Snap‘s (NYSE:SNAP) description of itself — “Snap is a camera company” — is very simple. But here is another simple statement about SNAP stock: It is super overvalued.

There is no logical reason why a simple camera company should be valued at $21.25 billion. It produces nothing but losses in every important category.

Snap likes pictures. So I am going to present a lot of Snap’s financial pictures. Snap’s growth on the surface seems impressive. But there is nothing but losses underneath.

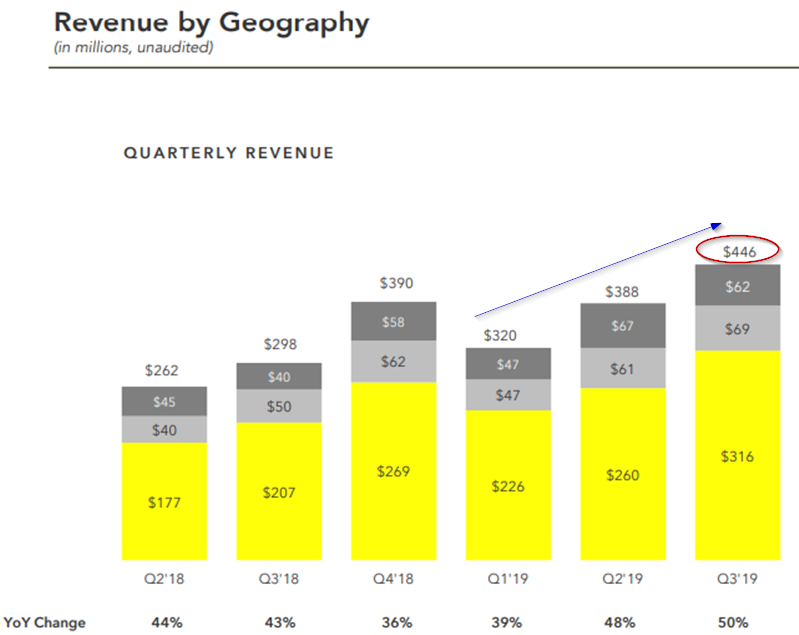

For example, revenue has been moving upward at a nice clip, as can be seen in the latest quarterly presentation. On a YoY basis, revenue rose 50% and even on a QoQ basis, it increased by 15%.

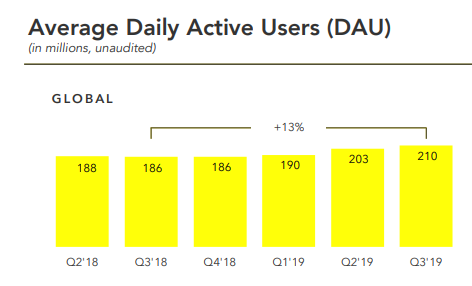

And other important metrics are improving, such as Average Daily Average Users. The chart at the right shows that the average DAU rose 13% YoY and 3.4% quarterly.

Snap Stock Is Hurt As Losses Continue

But in Q3 the net income and “Adjusted” EBITDA cash flow losses continued in negative territory. Now if you read any of my articles in InvestorPlace you know that I don’t agree with the “adjustments” that many loss-making companies like SNAP do to prettify their earnings.

For example, you can read my articles about Square (NYSE:SQ) and Shopify (NYSE:

SHOP) which, just like SNAP, add back their stock-based compensation (SBC) expenses.

The theory is that the vesting of the underlying issued shares or options has not yet occurred, therefore there is no real dilution at the present.

But that is extremely short-term thinking. The vesting occurs each quarter and the chart below shows that the SBC expenses are not one-time occurrences. They happen quarterly, therefore they are not irregular expenses.

Snap’s net income and adjusted EBITDA cash flow losses continued unabated during Q3. In the past 12 months, Snap has lost close to $1 billion (-$984 million) in net income and $294 million in adjusted EBITDA. In fact, adjusted EBITDA losses of $42 million in Q3 were roughly similar to the Q4 2018 losses of $50 million.

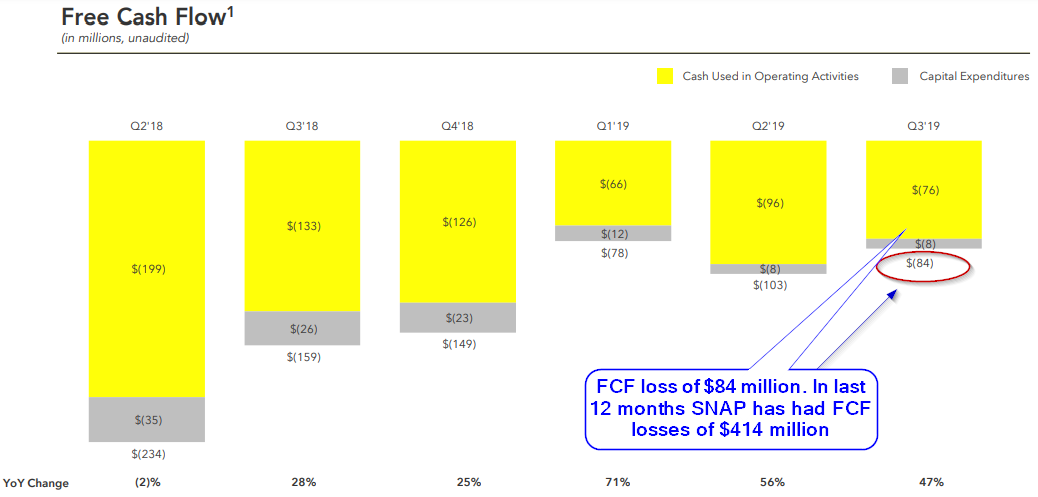

FCF Losses Continue at Snap

More to the point, free cash flow (“FCF”) losses also persist at Snap. The $84 million FCF loss in Q3 was even worse than the Q1 2019 loss of $78 million. In fact, over the past 12 months, Snap has bled out $414 million in FCF. This is only slightly better than the Q2 TTM FCF losses of $489 million.

In the end losses FCF matter. It drains the company’s cash and securities balance. At the end of Q2 2019, Snap had only $1.2 billion in cash and securities. If you add up all the losses and spending during Q3 from their cash flow statement, you see that Snap drained out $867 million. If Snap had not raised more money — $1.25 billion in convertible notes — the cash, and securities balance would have fallen to just $333 million.

In other words, shareholders got diluted through the convertible notes and had to pony up more money to keep the losses financed.

How Do You Value Money-Losing Snap Stock?

Snap stock is up over 175% so far this year. Speculative investors don’t care about the losses. The point that impresses them is the fact that the revenue and DAU metrics are going. Oh, and the losses seem to be getting smaller. So let’s give it a $21 billion valuation in hopes that within several years the losses turn into profits.

The underlying theory is that operating leverage comes into play. That is, with every new marginal dollar in revenue, the gross profit increases faster. And since the operating cost base is fairly stable Snap should be able to leverage revenue into faster growth in profits. The fact that the numbers are negative now is irrelevant.

The problem with this thinking is that it is speculative in nature. It is another form of gambling. There is simply no margin of safety in the valuation. In fact, you cannot really value a loss-making company like SNAP without this anticipation or forecasting of future profits.

In fact, the company may need to continue to dilute shareholders by raising more capital

This is exactly the opposite of what value investors do. They look for defensive investments where the value of existing assets is greater than the existing stock price and there is no undue reliance or speculation on the future of the company’s performance.

What Should YOU Do on SNAP Stock?

In short, you need to decide whether you are a gambler or a saver. You need a speculative mindset to wrap your head around a justification to buy SNAP stock. It has a $21 billion valuation but made $414 million in FCF losses in the past 12 months.

Is the company really going to turn FCF positive at any time in the near future? If you think so, go ahead at this valuation and gamble on Snap stock.

As of this writing, Mark Hake, CFA does not hold a position in any of the aforementioned securities. Mark Hake runs the Total Yield Value Guide which you can review here. The Guide focuses on high total yield value stocks, which includes both high dividend and buyback yields. In addition, subscribers a two-week free trial.