Sometimes, the market throws you a curveball. Recently, eCommerce giant eBay (NASDAQ:EBAY) has been pitching investors some nasty stuff. On the surface, you expect eBay stock to steadily move higher based on its underlying powerful brand and generally strong growth potential. However, even the best of us can be caught off guard.

Case in point is Piper Jaffray chief market technician Craig Johnson. Ahead of eBay’s third-quarter earnings report, Johnson expected the stock price to move higher. Citing positive technical developments, shares did look like they were charting a recovery. Not only that, EBAY was outperforming eCommerce king Amazon (NASDAQ:AMZN).

However, once the dust settled from the Q3 report, EBAY failed to rally. In fact, shares dropped substantially lower, reaching levels not seen since early this year.

Adding insult to injury, the Q3 results seemingly didn’t justify the volatility. Against a non-GAAP earnings-per-share target of 64 cents, EBAY delivered 67 cents. On the revenue front, the company rang up sales of $2.65 billion, up from the consensus $2.64 billion. And a metric that should have driven eBay higher was its active buyer base, which increased 4% to 183 million people worldwide.

So, why did the EBAY stock price collapse like it did? Not everything about the Q3 report was positive. For instance, while revenue beat expectations, it was flat against the year-ago quarter. Further, operating income was $310 million, a 57% drop from Q3 2018 results.

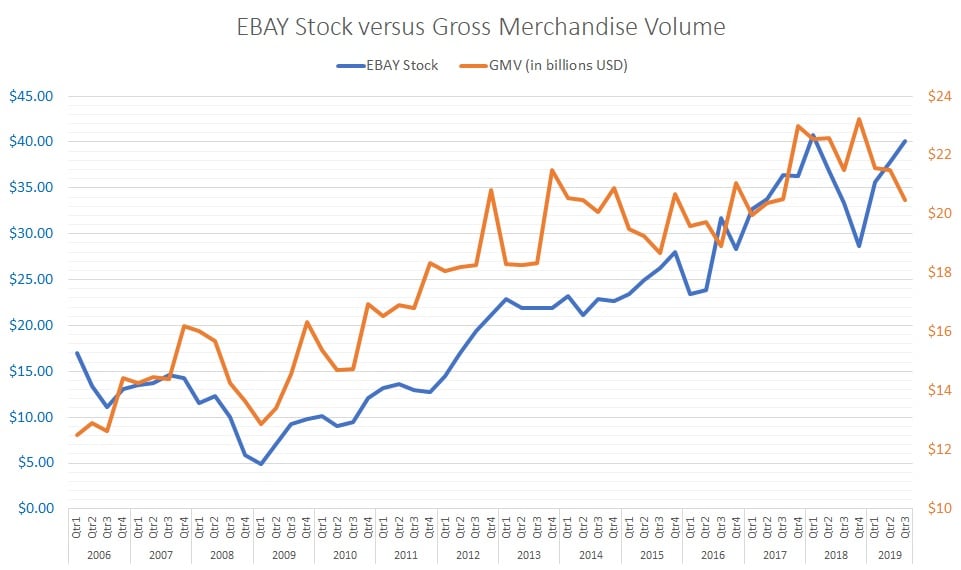

Still, any company can have a bad showing. What really hurt the stock here was its gross merchandise volume, which slipped nearly 5% year-over-year. That’s the key metric for shares, which I’ll quantify below:

For eBay Stock, GMV Is King

Typically, I don’t like to use any single metric for assessing the viability of a publicly-traded company. But for eBay, I’ll make an exception because mathematically, GMV is an accurate predictor.

At first, this statement might bemuse you. While GMV is fundamentally a useful indicator for eCommerce companies, it also has flaws. According to TheBalanceSMB.com contributor Aron Hsiao:

In terms of economics, GMV is a raw figure that doesn’t offer much insight into the value of the items sold because it doesn’t factor in any costs accrued by the retailer. Additionally, GMV doesn’t include discounts or returns, or the cost of keeping and storing inventory before it’s sold.

It’s not even a good predictor of net sales, which is a more accurate representation of a company’s overall financial health. Even for e-commerce sites like Amazon, the site’s revenue is not calculated based solely on the dollar value of items sold.

Why then use GMV to analyze EBAY? Simply put, eBay’s GMV and the EBAY stock price have a very strong direct correlation with each other: as GMV moves higher, so too does eBay shares. I calculated the correlation coefficient as a whopping 85%.

Click to Enlarge

Fundamentally, you can make the argument that eBay’s fee-based revenue source imposes greater importance to GMV. You can also make the case that stakeholders are accustomed to rising GMV.

Certainly, over the years, GMV has grown considerably. But in recent quarters, the metric has gone flat to declining.

Whatever the case, the math is clear: eBay stock doesn’t thrive on declining GMV. As such, shares are overvalued (relative to this metric). Until the company can prove otherwise by increasing GMV substantially in Q4, the equity remains incredibly risky.

EBAY Stock Is a Falling Knife for Now

Following the now not-so-great Q3 earnings report, investors will question whether the e-commerce marketplace still has the right stuff. Several years ago, EBAY was an ace pitcher in his prime. Having tacked on some years to his arm, the situation is murkier.

Now, I somewhat agree with our own Will Healy, who states that an opportunity still exists with EBAY. As Healy points out, the global online auction marketplace will continue to grow. And in that space, eBay is king thanks to a long-established track record.

So yes, at some point, eBay stock will become a compelling buy. I just don’t think that time is now. Again, shares are incredibly overvalued relative to sharply declining GMV. Until I get a better read for Q4 and beyond, I’ll sit on the sidelines.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.