) sales gains.

And I think this is why investors jumped ship following the Q2 disclosure. Prior to the earnings report, CSX stock was heading toward overbought territory. However, stakeholders demonstrated that they’re willing to drive the price higher, so long as the growth narrative remains intact.

The last report demonstrated that this narrative is suspect; hence, the fallout in shares.

No Other Confirming Factors Support CSX

I don’t think I would issue a cautionary note for CSX stock if I had other supporting factors. However, I’m not getting a good read from the fundamentals nor the competitive landscape.

For example, rival Canadian Pacific Railway (NYSE:CP) also released its Q2 earnings report. The difference, though, was that Canadian Pacific produced strong results, beating on both per-share profitability and revenue.

Regarding fundamental headwinds, our own Thomas Niel mentioned coal demand. Thanks to the Trump administration, coal became a hot-button issue on the political front. However, Niel cited industry data that indicated a downward trend in consumption. In all likelihood, this decline will continue, which doesn’t help CSX’s cause.

Finally, sustained economic strength could help buoy shares. But despite strong economic print, this optimism isn’t guaranteed to last forever. We’re in a contentious political environment. International flashpoints threaten to undermine our relative peace. And we still have a trade war to figure out.

At this point, I think it’s fair to say that CSX has more challenges than upside catalysts. As such, I’m going to stay on the sidelines.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.