Seemingly in recent years, technology-related initial public offerings fall into two camps: those who perform stunningly well, and those that crumble badly. Identity management specialist Okta (NASDAQ:OKTA) definitely belongs in the former category. In April of 2017, OKTA stock started off with an IPO price of $17. Today, shares are a little bit shy of $116.

Despite a general slowdown that started in August of this year and was exacerbated last month, Okta Inc stock has nevertheless enjoyed an overall brilliant performance. Since this January’s opening price, OKTA has gained over 89% in the markets. And in the current month, shares are up nearly 18%.

It’s one of the few bright spots in an environment mostly focused on the unpredictable U.S.-China trade war negotiations. Further, the narrative behind this conflict helps bolster the argument for OKTA stock.

While the headlines focus on the economic aspect of the trade war, what gets lost is how we got here. Unbalanced trade deficits, as well as China’s stealing of intellectual property (IP) from American tech firms like Micron Technology (NASDAQ:MU), have long dogged prior administrations. Contrary to the traditional strategy, though, President Donald Trump has thrown diplomacy out the window, instead opting for geopolitical hardball.

But underlining this nasty and ongoing dispute is the need for digital security. OKTA specializes in identity management, which involves much more than making sure only the right people can access specific information. Rather, the company recognizes that we live in a digitally interconnected world. Their technologies facilitate collaboration while still protecting IP and other valuable assets.

In the past, this has driven Okta Inc stock. But is there enough room today for a repeat performance?

Okta Stock Is Interesting, but Not at This Price

Over the past few years, we’ve seen tech upstarts like Twilio (NYSE:TWLO) impose an outsized influence relative to their size. OKTA stock operates under a similar principle.

Undoubtedly, one of the top attributes for the company is its scalability. Rather than an individual company investing in its own security protocol, it often makes economic sense to outsource this function. As a specialist, OKTA can provide cost-effective solutions quickly, thus driving the case for Okta stock.

At the same time, being a specialist has some drawbacks. Because these types of companies operate in a relatively narrow focus, they lack robust revenue diversity. If growth slows down in a key market, it could lever a larger-than-normal impact. And that’s what I believe happened with OKTA stock in recent months.

In August, management released its earnings result for the second quarter. On paper, the company beat both per-share profitability and revenue expectations. However, Okta stock slipped on the announcement, and tumbled days later.

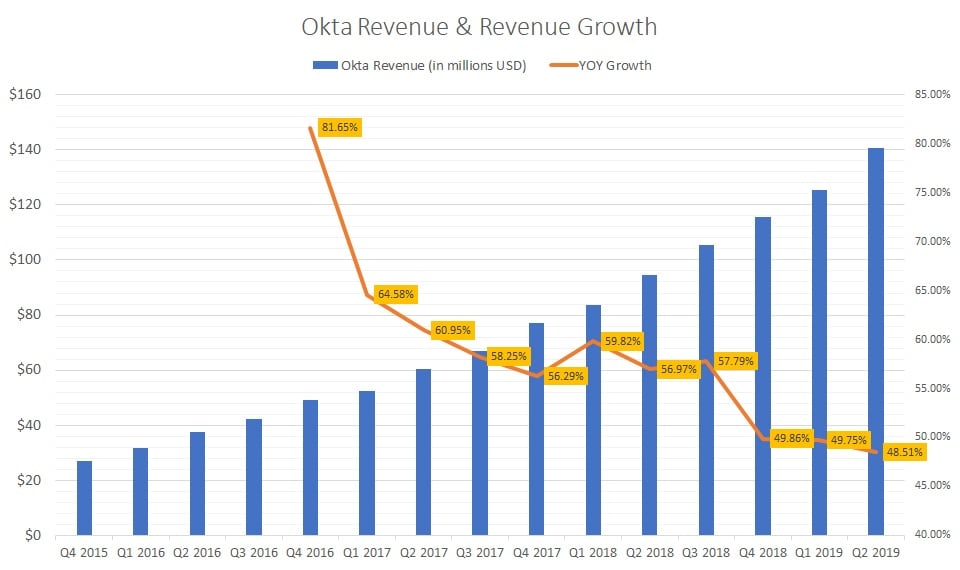

Sure, the company produced some impressive numbers. But on a longer-term timeframe, those figures are becoming less impressive.

Click to Enlarge

For instance, in Q4 2016, OKTA rang up $49.3 million in sales, which represented nearly 82% growth year-over-year. In Q4 2017, the company delivered revenue of $77 million, but a growth rate of “only” 56%. One year later, the sales tally increased to $115.5 million, but the growth rate declined again to just under 50%.

In the Q2 2019 report, OKTA drove home $140.5 million, while sales growth slipped to 48.5%. Of course, all companies experience growth declines as they progress nominally. But with OKTA stock having gained so much, investors wanted to see more.

They didn’t get it, which resulted in volatility for shares.

Low Barrier to Entry

Another potential risk factor for Okta Inc stock is the relatively low barrier to entry for the target industry.

Ironically, the attribute that makes OKTA stock so compelling – effective security solutions for corporations – is what makes it vulnerable to competition. Interestingly, management has invested funds into blockchain technology to bolster its security offerings.

Currently, few players can do identity management quite like Okta Inc. But tellingly, the blockchain is an open source innovation. Thus, another upstart with a better way of doing business could end up disrupting this space.

And it’s almost inevitable that identity management will attract more competitors. Looking at OKTA’s cost of goods sold, they’re very low relative to top-line sales. With quarterly gross margins consistently coming in above 70%, this is not the most capital-intensive industry.

That’s not to say that you should ignore OKTA stock indefinitely. But at the current price, I think the risks outweigh the rewards.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.