Before we look for any trading ideas this week, we have to acknowledge the level of panic in the global equity markets. They are all in free fall, and no one should be so confident in a thesis to take on the risk in size and without protection. There is no shame in missing the perfect bottom, so the goal is not to seek one. However, great champions are at their best under duress — and a few chip stocks are looking good.

When the S&P 500 and chip stocks fell 5% on Wednesday, Advanced Micro Devices (NASDAQ:AMD) stock rallied 0.7%. However, it was the only green among the losers. Nvidia (NASDAQ:NVDA) and the VanEck Vectors Semiconductor ETF (NYSEARCA:SMH) fell about -5.5%, while Intel (NASDAQ:INTC) stumbled -4.3%. There were no buyers, yet the AMD bids kept coming as the indices were falling fast and furious.

Moreover, this is nothing new because AMD stock was the best performer in the S&P last year. This is a rare feat, so it only makes sense to stick with the winners — and part of today’s point is to snipe entry levels for these chip companies.

The other part is to place them in order of preference. Clearly, I place AMD as number one. And NVDA would be second if not for the uncertainty in the headlines. It’s also riskier than INTC now because it has more froth to shed if this malaise persists. Otherwise, Nvidia stock is second best.

Overall, the logic is simple and it helped me decide on the order of preference. If INTC is rallying, then so are the other two. But as we saw yesterday, AMD doesn’t need them to rally. Therefore, I cannot assume that if AMD is rising that so are Nvidia and Intel. So, the strategy is to stick with the winner and let the bet roll.

That said, let’s take a look at these three chip stocks to buy on this huge dip.

Chip Stocks To Buy: Advanced Micro Devices (AMD)

Click to Enlarge

You already know my bias for the AMD stock above all the other major chip stocks. This is because of the company CEO Lisa Su.

Wall Street gives her credit for a tremendous turnaround plan that has shown a lot of results. and more due to come later. With that lies the catalyst, but also the risk. Should she leave the company, the stock will suffer tremendously on the headline. And whether or not it bounces from it would depend on how strong is the bench behind her. This is not my forecast, but I have to contemplate the risk.

Moreover, AMD stock is not cheap. In fact, it would cause my eye to twitch if I only look at its price-earnings (P/E) ratio of 160. But, this is a growth stock, so using the P/E to gauge its value would be a mistake. Chip stocks are not typically cheap so it’s important to look at other metrics. In this case, using the sales line makes sense. AMD sells at 8 times its full year actual revenues. As you will see later, it’s relatively cheap and not the shocker of a stat.

Additionally, the technicals are also important and the AMD stock chart suggests that the zone around $40 is pivotal. These usually provide support on the way down. But if it fails, then there is risk to the next level near $36 per share.

Knowing this, give the bulls some comfort to know that there should be buyers below if this malaise worsens. In a recent write up, I noted that as long as it held above $43 per share, the buyers are in control.

Catching falling knives is dangerous, especially when the globe is panicked over the coronavirus from China. So, instead of risking $45 per share without any protection, I prefer collecting $2.70 per contract to sell the January $23 put. Meaning, I would be paid for the opportunity to own AMD stock 50% cheaper; I don’t even need a rally to profit.

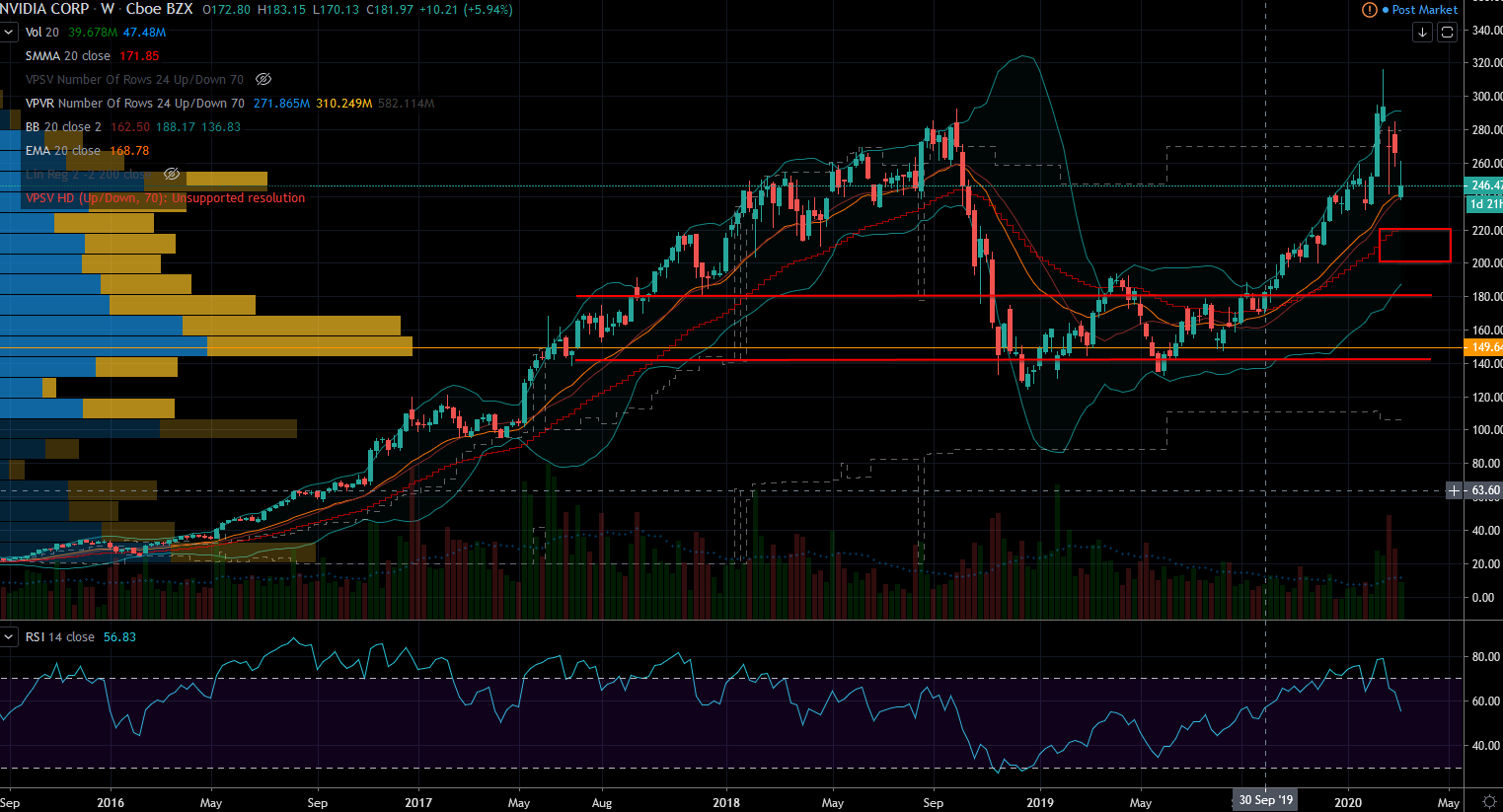

Nvidia (NVDA)

Click to Enlarge

NVDA stock has had a wild ride in the last two years. It rallied furiously to $290 per share before the October 2018 correction. Then, it collapsed 50% to $125 before it found a bottom.

Last summer, investors fell back in love with it and couldn’t have enough of its stock. It peaked after the earnings report in a fantastic breach of its highs set back in 2018. However, this shake up has knocked it down a few notches — but a 23% drop is not enough for me to get easy with the idea of catching it here.

Overall, the problem for me is that NVDA sells at a whopping 15 times sales. And if the problems with the coronavirus persist and disrupt the order flow, then it’s easy fat for investors to trim. The stock would fall fast to fix this potential inequity; Remember that AMD stock is 50% cheaper already from that perspective.

Sure, I bet I can find experts who know the industry way better than me. But the logic even at this macro level stands true on its own. Theories behind owning stocks should be simple. If I have to fish for an obscure reason, then perhaps I would be merely justifying my intent and not really looking to gauge its viability. In this case, I know that this bunch’s products and services will be in demand and the barriers to entry are huge. And therefore, chip stocks will be fine for the next decade.

Intel (INTC)

Click to Enlarge

Among these three, if I wanted cheap, then Intel is the winner. But in this case, you get what you pay for — and this stock has been a serial disappointer.

It did come to life late last year, but I need more time to get comfortable with the idea that it’s out of the woods. Responsibility is on management to prove to investors that they are back on track. This used to be the giant, and now it seems like it’s playing catch-up.

Technically, INTC stock already fell into a well-consolidated zone. From that perspective, it has the least obvious pitfall on its chart if this selloff continues.

However, that alone is not a reason for me to buy. But those who like to chase true value Intel is definitely the one. It has a very humble 11 times earnings, and only 3.5 times its sales. So clearly, there isn’t a lot of fat to trim in case of more trouble.

Nonetheless, I am confident that if the sellers want to, they will sell it down just as hard as the other two. I remember when Micron (NASDAQ:MU) fell to two times earnings, and it was still called a value trap.

Nicolas Chahine is the managing director of SellSpreads.com. Join his live chat room for free here. As of this writing, he did not hold a position in any of the aforementioned securities. Join his live chat room for free here.