Qualcomm (NASDAQ:QCOM) has been enjoying a steady march higher over the past few quarters. Despite some bearish short-term developments on the chart, the long-term trends point higher, while the fundamentals suggest that prosperous times lie ahead for the company.

Does that make Qualcomm a screaming buy? I wouldn’t say screaming, but it is a name that investors may want to keep on their radar.

The company’s resolution with Apple (NASDAQ:AAPL) adds clarity to its business model, although some legal snares still threaten to create future volatility. Of course, it helps that Qualcomm pays a healthy dividend too. Despite the big one-year rise in the stock price, shares still pay out 2.85%, while boasting solid growth projections. Outside of say, Broadcom (NASDAQ:AVGO), not many stocks can make such a claim.

Let’s take a closer look at Qualcomm.

Valuing Qualcomm

In fiscal 2019, Qualcomm earned just $3.54 per share in profit. After rallying 56% over the past 12 months, it leaves shares trading at 24.5 times its trailing earnings. However, when we look at current earnings (this fiscal year) or forward earnings (next fiscal year), the valuation becomes more reasonable.

Analysts expect earnings of $4.19 per share this year. That’s up almost 20% from 2019 and leaves Qualcomm trading at 20.8 times this year’s earnings. Alongside the expected jump in earnings, analysts expect revenue to increase 13%.

Here’s where it takes some guesswork. Qualcomm is only one quarter into the current fiscal year and hasn’t even reported those first-quarter figures yet. As a result, I don’t typically put much weight in out-year estimates. But because they are so impressive for Qualcomm, I must mention them.

Analysts expect revenue growth of 13% in 2020 to accelerate to 23% growth in fiscal 2021. On the earnings front, they expect growth of 18.4% this year to accelerate to more than 45% next year. If achieved, this represents an incredible growth profile over the next eight quarters (24 months), particularly for a company with a $99 billion market capitalization.

Based on 2021’s estimates, Qualcomm stock trades at just 14.2-times earnings. Margins and free cash flow improved notably in 2019 and if that trend continues in 2020, it will more than justify a higher stock price for Qualcomm investors.

How to Trade Shares

We should mention that Qualcomm isn’t without risks. First, much of what I just mentioned is based on estimates. Should those estimates change, then so does the thesis for owning the stock. A shakeup with Apple or legal action from the FTC could throw a wrench in the long thesis too.

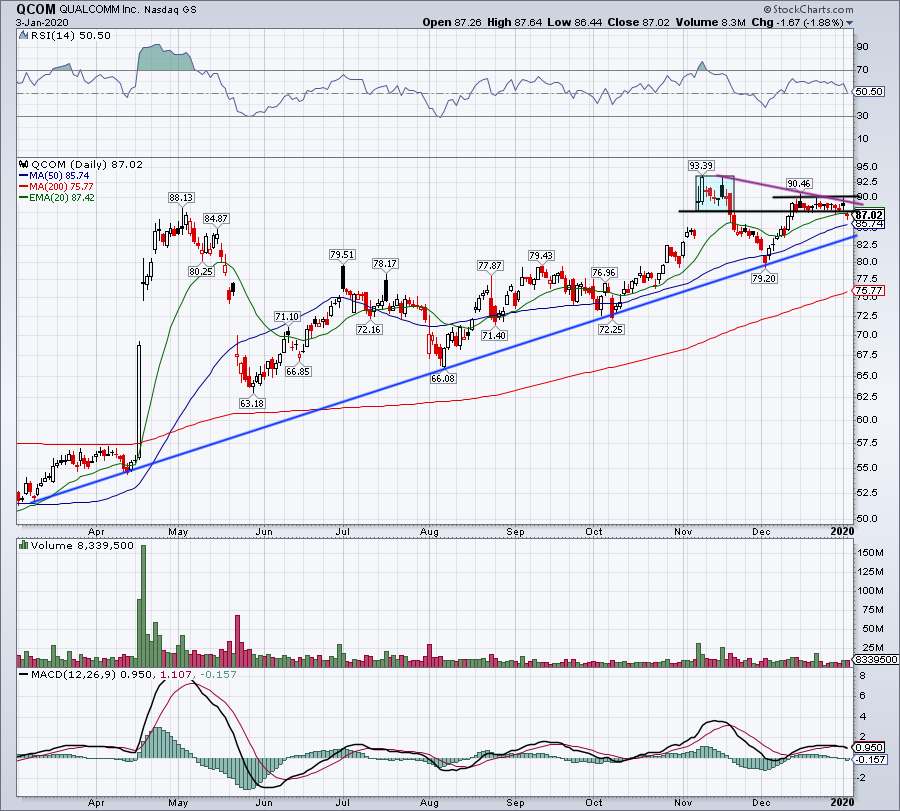

Click to Enlarge

As it stands though, the longer-term themes are in place to elevate Qualcomm’s share price. So, what do the charts look like?

Actually, pretty good. The long-term trends remain bullish, while the short-term action has been consolidation. That changed a bit on Friday, shifting to a more bearish tone as the stock broke below recent support. But without any follow-through, the move could certainly be a false breakdown.

In early November, Qualcomm shares gapped higher on better-than-expected earnings. Shares consolidated in a $5 range for several weeks, between $87.50 and $92.50, before breaking lower. The move sent shares tumbling down to the 50-day moving average in early December.

After recovering and consolidating in an even tighter range, shares of Qualcomm broke below support on Friday. If the stock can reclaim this level early next week, bulls may be okay.

Otherwise, look for a dip down to the 50-day moving average and/or uptrend support. Bulls can buy this dip provided support holds. Below these marks will be reason to exercise more caution in the intermediate term.

On the upside, investors need to see several things happen. First, Qualcomm needs to reclaim $87.50 and the 20-day moving average. Above puts recent resistance at $90 on the table, as well as short-term downtrend resistance (purple line). Above puts the post-earnings high of $93.39 on the table and over that, $100 is possible.

Bret Kenwell is the manager and author of Future Blue Chips and is on Twitter @BretKenwell. As of this writing, Bret Kenwell is long AVGO and AAPL.