Almost since its introduction, cybersecurity specialist FireEye (NASDAQ:FEYE) has turned into an investment where the broader bullish fundamentals haven’t translated into consistent market returns. For the last four years, FEYE stock has largely moved sideways, punctuated by the occasional (and temporary) swings higher. And with the cybersecurity firm’s fourth quarter of 2019 earnings results, initial signs suggest sustained apathy.

It’s becoming a familiar tale for long embattled stakeholders. Generally speaking, FireEye usually delivers the goods on paper. But making it stick for FEYE stock has confounded proponents. This time around, the company delivered adjusted earnings per share of 7 cents, easily beating out Wall Street’s consensus target of 4 cents. In the year-ago quarter, FireEye produced an EPS of 6 cents against a 5-cent estimate.

On the revenue front, the company rang up $235.09 million, again convincingly beating the Street’s consensus target of $226.61 million. As well, the most recent haul beat out Q4 2018’s tally of $217.53 million.

Still, during the after-hours session, FEYE stock crumbled 5%. Do investors have any reason to believe in the cybersecurity firm?

For one thing, not everything about the Q4 report was all peaches and cream. Although FireEye’s operating loss of $35.09 million represented a 4.4% improvement year-over-year, management disclosed a net loss of $49.2 million. That’s a bit worse than the year-ago quarter’s net loss of $48.4 million.

But most investors probably felt discouraged from the company’s 2020 outlook. The leadership team expects “revenue of $935 million to $945 million.” However, analysts were looking “$946.08 million for the year.”

Though it might appear a small miss, analysts sorely need robust revenue growth to feel confident in FEYE stock.

Uninspiring Revenue Trend for FEYE Stock

From a topical perspective, the bull case for FireEye shares is patently obvious. According to DigitalGuardian.com, the average cost of a data breach can greatly vary depending on the affected country. However, victimized entities can expect to pay anywhere between $1.25 million to $8.19 million. Not only that, the U.S. occupies the highest point of this range.

Furthermore, cybersecurity is a dubiously attractive crime for those who have the skill and talent to pull it off. Unlike a physical crime like a bank robbery, there’s very little chance of immediate violence. Plus, in the case of digital attacks like identity theft, the overall impact is asymmetrical: little to no physical risk against the ability to steal from anywhere.

If you’re smart enough, you can commit the perfect crime. Therefore, the allure of cyberattacks will only increase in the future.

The flipside of this dynamic is that more people and enterprises are incentivized to invest in cybersecurity mechanisms. While the average breach may “only” cost a few million dollars, not all breaches are equally damaging. Some compromising incidents, like the Equifax (NYSE:EFX) disaster a few years back, can impact entire nations.

Therefore, preventing or at least sharply mitigating just one catastrophic cyberattack is well worth a premium cybersecurity contract. But the problem for FEYE stock is it has no beef.

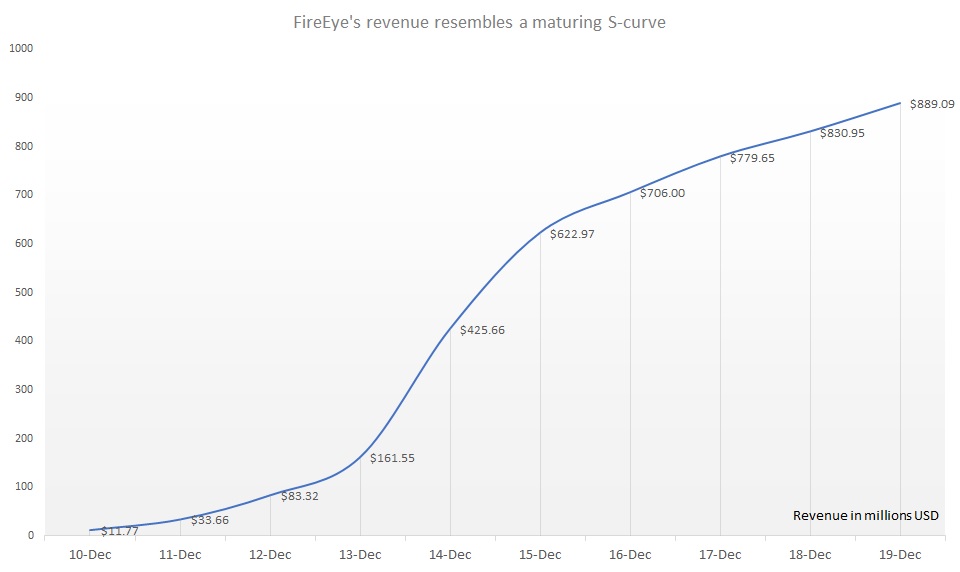

With the Q4 results, FireEye delivered a total 2019 revenue of $889 million. That’s only a 7% increase from 2018’s tally. Since 2016, annual sales growth is a relatively paltry 9.3%. This compares unfavorably to the 127%-plus average growth rate between 2011 through 2015.

Click to Enlarge

Ominously, FireEye’s nominal revenue trend looks like a maturing S-curve.

In contrast, Palo Alto Networks (NYSE:PANW) averages sales growth of 61.4% since 2011. Simply put, the optics are terrible.

The Case for Speculation

If you’re a risk-averse investor, both the financials and the technicals are speaking in unison: stay away! From the latter point-of-view, FEYE stock hasn’t done anything in the past four years. On the financial end, FireEye has failed to convert a positive industry backdrop into sales.

Plus, far better options exist in the space.

That said, the most compelling bull case for FEYE stock is the addressable market. As big as it is now, it’s only going to get bigger in the future.

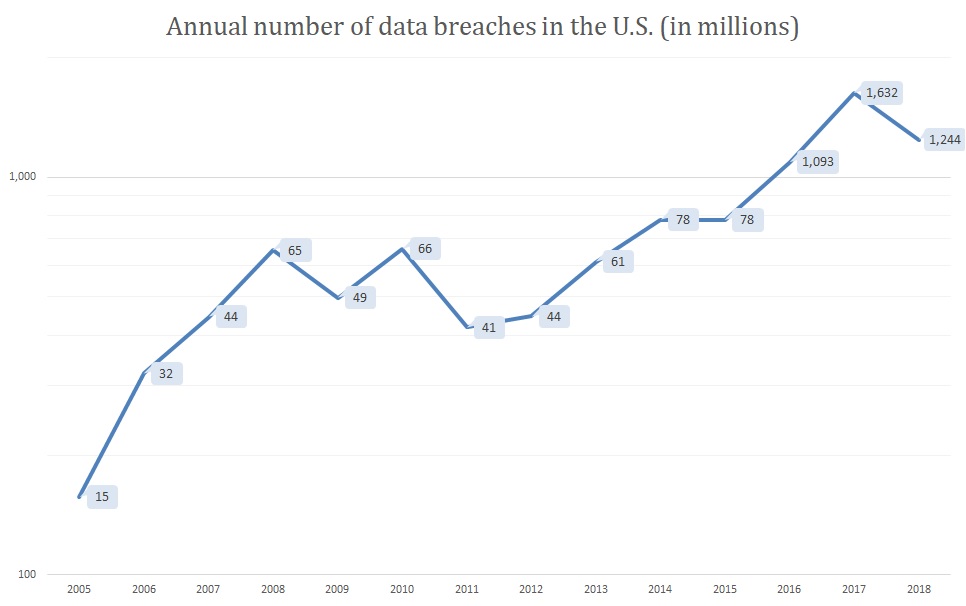

Click to Enlarge

In recent years, we’ve seen a huge increase in the number of data breaches in the U.S. In 2018, we suffered a total of 1.24 billion breaches. That however paled in comparison to 2017, where we saw 1.63 billion attacks. Combined with 2016’s tally, the number of breaches amounts to 3.97 billion.

To put this figure into perspective, this total exceeds all the breaches suffered from 2005 through 2012. With ever-expanding technological platforms and the digitalization of everything, we should expect this trend to worsen.

Of course, that’s bad news for organizations that will invariably fall victim to cyberattacks. However, it opens wider the revenue-making opportunities for FireEye.

I get it: we’ve heard this narrative before. But if you’re a gambler, the addressable market has factually become larger for FEYE stock. That’s worth a careful, measured bet.

As of this writing, Josh Enomoto did not hold a position in any of the aforementioned securities.