Few industries have been battered as badly by the novel coronavirus pandemic as the airlines. As a case in point, Delta Air Lines (NYSE:DAL) stock is still down nearly 60% from its 52-week highs, and that’s after rallying 56% from its recent lows.

Trading at such a haircut, it’s tempting to go bottom-fishing in DAL stock. After all, the best opportunities for value investors come when the crowd is running for the door.

That said, I wouldn’t be in hurry. DAL stock looks cheap at first glance, but there are no guarantees that the airline makes it through this experience intact or at least without having to dilute its shareholders with a large secondary offering.

As a case in point, rival American Airlines (NYSE:AAL) just raised nearly $2 billion in stock and convertible bonds. This staves off the threat of bankruptcy for now, but it comes at a price. That $2 billion accounts for about 36% of American’s market cap, which is shockingly high dilution for the existing shareholders.

Remember, the proceeds of the offering weren’t used to finance growth initiatives. They were used to plug a massive hole in the budget. That means the earnings pie didn’t get any bigger, yet all the existing investors get slices that are now 36% smaller.

Southwest Airlines (NYSE:LUV) went down a similar road in April, raising about $4 billion in stock and convertible bonds.

There is no guarantee that Delta makes a similar move, of course. Delta already raised several billion in new debt earlier this year and expected to finish the second quarter with about $14 billion in liquidity. But considering the airline burns about $40 million per day under current conditions, things needs to improve pretty quickly.

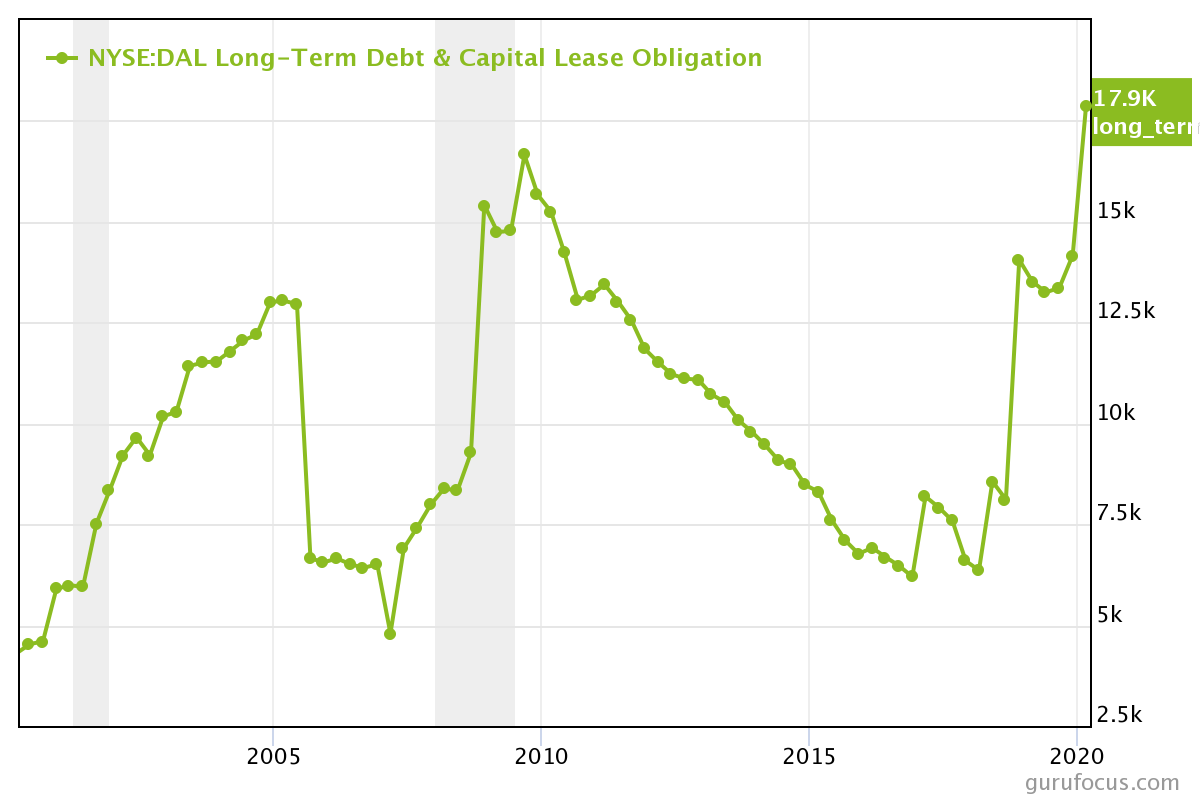

Delta’s debt-equity ratio was already a little on the high side before the pandemic hit and stood at 1.61 as of the end of March, and these figures don’t include the debt accumulated since the end of March.

Source: GuruFocus

As of quarter end, DAL stock had nearly $18 billion in long-term debt. When the numbers come out for the June quarter, that figure should be more than $21 billion. Even in a more normal environment, Delta’s rising debt load would be a red flag. But today’s situation is far from normal, and Delta indicated recently that it may be in violation of certain debt covenants by early next year.

I don’t expect Delta’s creditors to start seizing assets. It’s clearly in their best interests to negotiate. But any negotiations might involve Delta having to dilute its shareholders with an equity offering.

Recovery In Travel Is Far From Certain

Of course, the elephant in the room remains Covid-19. It’s now peak summer vacation season, and Americans are starting to travel again. But even so, the recovery has been tepid. Flights are down about 63% from year-ago levels. That’s better than the 96% year-over-year reduction we saw in April, but it’s still far from good.

It’s also not clear how sustainable it is. COVID cases are rising again, particularly in vacation hot spots like Florida and southern California. And once summer is over, business travel really needs to pick up the slack.

Unfortunately, that’s going to be a slower process than in past recessions. Most companies are still reluctant to bring employees back to the office let alone authorize them to travel. And the popularity of Zoom Video Communications (NASDAQ:ZM) and other virtual meetings have made that marginal business trip a lot less necessary.

Business travel will resume at some point. At the end of the day, there is still no substitute for a face to face meeting when you’re negotiating a deal or working on a critical project. But it’s that marginal business trip that was of somewhat questionable value might be cut out permanently.

All of this is to say that, while airlines won’t be disappearing, the competitive landscape really has changed for the foreseeable future. And DAL stock at current prices simply doesn’t reflect that competitive landscape.

DAL stock is best avoided at current prices.

Charles Lewis Sizemore, CFA is the principal of Sizemore Capital Management. As of this writing he did not hold a position in any of the aforementioned securities.